Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Curaleaf is stocked at 167 licensed dispensaries across Florida, Connecticut, and 9 other states, 72 of them in Florida, with the deepest coverage in Tampa, Miami, Orlando, Jacksonville, and Boca Raton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

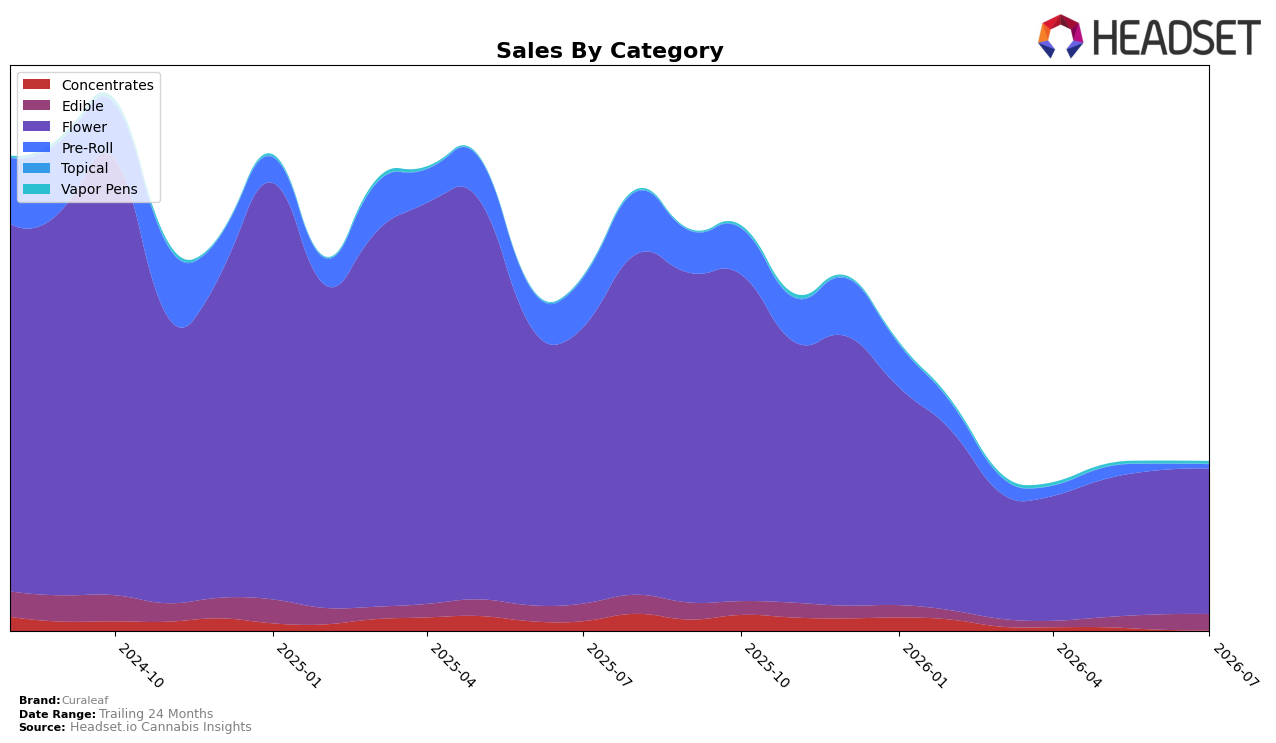

Curaleaf concentrated 86.62% of July 2026 sales in Flower while ranking 11 in Flower in Connecticut, with Flower down 47.42% year over year but up 0.97% month over month; Edible held 9.51% share with sales up 7.67% month over month yet down 7.28% year over year. Pre-Roll slipped to 2.35% share with a 35.94% month-over-month decline and a 91.94% year-over-year drop, whereas Vapor Pens, at 1.40% share, jumped 345.83% year over year and 1.39% month over month. The mix shows a heavy reliance on Flower despite its double-digit year-over-year contraction, implying exposure to category-specific headwinds even as incremental month-over-month gains and Vapor Pens recovery create a narrow offset.

