Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Pacific Stone is stocked at 463 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, Sacramento, San Francisco, and Costa Mesa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

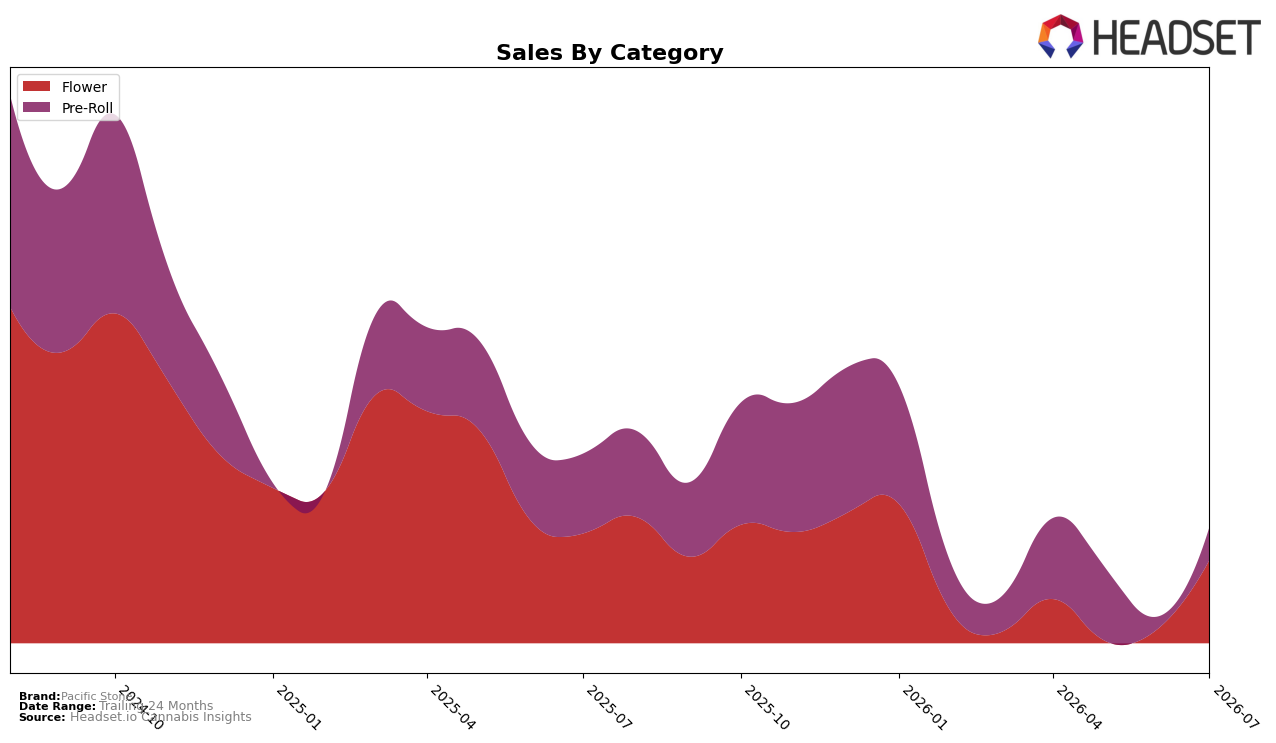

Pacific Stone’s mix in July 2026 tipped slightly toward Flower at 52.32% share (up versus Pre-Roll at 47.68%), with Flower rising 13.84% month over month despite a 4.51% year-over-year decline, while Pre-Roll grew 4.20% MoM but fell 8.35% YoY. Average pricing fell 14.41% YoY to $22.56 across the brand, with category-level pricing sitting at $24.66 for Flower and $20.63 for Pre-Roll, and overall brand sales were down 6.38% YoY alongside a 25.51% decline versus 24 months prior. In California Flower, the brand ranked 16th, indicating that the July 2026 channel shift favored higher-volume Flower gains over Pre-Roll, but not enough to offset broader YoY drag.

The mix pivot toward Flower alongside lower average prices suggests an emphasis on volume capture within the mid-priced tiers, with the 13.84% MoM Flower lift outpacing the 4.20% MoM Pre-Roll rise while both categories remain down YoY (Flower -4.51%, Pre-Roll -8.35%). With Flower holding a 52.32% share and a 16th-place rank in California Flower, the pattern implies that Pacific Stone is using price compression to defend shelf position and expand unit throughput in Flower, accepting YoY softness as the trade-off for retaining visibility and basket relevance.

