Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

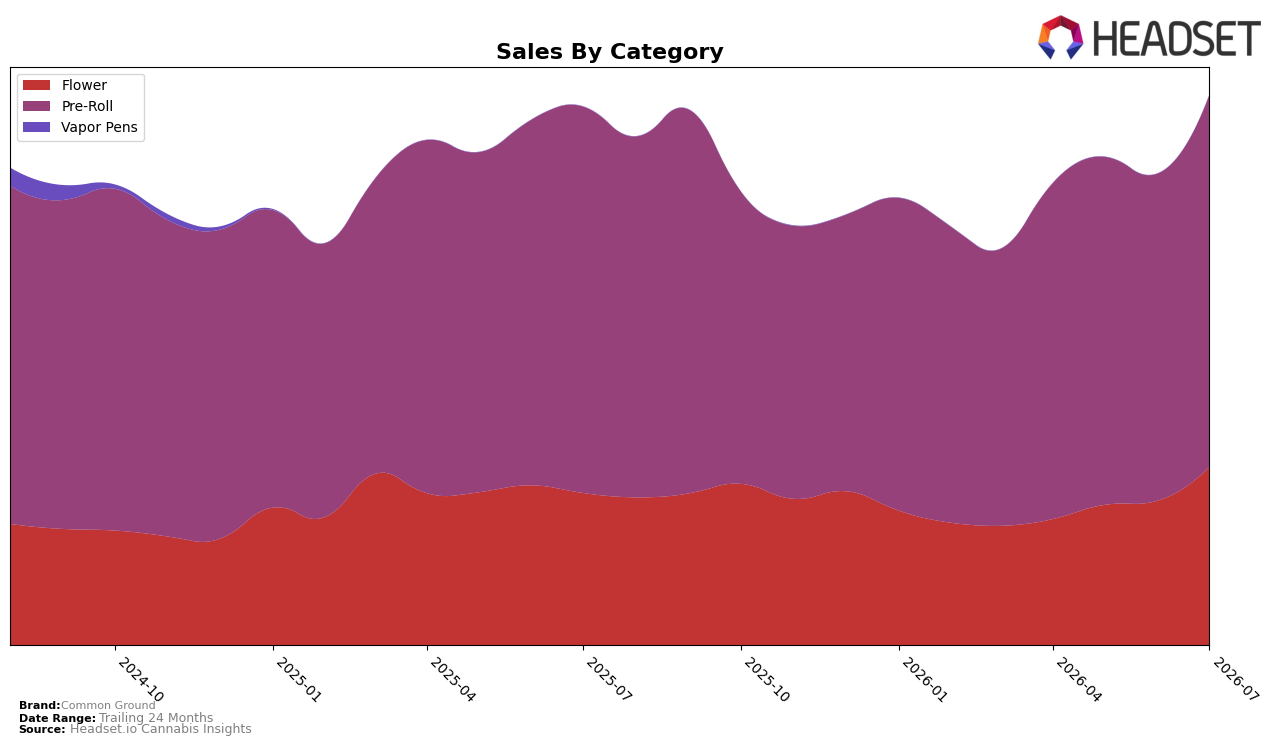

In July 2026, Common Ground’s sales are concentrated in Pre-Roll at 67.64% share while Flower holds 32.36%, with Pre-Roll down 3.64% year over year but up 13.82% month over month, and Flower up 17.14% year over year and up 23.28% month over month. Despite a brand-level average price decline of 1.03% year over year, Pre-Roll’s average price sits at 17.68 while Flower commands 24.90, and the brand’s overall sales grew 2.23% year over year against a 13.98% two-year gain; the pattern implies a July pivot where Flower’s faster growth rate and higher price point are lifting mix contribution even as Pre-Roll remains the volume anchor.

With a Pre-Roll rank of 16 in Saskatchewan and a 13.82% month-over-month lift in that category alongside a 23.28% month-over-month surge in Flower, the July 2026 mix suggests momentum is shifting toward higher-value Flower without displacing Pre-Roll scale. The combination of a 2.23% year-over-year brand sales increase and a 1.03% average price decline indicates price elasticity is working in Pre-Roll while Flower’s 17.14% year-over-year growth supports premium positioning; the implication is a barbell strategy where Pre-Roll defends share and Flower drives margin, positioning Common Ground to climb from rank 16 as Flower mix expands.

