Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Shango is stocked at 73 licensed dispensaries across Arizona, Florida, and 2 other states, 52 of them in Arizona, with the deepest coverage in Phoenix, Mesa, Chandler, Glendale, and Tempe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

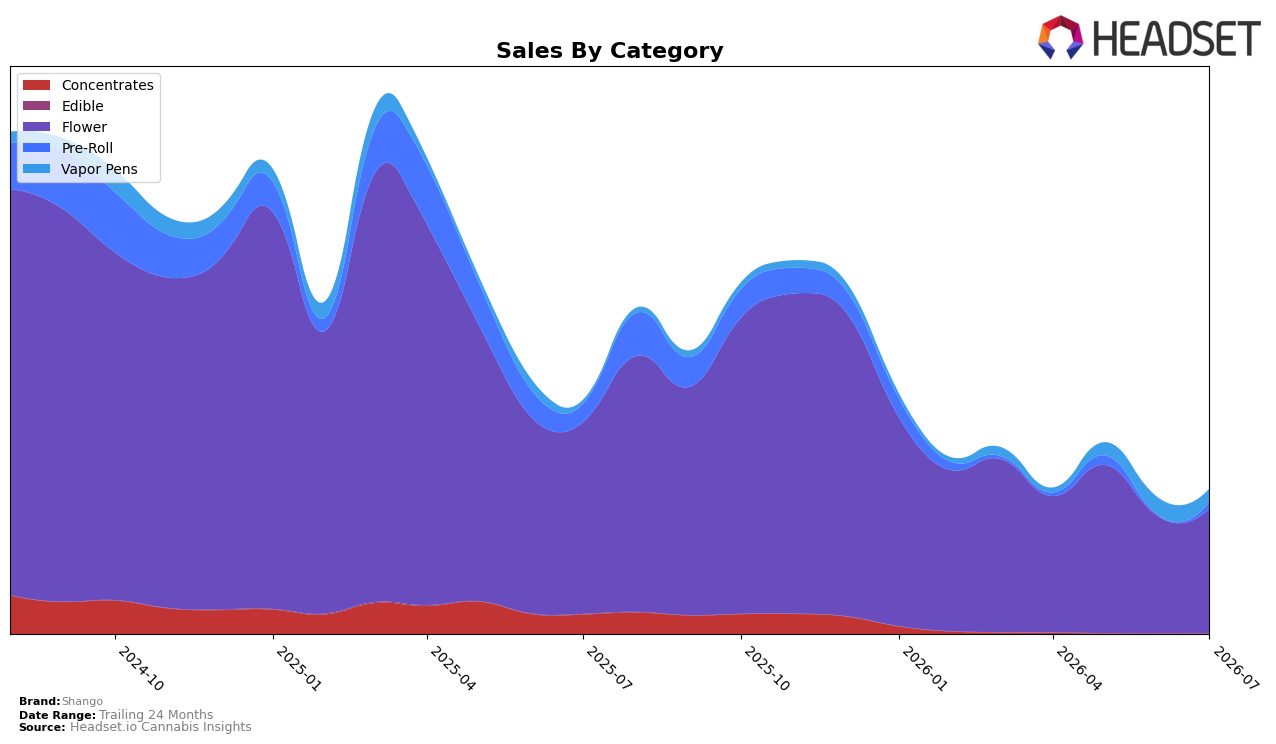

In July 2026, Shango concentrated 86.56% of sales in Flower with a 6.65% month-over-month lift but a 35.08% year-over-year decline, while Vapor Pens held 9.12% share on a 23.75% MoM drop despite a 288.76% YoY surge. Pre-Roll jumped 698.70% MoM to 4.29% share even as it fell 66.32% YoY, and Concentrates slid 52.80% MoM to 0.03% share alongside a 99.80% YoY contraction. With overall brand sales down 38.23% YoY and average price down 40.14% YoY, this category mix indicates a pivot toward lower-priced Flower volume with opportunistic rebounds in Pre-Roll, implying a trade-down environment shaping July 2026 performance.