Competitive Landscape

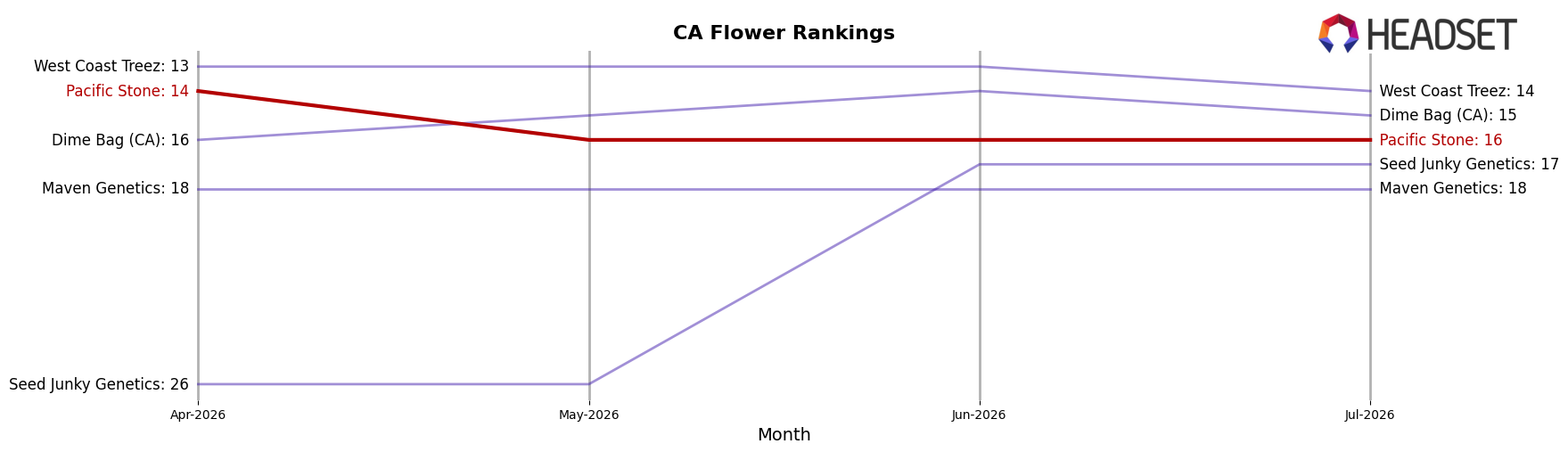

Pacific Stone sits at rank #16 in California Flower for July 2026, unchanged YoY from rank #16 but down 2 positions versus April 2026 when it held #14, while its historical peak of #8 in October 2024 underscores a longer-run slide; in contrast, STIIIZY moved from #2 to #1 with 59.7% YoY sales growth and CannaBiotix (CBX) slipped from #1 to #2 despite 7.0% YoY growth, and CAM climbed from #4 to #3 with 52.2% YoY growth while Claybourne Co. fell from #3 to #5 with a -1.4% YoY decline; the pattern implies Pacific Stone’s flat YoY rank and quarter-over-quarter dip position it as a share donor in a market where faster-growing leaders are consolidating ranks.

Notable Products

Wedding Cake (3.5g) posted the standout movement in July 2026 with a 43.5% month-over-month rise to $100,601 while still trailing the top-ranked Blue Dream Pre-Roll 14-Pack (7g) at rank 1 after a 4.9% decline, signaling accelerated premium flower traction against softening flagship pre-roll volume. Within pre-rolls, Wedding Cake Pre-Roll 14-Pack (7g) climbed 23.1% to rank 4 as 805 Glue Pre-Roll 14-Pack (7g) fell 8.6% at rank 6, and with six of the top ten being Pre-Roll SKUs the format remains concentrated despite mixed momentum. The 805 Glue (3.5g) flower advanced 35.1% at rank 9 while Blue Dream (3.5g) ticked up 6.5% at rank 8, indicating variety-led gains in flower even as Blue Dream pre-rolls cooled by 4.9% and the Wedding Cake Pre-Roll 2-Pack (1g) slipped 7.0% at rank 5. Together, the pattern points to Pacific Stone leaning into multi-pack pre-rolls for scale while reallocating focus toward surging value-tier flower cuts to diversify away from single-format dependence.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.