Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

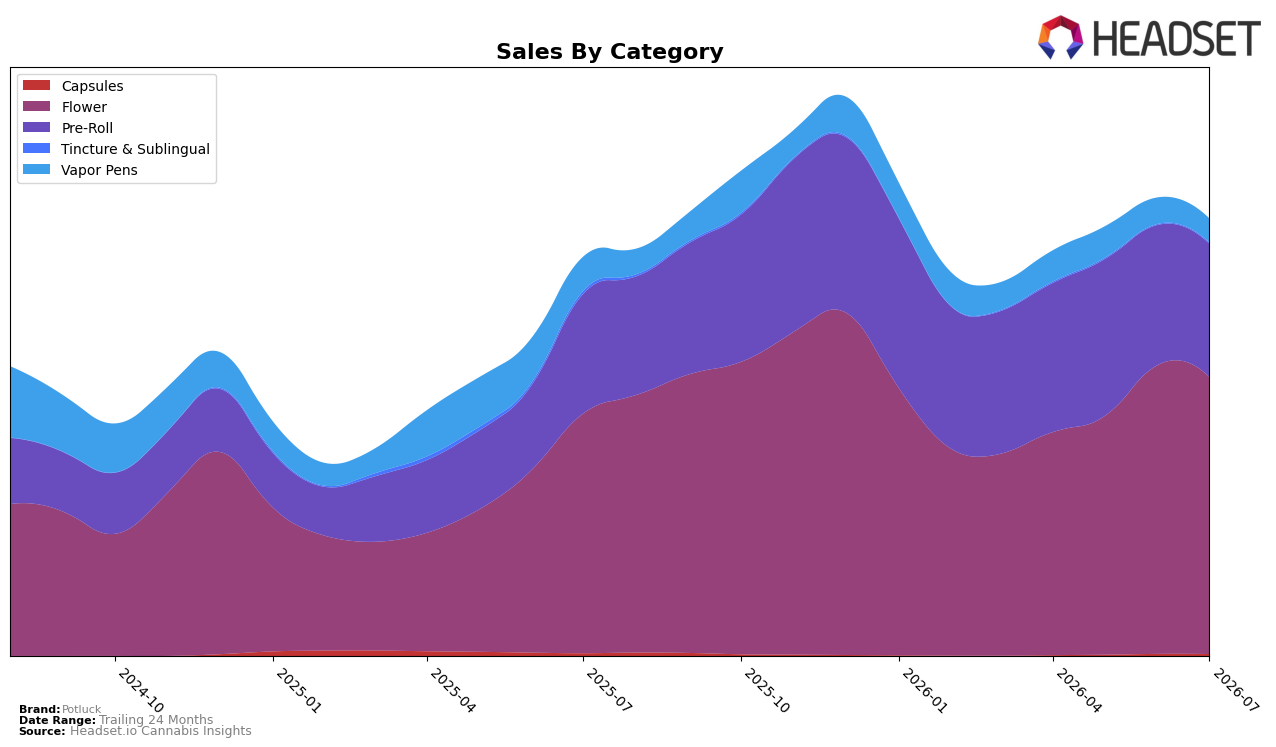

In July 2026, Potluck concentrated 63.41% of sales in Flower with a 15.57% year-over-year increase but a 4.19% month-over-month decline, while Pre-Roll held 30.50% share with 11.54% YoY growth and a 4.81% MoM dip. Vapor Pens contracted to 5.46% share with a 30.02% YoY decline and a 9.21% MoM decline, and Capsules fell 29.90% YoY with a 6.93% MoM dip at 0.43% share; the only sequential uptick came from Tincture & Sublingual, up 39.32% MoM despite a 67.69% YoY drop at 0.19% share. With overall brand sales up 9.60% YoY and average price down 1.25% YoY to $17.34, the pattern implies Potluck is leaning on Flower and Pre-Roll for scale while allowing premium-sensitive or niche formats like Vapor Pens and Capsules to contract, sharpening category focus even as rank 14 in Flower in Ontario caps upside without further mix shifts.

The mix shift implies Potluck’s positioning is consolidating around value-accessible inhalables, where Flower’s 63.41% share and Pre-Roll’s 30.50% share can absorb modest price elasticity, evidenced by a 1.25% YoY price decrease alongside 15.57% and 11.54% YoY category gains. Sequential declines of 4.19% in Flower and 4.81% in Pre-Roll against a 39.32% MoM rebound in Tincture & Sublingual indicate a tactical opportunity to use small wellness-adjacent formats to stabilize volatility while maintaining the core, and the 30.02% YoY decline in Vapor Pens combined with a 9.21% MoM drop suggests de-emphasis of higher-price-per-unit segments that may be diluting share without improving July 2026 rank 14 in Ontario Flower.

