Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

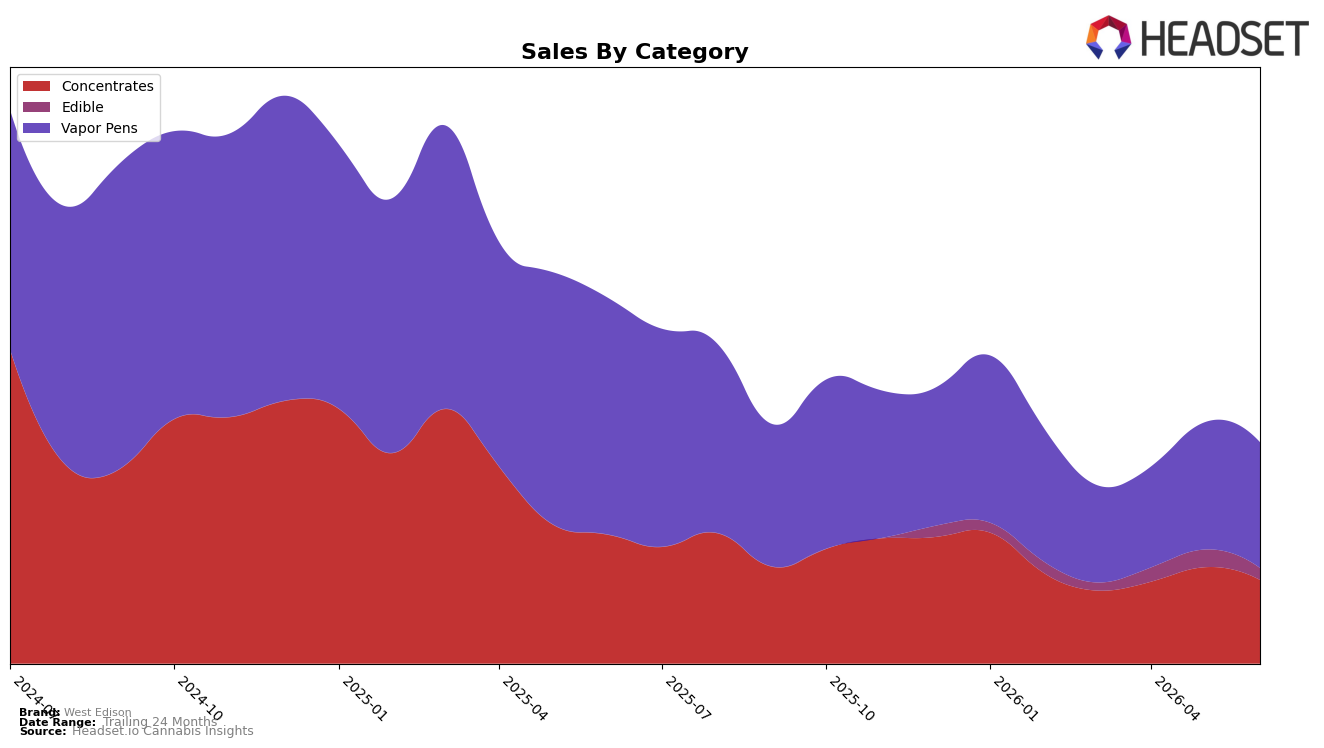

In June 2026, West Edison concentrated 56.89% of sales in Vapor Pens with a year-over-year decline of 46.89% and a month-over-month dip of 1.14%, while Concentrates held 37.82% share with a 35.08% YoY drop and a 13.22% MoM pullback; Edible accounted for 5.29% share with a 33.01% MoM contraction and no year-over-year baseline. Average price rose 10.95% YoY to $20.54 even as Vapor Pens averaged $35.14 and Concentrates averaged $13.38, implying a mix that skews toward higher-priced units despite total brand sales falling 39.53% YoY and 61.51% over 24 months; the pattern indicates a reliance on premium-priced Vapor Pens alongside a shrinking Concentrates contribution that is accelerating month-on-month.

