Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

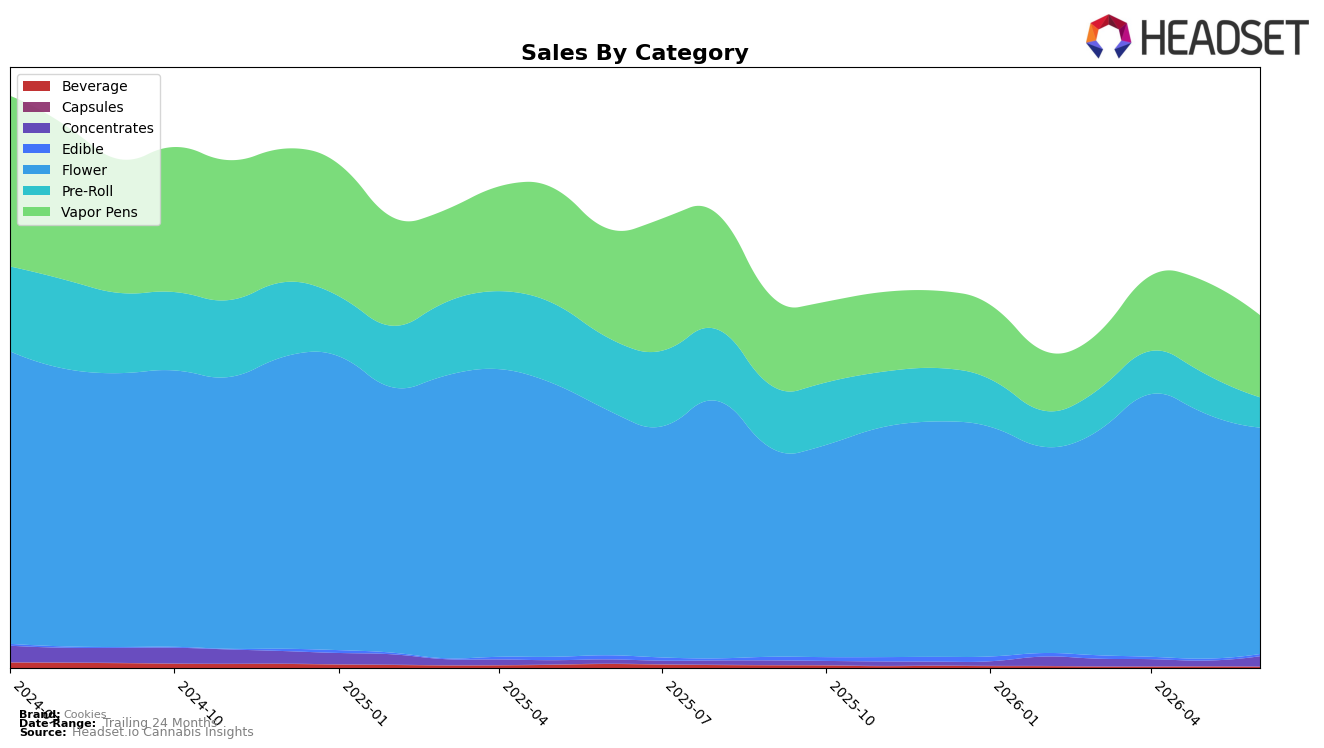

In June 2026, Cookies concentrated 64.41% of sales in Flower while Vapor Pens held 23.32%, a mix that tilted further toward the core as Flower fell a smaller 7.55% year over year versus a 24.72% YoY drop in Vapor Pens. Month over month, Flower declined 7.73% compared with an 11.05% MoM slide in Vapor Pens, while Pre-Roll contracted 23.96% MoM and 58.54% YoY, shrinking its 8.54% share. The outlier was Concentrates, which grew 149.09% YoY and 83.99% MoM to 2.84% share, alongside a 14.40% MoM uptick in Edible that still sat at just 0.54% share. With brand sales down 19.75% YoY and the average price up 7.62% YoY to $29.93, the pattern implies Cookies is leaning on higher-priced Flower to offset wider declines, while a small but rapidly expanding Concentrates pocket is the only material countertrend.