Positionally, reliance on Flower at 86.56% share alongside a 6.65% MoM rise but 35.08% YoY drop suggests short-term stability from core SKUs while longer-term erosion persists, and the 23.75% MoM pullback in Vapor Pens after a 288.76% YoY spike signals volatile, promotion-sensitive demand rather than durable penetration. The 698.70% MoM surge in Pre-Roll against a 66.32% YoY decline points to tactical inventory or pricing moves that can flex share quickly but do not yet offset the 38.23% YoY brand contraction, implying Shango is competing primarily on value and needs broader category balance to sustain rank 20 in Flower in Arizona.

Competitive Landscape

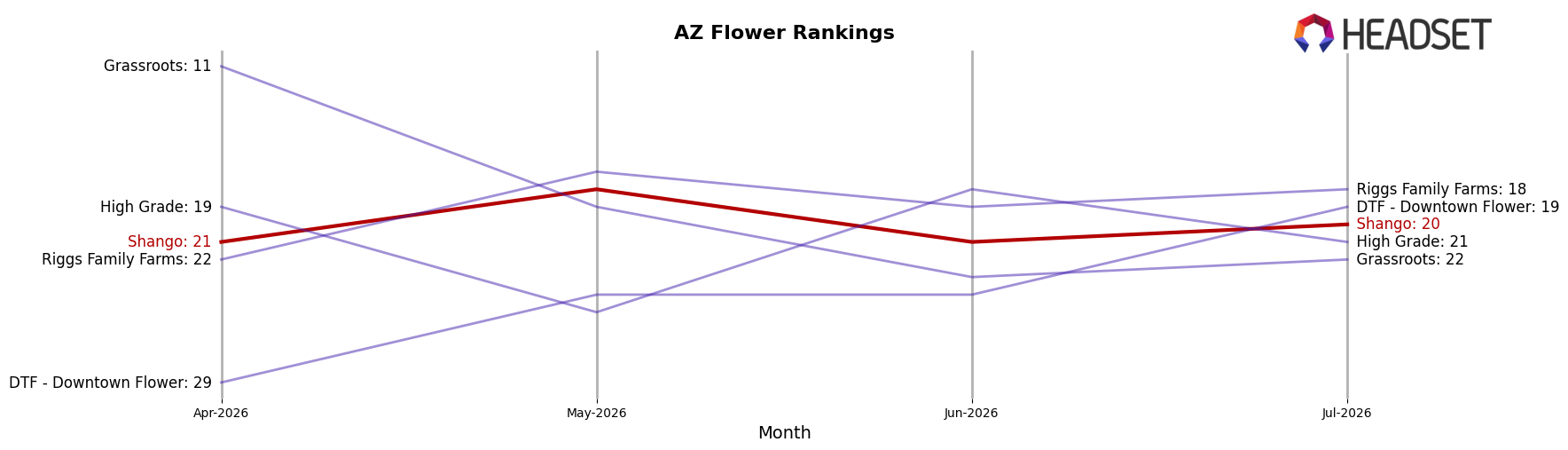

Shango sits at rank #20 in July 2026 in AZ Flower, down 4 positions from #16 in July 2025, while it moved up 1 spot from #21 in April 2026, indicating short-term stabilization amid a year-over-year slide; against this backdrop, Just Flower held #1 year-over-year with a 21.8% sales increase, and Brown Bag advanced from #5 to #4 with 79.0% growth as Fenix slipped from #4 to #5 with a -6.9% decline, signaling that Shango’s path from a peak of #4 in March 2025 to #20 now implies share has migrated to faster-rising value and incumbents, requiring a tactical pivot toward segments where rank erosion can be arrested and near-term gains converted into durable positioning.

Notable Products

Anslinger's Demise Shake (14g) posted the steepest movement in July 2026, dropping -21.3% month over month while sitting at rank 1, and LCG x QTS Shake (14g) in rank 5 inched up +3.4%, signaling volatility at the top of a concentrated lineup. With five shake SKUs inside the top ten and ranks clustered at 1, 3, 5, 6, and 9, the shake format anchors demand even as its lead SKU contracts, while Flower eighths like Acai (3.5g) at rank 2 provide balance without outsized growth. The presence of Goldenstate Duck Pre-Roll (1g) only at rank 10 and with $4,271 in sales indicates limited diversification into Pre-Roll relative to Flower dominance. Net effect: Shango’s mix is consolidating around value-driven shake formats, implying a price-sensitive strategy that trades premium breadth for volume efficiency.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.