With brand-level sales down 52.55% year over year alongside an 11.84% average price decrease, the shift toward lower-priced formats such as Pre-Roll (average price $6.69) and modestly priced Edible ($18.18) has not stabilized share, while Vapor Pens growth from a small base suggests repositioning potential rather than current scale. Holding rank 11 in Connecticut Flower while Flower commands 86.62% of the mix indicates that maintaining or improving Flower rank is pivotal; the juxtaposition of a 0.97% month-over-month Flower lift and a 77.54% month-over-month decline in Concentrates implies that near-term share defense hinges on Flower optimization and targeted investment in Vapor Pens where triple-digit year-over-year momentum can diversify dependency.

Competitive Landscape

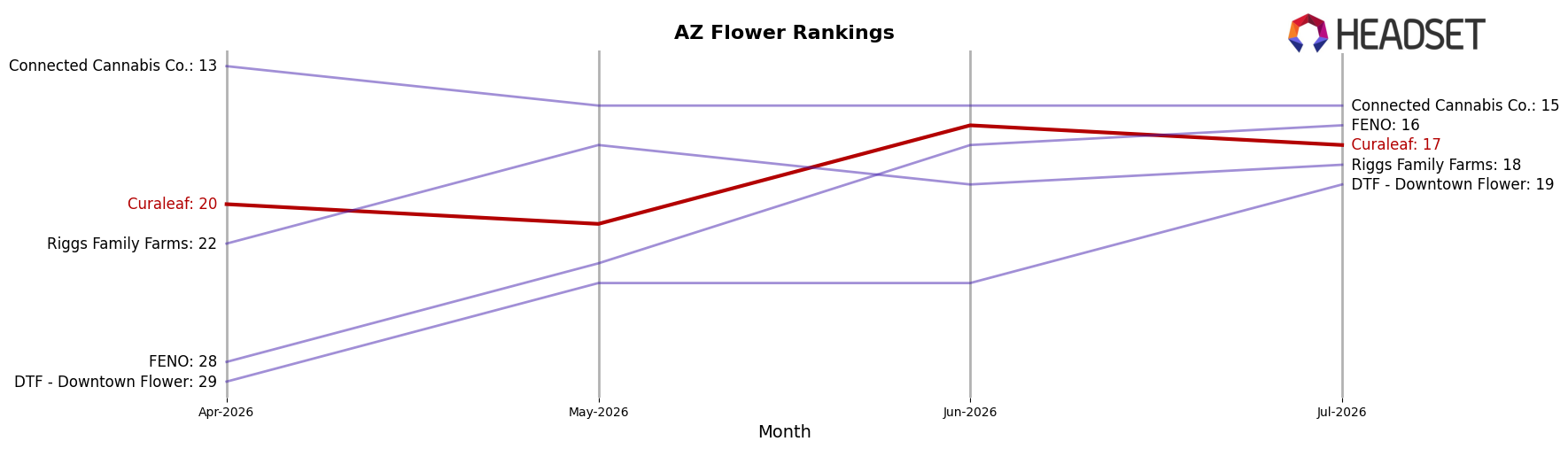

Curaleaf sits at rank 17 in July 2026, improving 6 positions year over year and rising 3 places from rank 20 in April 2026, while still far from its peak at rank 5 in September 2025; meanwhile, Just Flower holds rank 1 with a 1-position YoY climb and 21.8% sales growth, and Fenix is at rank 5 with a 1-position YoY drop and a 6.9% sales decline, indicating Curaleaf’s mid-pack ascent is occurring as the top tier both consolidates gains and sheds weaker momentum. The combination of a 6-rank YoY lift and a 3-rank quarter-to-date move implies Curaleaf is regaining share from lower tiers but must close a 12-rank gap to its September 2025 peak to signal durable category re-entry.

Notable Products

White Hot Guava (14g) posted the steepest decline in July 2026 at -40.18% while sliding to rank 4, even as the same strain’s White Hot Guava (3.5g) surged +49.63% to rank 1 with $94,593 in sales. Atomic Breath (3.5g) fell -21.75% to rank 2, and Classic Bites - Raspberry Gummies 10-Pack (300mg) dropped -21.52% at rank 9, while Classic Bites - Watermelon Gummies 10-Pack (300mg) climbed +34.36% to rank 3. Six of the top ten SKUs are Flower, but the mixed direction across sizes and formats suggests Curaleaf is reallocating demand from larger Flower packs into premium eighths while Edibles absorb replenishment-driven gains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.