Where to Buy

CLOVR is stocked at 152 licensed dispensaries across Missouri and Mississippi, 151 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Columbia, Springfield, and Cape Girardeau. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

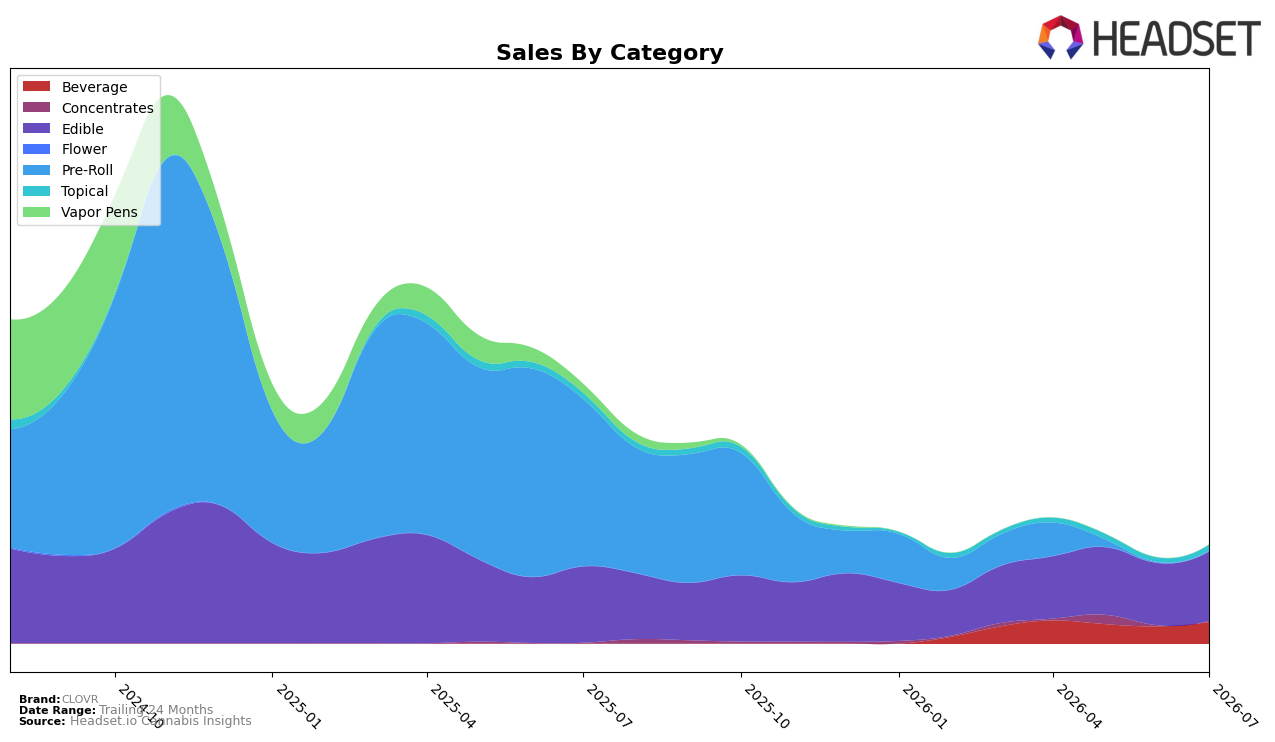

Market Insights Snapshot

CLOVR’s July 2026 mix is concentrated in Edible at 70.92% share with a month-over-month gain of 11.30% but a year-over-year decline of 9.04%, while Beverage expanded month-over-month by 24.82% to 22.23% share despite no year-over-year comparison available. Topical holds 5.46% share with 24.33% month-over-month growth against a 9.24% year-over-year decline, and small niches like Concentrates at 0.70% grew 25.67% year-over-year but only 3.91% month-over-month, whereas Pre-Roll sits at 0.69% share after a 157.98% month-over-month rebound from a 99.60% year-over-year collapse. With average price up 4.33% year-over-year to $16.64 and Edible pricing at $17.47, the mix shift toward faster month-over-month growth in Beverage and Topical alongside a still-dominant but contracting Edible suggests a tactical pivot toward immediate-volume categories while legacy Edible scale anchors the base.

