Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

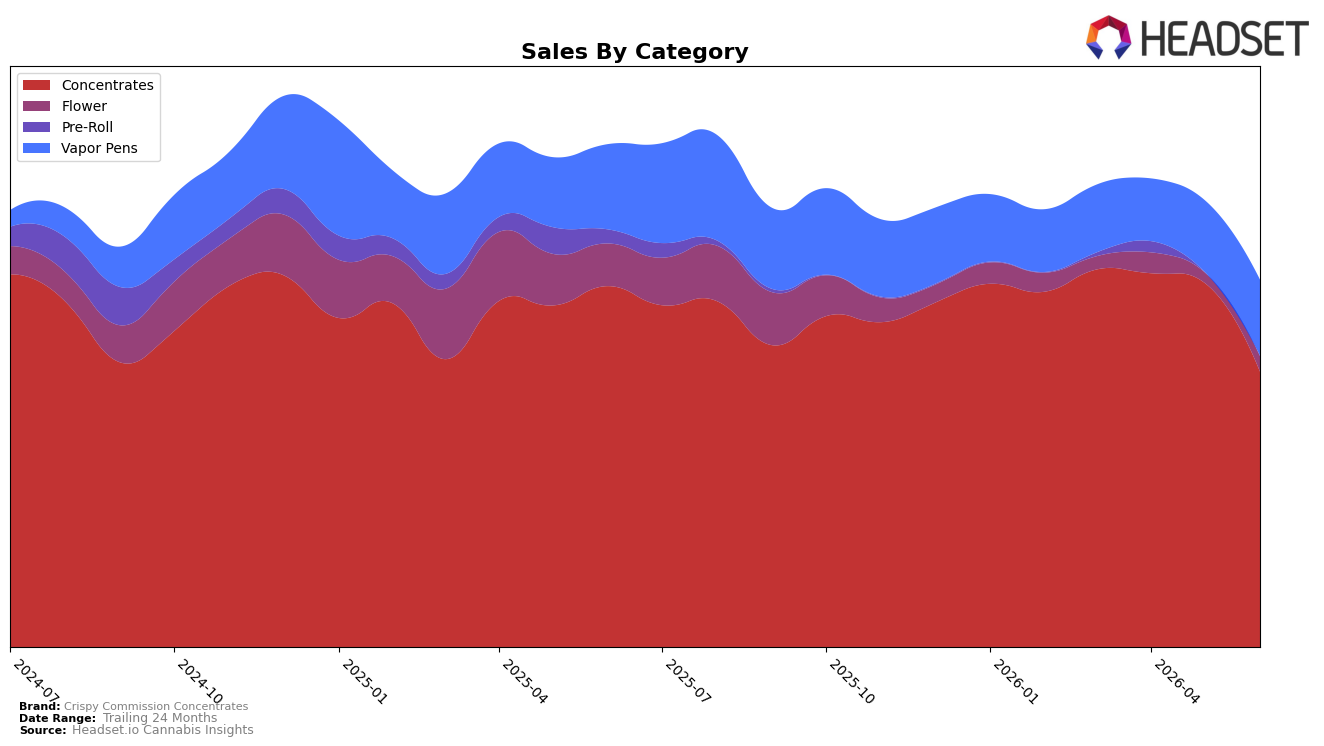

Crispy Commission Concentrates concentrated 75.16% of June 2026 sales in Concentrates, where sales fell 23.71% year over year and 24.39% month over month, while Vapor Pens rose 5.85% month over month despite a 10.95% year-over-year decline to 20.67% share; Flower held 4.17% share with a 48.63% month-over-month lift against a 63.91% year-over-year drop. Despite brand-level sales down 27.02% year over year and average price easing 1.94%, the brand held rank 2 in Concentrates in Massachusetts, implying that the category-led pullback is broad-based while the rank signals relative stability within its core.

The mix shift—Concentrates losing 24.39% month over month as Vapor Pens gained 5.85% and Flower rebounded 48.63%—suggests consumers are diversifying formats, with price-sensitive trade-off visible as average prices cluster near $35.32 in Concentrates and $31.70 in Vapor Pens. Holding rank 2 in Concentrates alongside a 23.71% category-level year-over-year decline and a 27.02% brand-level year-over-year decline indicates the current positioning is anchored in a shrinking core, so incremental growth likely depends on extending share in Vapor Pens or converting Flower’s month-over-month momentum into durable contribution.

Competitive Landscape

Crispy Commission Concentrates sits at rank #2 in MA Concentrates in June 2026, unchanged from #2 a year earlier, while its prior peak at #1 in October 2025 did not carry forward as the brand also held #2 three months ago; meanwhile, Good Chemistry Nurseries held #1 year over year with a 31.3% YoY sales increase, and Nature's Heritage remained #3 with 28.0% YoY growth, indicating Crispy Commission Concentrates’ flat rank versus competitors’ double-digit gains points to a stable but capped position unless it reclaims share from the leader.

Notable Products

Grease Bucket Cured Budder (1g) posted the standout move in June 2026 with a +104% month-over-month surge to rank 2, while Angry Ginger Live Resin Sauce Cartridge (1g) fell -24% to rank 8; this split, alongside Lemon OG Haze Live Sauce Cartridge (1g) holding rank 1, signals a pivot where concentrate formats gain share even as one vapor pen weakens. With eight of the top ten SKUs in Concentrates and Vapor Pens and only one Flower item in the top seven, the rank spread from 1 to 10 concentrates revenue around extracts, implying Crispy Commission Concentrates is consolidating strength in dabbable and cartridge-led segments rather than broadening into flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.