Competitive Landscape

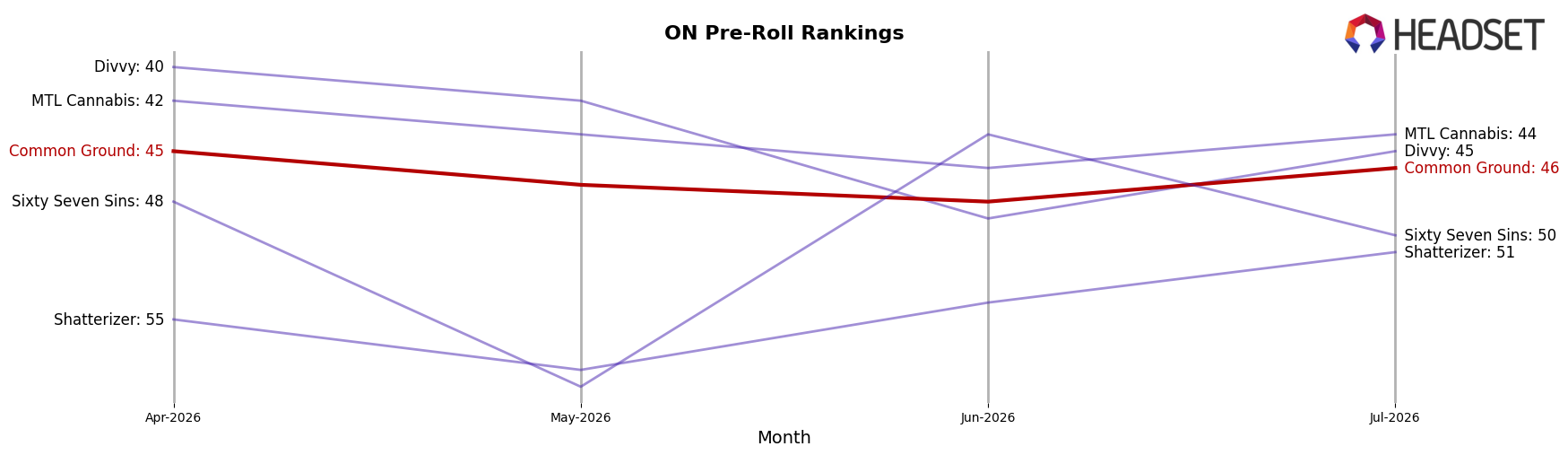

Common Ground sits at rank #46 in ON Pre-Roll in July 2026, down 9 spots year over year from #37 and slipping 1 position since April 2026 from #45, while still 17 places below its peak of #29 from July 2024; in contrast, Back Forty / Back 40 Cannabis rose from #2 to #1 as its sales grew 67.4% year over year and General Admission fell from #1 to #2 amid a 23.2% year-over-year sales decline, indicating that Common Ground’s downward drift alongside leadership churn at the top signals share consolidation away from mid-tier players and implies further rank pressure unless distribution or assortment shifts reverse the trajectory.

Notable Products

Pink Rozay Pre-Roll 2-Pack (2g) posted the standout move in July 2026 with a +33.2% MoM surge into rank 4, while Strawberry Pie Pre-Roll 5-Pack (2.5g) advanced +23.3% to rank 2, together signaling accelerated velocity in multi-pack pre-rolls. Amherst Sour Diesel Pre-Roll 10-Pack (5g) held rank 1 with +12.6% MoM and roughly $268,582 in sales, and Purple Gas Pre-Roll 10-Pack (5g) added +11.5% at rank 10; with seven of the top ten being Pre-Roll SKUs, the assortment is consolidating around format-driven convenience rather than strain novelty. The concentration of gains above +10% across multiple pack sizes implies Common Ground is optimizing around repeatable pre-roll demand curves and away from slower Flower turns, which saw Lemon Pave Milled (7g) dip -1.9% at rank 9.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.