May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

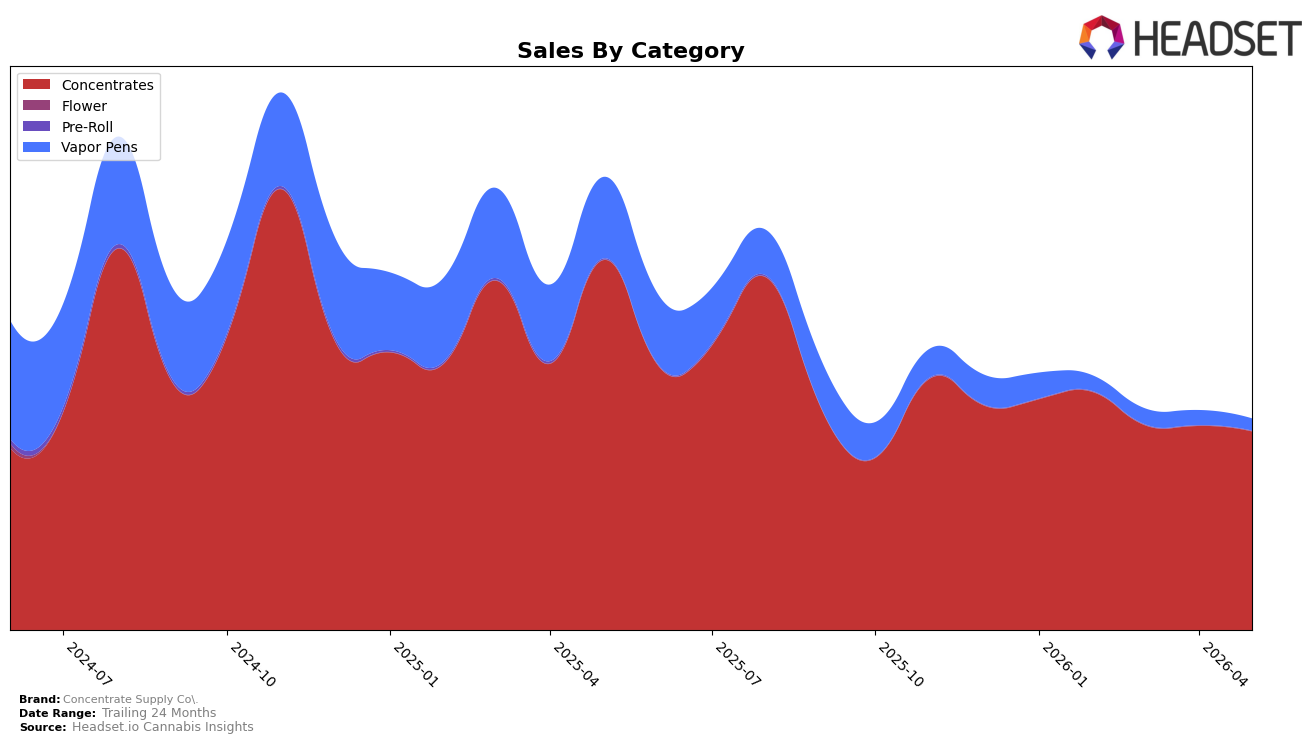

In May 2026, Concentrate Supply Co. concentrated 94.38% of sales in Concentrates with a year-over-year change of -46.38% and a month-over-month change of -2.68%, while Vapor Pens held 5.62% share with a year-over-year change of -85.45% and a month-over-month change of -19.67%. Overall brand sales declined -53.50% year over year alongside a 16.43% increase in average price, and within Concentrates the average price was $19.07 compared to $21.66 in Vapor Pens. The pattern implies a deliberate tilt toward lower-priced Concentrates while de-emphasizing Vapor Pens, with price-taking adding pressure to volume as category exposure concentrates risk.

Within Colorado Concentrates, the brand placed rank 12 as of May 2026, while brand sales over 24 months declined -33.37% and month-over-month mix further favored Concentrates by 2.68 percentage points versus a 19.67% retreat in Vapor Pens. The average price across the brand at $19.20 rose 16.43% year over year as Vapor Pens underperformed by -85.45% year over year relative to -46.38% in Concentrates. This positioning implies the brand is competing as a mid-pack Concentrates specialist in Colorado, trading short-term breadth for depth and relying on price discipline to defend share despite steeper unit elasticity in Vapor Pens.

Competitive Landscape

Concentrate Supply Co. sits at rank #12 in Colorado Concentrates for May 2026, down 5 positions year over year from #7 and down 1 position versus February 2026’s #11, while its historical peak was #4 in November 2024; by contrast, Amber advanced from #3 to #1 alongside a 101.7% YoY sales increase, and 710 Labs held at #2 despite a -16.9% YoY sales decline, indicating that Concentrate Supply Co.’s relative slippage is driven more by rivals’ upward movement than broad category contraction. With Spectra moving from #5 to #3 on 14.7% YoY growth and Billo jumping from #16 to #5 on 128.2% YoY growth, the brand’s fall from #7 to #12 over the year and from #11 to #12 over the last three months suggests that without a share-accretive initiative, the likely trajectory is continued mid-tier compression despite a prior peak at #4 in November 2024.

Notable Products

Devil Driver X Zero Gravity Wax (1g) posted the standout movement in May 2026 with a +35.9% month-over-month increase, climbing to rank 2, while Hybrid Wax (1g) rose +23.9% to hold rank 1. Super Boof Sugar Wax (4g) in rank 6 edged up +6.4%, whereas Super Boof Sugar Wax (1g) at rank 3 barely moved at +1.7%, indicating momentum is consolidating in value or specialty formats over core 1g variants. Four of the top ten are Sugar Wax SKUs and six of the top ten are 1g Wax formats, and the 4g Kevin Garnett Wax (4g) at rank 4 carried the highest single-month dollar total at $14,420, pointing to a mix skew that leans into price-tier diversification rather than a single-format push. The pattern implies Concentrate Supply Co. is pulling volume through both premiumized collabs and multi-gram value packs, suggesting a barbell strategy to capture share across budget and enthusiast segments.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.