Where to Buy

Daybreak Cannabis is stocked at 94 licensed dispensaries across Missouri, Georgia, and Oklahoma, 76 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Columbia, Kansas City, and St Peters. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

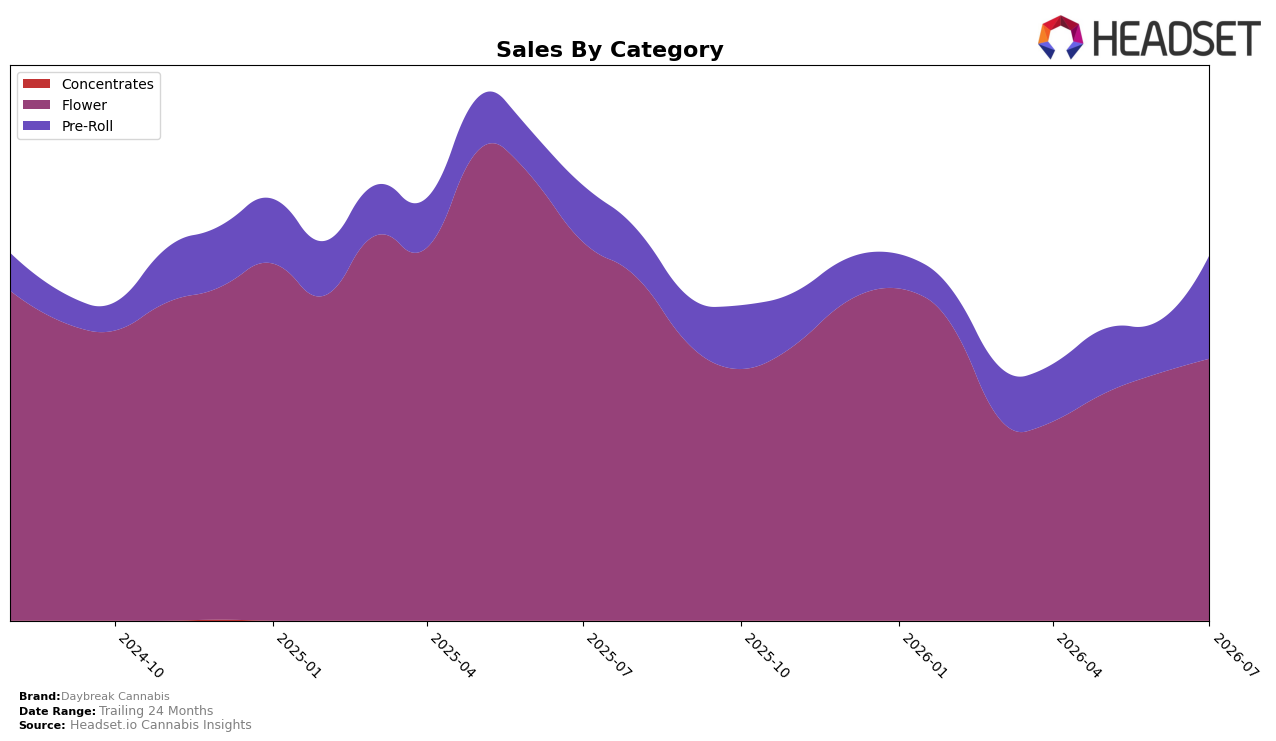

Daybreak Cannabis concentrated 71.73% of July 2026 sales in Flower, with Pre-Roll rising to 28.27% share; within this mix, Flower declined 30.83% year over year while Pre-Roll expanded 83.08% YoY, and month over month Flower grew 6.00% as Pre-Roll surged 99.41%. Despite a 14.14% YoY drop in average price alongside a 16.07% YoY sales decline, category momentum skewed toward value-accessible formats: Pre-Roll’s average price at $11.21 contrasted with Flower’s $39.69, indicating shoppers traded into lower-ticket units as Pre-Roll’s share nearly doubled MoM and Flower maintained the lead by volume; the pattern implies mix-led cushioning of revenue pressure even as higher-priced units contracted.

With Daybreak Cannabis ranked 11 in Flower in Missouri and Flower still the top category, the 6.00% MoM lift in Flower alongside a 99.41% MoM spike in Pre-Roll suggests a pivot toward volume capture rather than premium pricing, reinforced by the 14.14% YoY average price decrease. Given brand sales down 16.07% YoY and 26.77% over 24 months while Pre-Roll expanded 83.08% YoY and Flower fell 30.83% YoY, the positioning implication is a defensive shift toward accessible, higher-frequency products to stabilize share, with the July mix implying that sustained Pre-Roll growth is now the primary lever to offset pressure in higher-priced Flower while preserving a top-15 foothold in the core category.

