May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

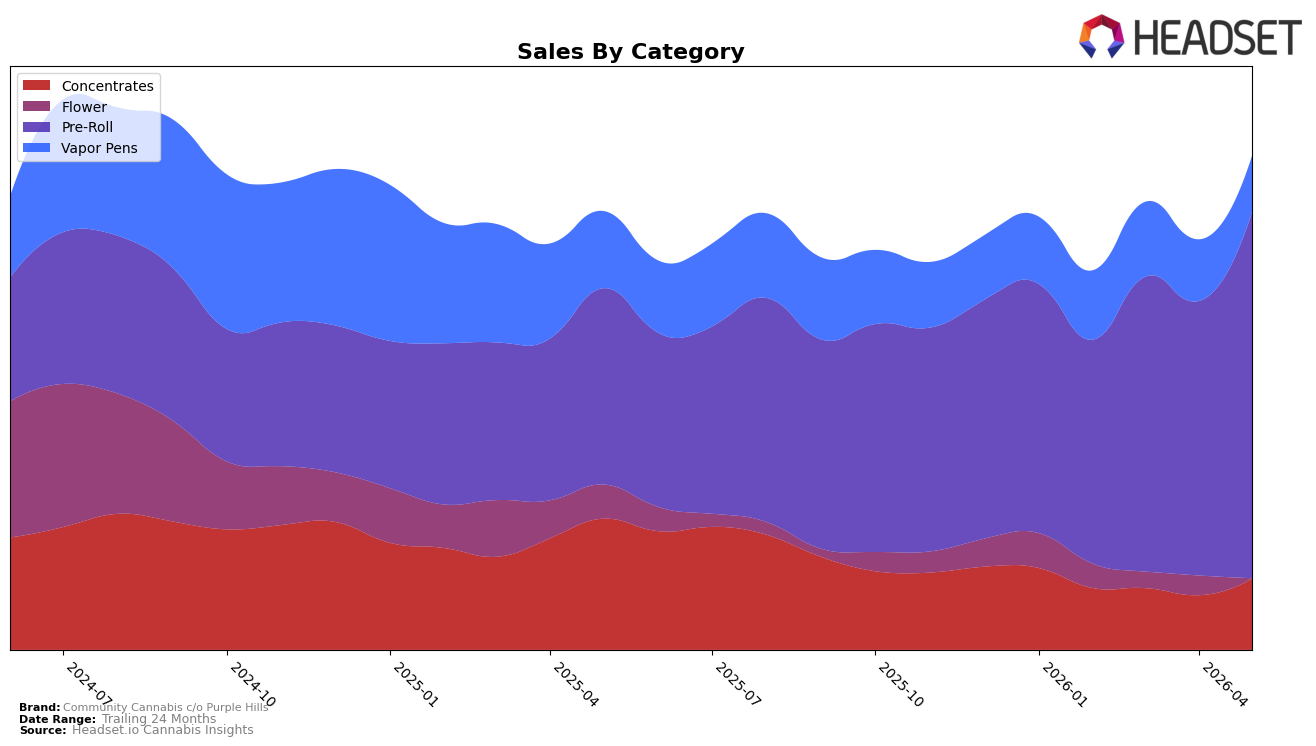

In May 2026, Community Cannabis c/o Purple Hills concentrated 71.91% of sales in Pre-Roll with year-over-year growth of 84.01% and month-over-month growth of 32.69%, while Vapor Pens held 12.01% share with a -25.13% year-over-year change and a -7.94% month-over-month change. Concentrates represented 14.91% share despite a -43.73% year-over-year decline but rebounded 27.53% month over month, and Flower contracted to 1.17% share with an -84.77% year-over-year drop and a -76.12% month-over-month slide. With brand-level sales up 11.96% year over year alongside a -25.40% average price shift, the pattern implies a deliberate pivot toward value-leaning Pre-Rolls and away from higher-priced Flower, concentrating volume where price elasticity is favorable.

The shift leaves Community Cannabis c/o Purple Hills ranked 51 in Pre-Roll in Ontario, indicating that the 32.69% month-over-month lift in its largest category has not yet translated into top-tier placement while Vapor Pens’ -7.94% month-over-month decline and Concentrates’ 27.53% month-over-month uptick suggest repositioning headroom across inhalables. Given Pre-Roll’s 71.91% share and Concentrates’ 14.91% share against a brand average price at $15.09, the mix implies a strategy anchored in high-velocity, lower-ticket units, where incremental rank gains will likely hinge on sustaining Pre-Roll growth while stabilizing Vapor Pens to diversify beyond a single-category dependency.

Competitive Landscape

Community Cannabis c/o Purple Hills sits at rank #51 in ON Pre-Roll for May 2026, improving 14 positions from #65 year over year, and edging up 6 spots from #57 in February 2026 to match its peak rank #51 in May 2026; meanwhile, category leaders moved in divergent directions as Back Forty / Back 40 Cannabis climbed from #3 to #1 with a 66.8% YoY sales increase while General Admission slipped from #1 to #2 alongside a 13.6% YoY sales decline. This pattern—mid-tier rank ascent amid a reshuffling top three and mixed competitor growth—implies Community Cannabis c/o Purple Hills is gaining placement through incremental share capture rather than category-wide lift, positioning it to convert small rank wins into sustained distribution if it maintains momentum against both rising and contracting leaders.

Notable Products

Indica XL Distillate Cartridge (1.2g) posted the steepest decline in May 2026 at -17.6% MoM while sliding to rank 5, whereas Sour Grapes XL CO2 Cartridge (1.2g) eased -4.3% at rank 4; by contrast, Bakery Preroll 14-Pack (7g) climbed 44.1% to rank 2 but fell short of the +50% threshold that would redefine the month’s narrative. TwoFer Pre-Roll 2-Pack (2g) rose 21.9% to rank 1 as Hybrid Hash (3g) advanced 29.8% at rank 3, and three Vapor Pens still populate ranks 4–6 with mixed momentum including a 27.3% lift for 95+ Island Drip Distillate Cartridge (0.95g). With Pre-Roll SKUs occupying two of the top three ranks and Vapor Pens spanning four of the top ten, the mix implies a tilt toward value-driven inhalables where pre-roll scale offsets volatility in cartridges, guiding Community Cannabis c/o Purple Hills to prioritize bundle-led Pre-Roll volume while triaging underperforming pen formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.