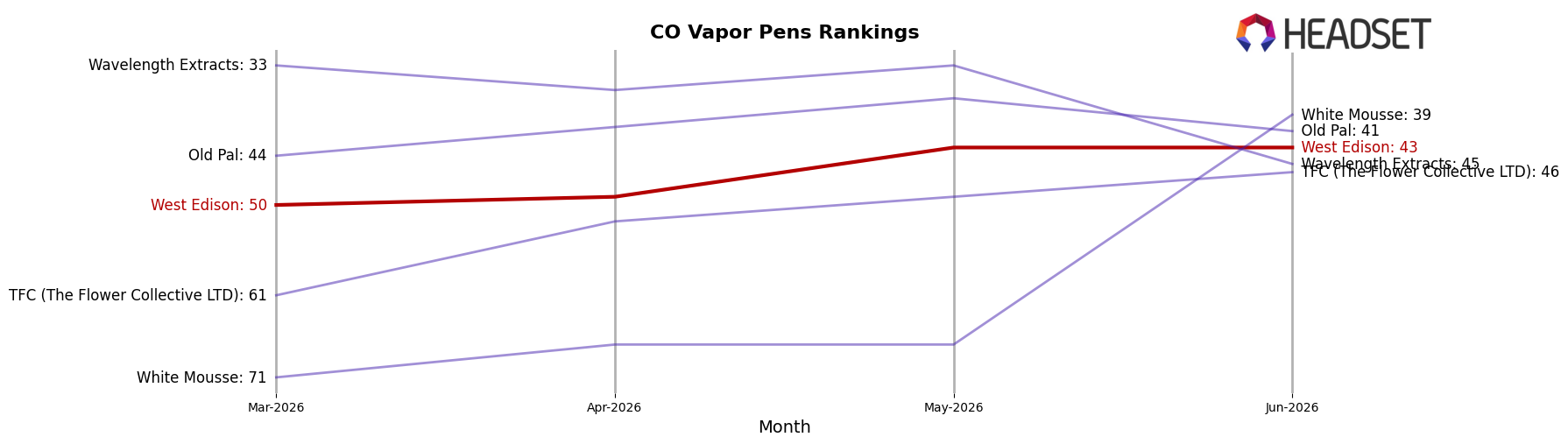

The category shifts suggest West Edison is trading depth for price, as higher-priced Vapor Pens maintain the majority share at 56.89% while suffering a larger 46.89% YoY contraction than the 35.08% YoY drop in Concentrates, pointing to exposure in a premium-led segment that is losing velocity. With a 43 rank in Colorado Vapor Pens and a 13.22% MoM decline in Concentrates against just 1.14% MoM in Vapor Pens, the near-term resilience sits in the lead category but at the cost of broader basket penetration; this positioning implies that stabilizing share will require either pricing calibration in Vapor Pens or reactivation of value-oriented Concentrates to counter the 33.01% MoM retreat in Edible and preserve category breadth.

Competitive Landscape

West Edison sits at rank #43 in CO Vapor Pens in June 2026, down 10 spots year over year from #33, yet up 7 places from #50 three months ago; the brand’s peak was #27 in September 2024, placing its current position 16 ranks below that high while still marking a quarter-on-quarter lift. In contrast, Spherex rose from #2 to #1 as its sales fell 9.6%, and PAX improved from #3 to #2 with 22.5% sales growth, indicating leaders can gain rank despite mixed sales outcomes; meanwhile, Bonanza Cannabis Company declined from #1 to #5 alongside a 67.4% sales drop. The pattern implies West Edison’s rank trajectory is stabilizing off a low base but remains structurally below its September 2024 ceiling, suggesting share recovery requires gains that exceed the incremental improvements seen over the past three months.

Notable Products

Strawberry RSO Full‑spectrum Gummy (100mg) posted the steepest decline in June 2026 at -34.4% MoM while dropping to rank 6, and Blue Raspberry RSO Full-spectrum Gummy (100mg) fell -26.7% MoM at rank 8, indicating Edibles are losing velocity versus other formats. In contrast, Sherb Cake Activated Oil Syringe (1g) rose 12.1% MoM to rank 2, and Vapor Pens saw mixed results with Pineapple Express Distillate Cartridge (1g) sliding -19.7% MoM at rank 4 even as the category holds multiple top‑10 slots. With Concentrates occupying ranks 1–3 and at least four of the top ten being Vapor Pens, the mix points toward prioritizing inhalable formats over Edibles as the near‑term commercial path.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.