Positioning-wise, holding rank 16 in Flower in Ohio while Flower’s share sits at 64.41% and falls less sharply than Vapor Pens (−7.73% vs. −11.05% MoM) implies the brand’s relative footing is anchored to Flower rather than inhalable adjacencies. The 2.84% share for Concentrates with triple‑digit YoY growth and an 83.99% MoM surge, contrasted with Pre-Roll’s 58.54% YoY contraction and Beverage’s 69.35% YoY decline, suggests Cookies can reposition around potency-driven formats without abandoning Flower leadership. The thesis is that Cookies’ near-term defensibility comes from stabilizing Flower price-mix while selectively scaling Concentrates to diversify away from categories with double-digit MoM/YoY erosion.

Competitive Landscape

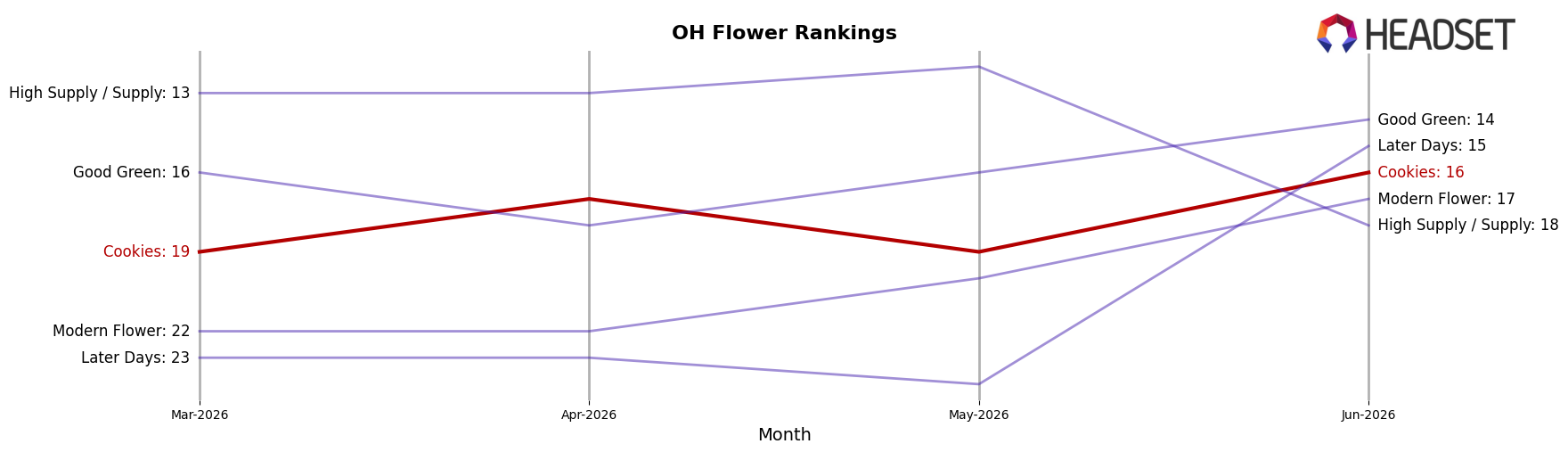

Cookies ranks #16 in Ohio Flower in June 2026, a +26-place climb from #42 in June 2025, and up 3 spots from #19 in March 2026; this coincides with hitting a peak rank of #16 in June 2026 while remaining outside the top 10. In contrast, Klutch Cannabis moved from #20 to #1 year over year with +304.8% sales growth, while Riviera Creek slipped from #1 to #2 alongside a -22.7% sales decline, indicating that Cookies’ upward rank mobility is occurring as leaders reshuffle rather than during uniform market expansion; the pattern implies Cookies is gaining relative position but must convert momentum into share capture to break into the top tier.

Notable Products

Ridgeline Lantz (3.5g) posted the steepest decline at -36.4% month over month while dropping to rank 5, and Blue Raz Full Spectrum CO2 iKrusher Disposable (1g) fell -29.0% to rank 3, indicating consumer momentum pulled away from prior velocity SKUs. Mexican Flan (3.5g) rose +12.9% MoM at rank 7 as Apples & Bananas Pre-Roll (1g) climbed +25.1% at rank 2, while Fried Bananas Infused Pre-Roll (1g) slid -30.1% to rank 6, creating a split within inhalables by format and infusion. Four of the top ten are Flower SKUs clustered at ranks 1, 5, 7, and 8, with Hollywood (3.5g) holding rank 1 despite no reported MoM rate and Ridgeline Lantz Smalls (14.15g) anchoring the segment with $191,246 in June 2026, implying shelf power is concentrated in core flower tiers even as select pre-rolls gain share. The pattern implies Cookies is tilting its commercial mix toward dependable Flower leadership while reallocating support away from volatile infused and disposable variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.