The concentration in Edible at 70.92% alongside a 9.04% year-over-year drop and an Edible category rank of 38 in Missouri positions CLOVR as scale-heavy but mid-tier, and the 24.82% month-over-month acceleration in Beverage plus 24.33% in Topical indicates a near-term drive to diversify baskets where price points are lower than Edible by 21.8% and 16.3%, respectively. The 157.98% month-over-month surge in Pre-Roll off a 99.60% year-over-year base erosion and the 25.67% year-over-year rise in Concentrates at 0.70% share imply opportunistic recovery and experimentation at the fringes rather than mix redefinition, meaning short-term momentum is coming from breadth expansion while long-term positioning still relies on stabilizing Edible performance and price architecture.

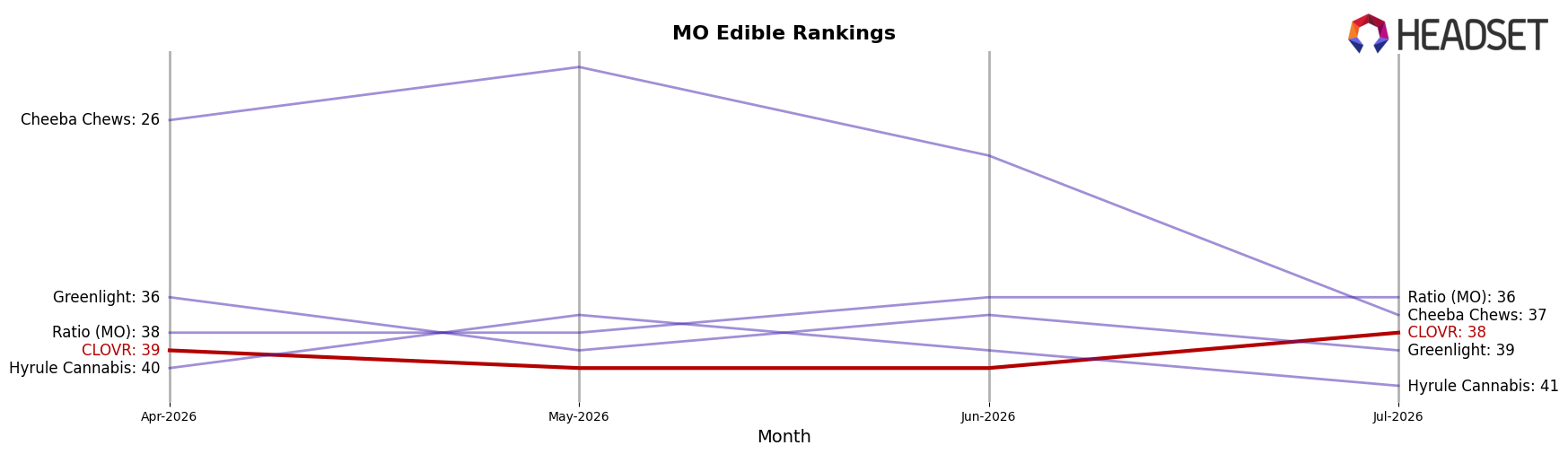

Competitive Landscape

CLOVR is ranked #38 in MO Edible in July 2026, unchanged from #38 year over year, and essentially flat versus April 2026 when it sat at #39, while still far from its peak of #29 reached in September 2024; in contrast, Good Day Farm improved from #3 to #2 as sales grew 11.8% year over year, and Good Taste climbed from #8 to #4 with a 63.8% year-over-year sales increase. Meanwhile, category leaders are shifting: Gron / Grön held #1 despite a 5.5% sales decline and Smokiez Edibles fell from #2 to #5 with an 18.1% drop, indicating that CLOVR’s static rank alongside volatile top-tier moves implies a mid-pack stall where incremental share is being captured by faster risers rather than lost to incumbents.

Notable Products

Tickled Pink Shot (100mg THC, 2oz, 60ml) posted the steepest slide in July 2026 with a -9.15% month-over-month decline, while Royal Razz Shot (100mg THC, 2oz, 60ml) surged 49.25% and climbed to rank 6, signaling a shift within CLOVR’s beverage lineup. At the top, CBD/THC/CBN 1:1:1 Thin Mint Milk Chocolate Bar 10-Pack (100mg CBD, 100mg THC, 100mg CBN) held rank 1 with +16.14% MoM as two other chocolates rose about +40% each into ranks 3–4, and at least six of the top ten are Edibles, concentrating share away from drinks. With Watermelon Sucker (25mg) dropping -38.55% at rank 2 against MoM gains in multi-cannabinoid chocolate bars, the mix points to a pivot toward multi-cannabinoid Edibles anchoring leadership while beverages become more selective bets.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.