Competitive Landscape

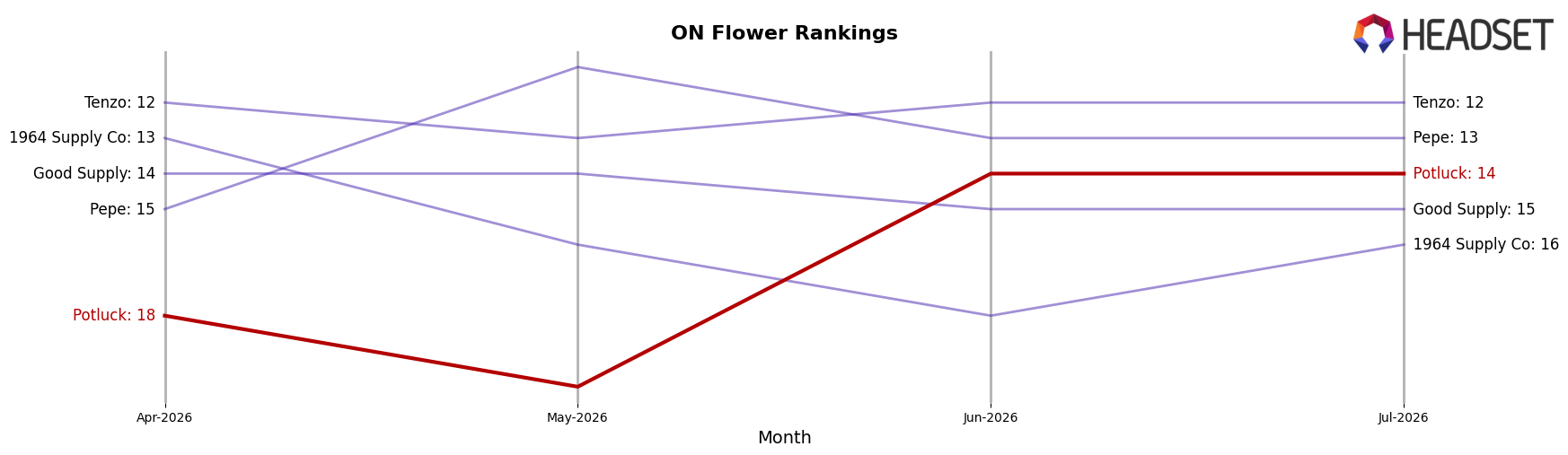

Potluck is ranked #14 in ON Flower in July 2026, improving 8 positions from #22 year over year and rising 4 spots from #18 in April 2026; this matches a new peak rank of #14 in July 2026 while sitting 13 positions behind Shred at #1. Competitive movement is upward at the top: Shred moved from #2 to #1 with 17.2% YoY sales growth, and Spinach advanced from #4 to #2 on 31.1% YoY growth, whereas Back Forty / Back 40 Cannabis slipped from #1 to #4 with a 5.4% YoY decline; Potluck’s 3-month climb of 22% in rank terms (from #18 to #14) contrasts with the flat #3 position for Big Bag O' Buds (steady at #3) and the one-spot improvement for The Original Fraser Valley Weed Co. from #6 to #5. The pattern implies Potluck’s upward rank trajectory is timing into a tight top tier where gains require outpacing leaders that are still expanding share, making sustained incremental rank wins the likely path rather than a rapid leap.

Notable Products

Watermelon Wave Infused Pre-Roll (0.5g) posted the steepest decline in July 2026 at -21.3% MoM while sitting at rank 5, and Strawberry Cough Pre-Roll (0.5g) also fell -8.7% at rank 4. In contrast, Beaver Tail (7g) in Flower rose +6.7% MoM to rank 3, and Mango Dream (7g) slipped -12.8% at rank 10. Seven of the top ten are Pre-Roll SKUs, with leaders like Berry Cherry Infused Pre-Roll (0.5g) at rank 1 despite an -8.1% MoM dip, indicating a portfolio tilted toward Pre-Rolls even as momentum shifts toward larger-pack Flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.