Competitive Landscape

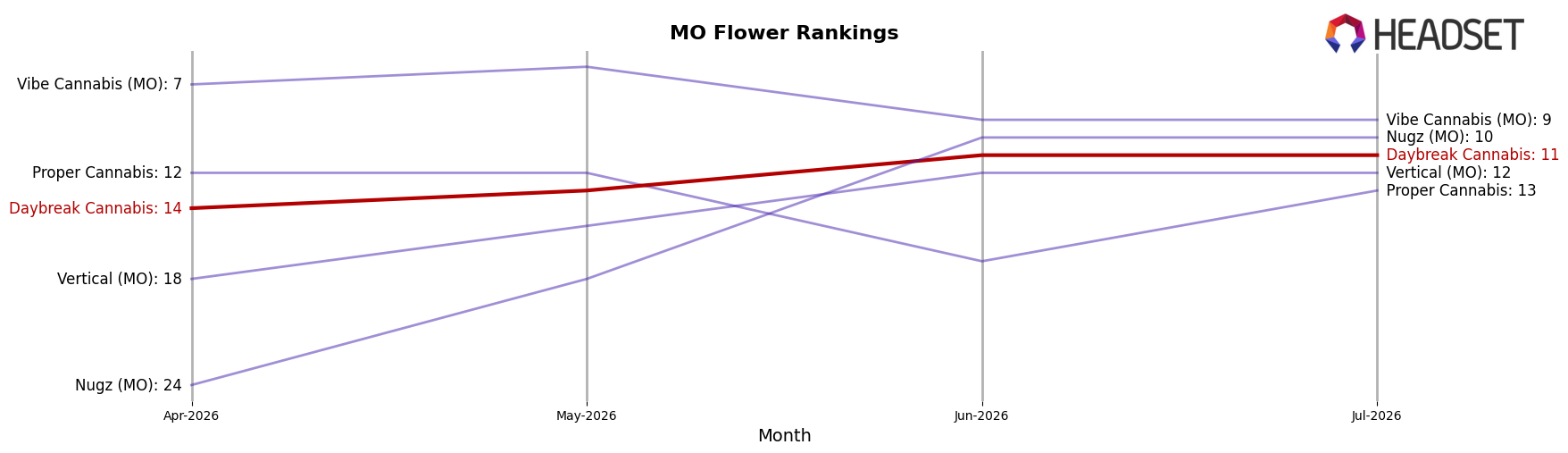

Daybreak Cannabis is currently ranked #11 in MO Flower in July 2026, down 4 positions year over year from #7, and up 3 places from April 2026 when it sat at #14; compared to its peak at #7 in July 2025, the brand is now 4 ranks lower while category leaders like Flora Farms held #1 with a 1.25% YoY sales decline and Local Cannabis Co. advanced from #10 to #5 alongside 41.83% YoY sales growth. With Sinse Cannabis moving from #4 to #2 on 8.99% YoY growth and Amaze Cannabis rising from #6 to #4 with 20.59% YoY growth, Daybreak Cannabis’s relative slippage despite a recent 3-rank quarter-over-quarter lift indicates share consolidation among faster-rising competitors and implies that holding a top-10 position will require outpacing double-digit movers rather than incremental gains.

Notable Products

Triangle Kush Pre-Roll (1g) posted the steepest decline at -28.8% while sliding to rank 5 in July 2026, and Biscotti Pie #6 Pre-Roll 2-Pack (1g) fell -14.5% at rank 4, signaling near-term volatility in single-count pre-rolls. Supremium Pre-Roll (1g) was a counterpoint with +11.8% at rank 6, yet six of the top ten are Pre-Roll SKUs concentrated in both singles and 10-packs, indicating the category still anchors visibility despite mixed momentum. Melted Strawberries Pre-Roll (1g) led at rank 1 and California #10 Pre-Roll (1g) held rank 3, while higher-ranked bulk Flower like Permanent Marker (Bulk) at rank 7 and Guava Bomba (Bulk) at rank 9 concentrate volume with fewer units, pointing to a barbell mix between premium pre-roll visibility and bulk flower throughput. The pattern implies Daybreak Cannabis is leaning into a two-speed strategy where pre-rolls drive shelf presence and trial, while bulk flower absorbs spend and stabilizes revenue.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.