Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

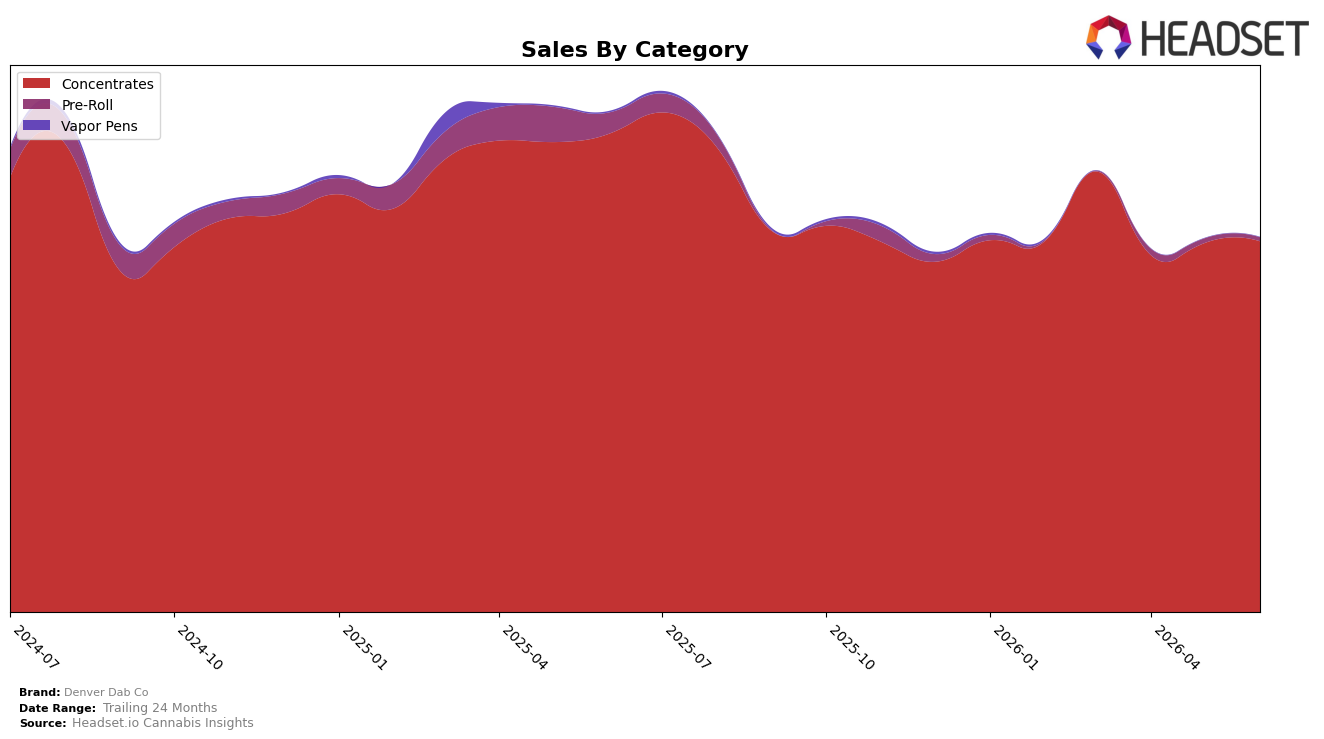

In June 2026, Denver Dab Co’s mix was overwhelmingly Concentrates at 99.04% share while Pre-Roll held 0.96% share, a consolidation that tightened versus year-over-year declines of 22.44% in Concentrates and 82.79% in Pre-Roll. Month over month, Concentrates inched up 0.48% while Pre-Roll fell 16.09%, aligning with a brand-level average price drop of 14.37% year over year and a brand sales contraction of 25.13% year over year. With Concentrates ranked 10th in Colorado, the category-heavy mix and divergent MoM trajectories imply the brand is leaning further into its core while allowing peripheral exposure to shrink, trading breadth for depth.

The pattern suggests Denver Dab Co is prioritizing share defense within Concentrates over cross-category expansion: a 0.48% MoM lift in the 99.04% pillar offsets little from an 82.79% YoY collapse in the 0.96% satellite, indicating purposeful concentration rather than diversification. Given a 25.13% YoY sales decline against a 14.37% YoY price reduction and a 10th-place Concentrates rank in Colorado, the strategy implies price-led retention within a single category to stabilize rank rather than volume-led recovery via Pre-Roll, signaling a positioning bet on category authority over portfolio breadth.

Competitive Landscape

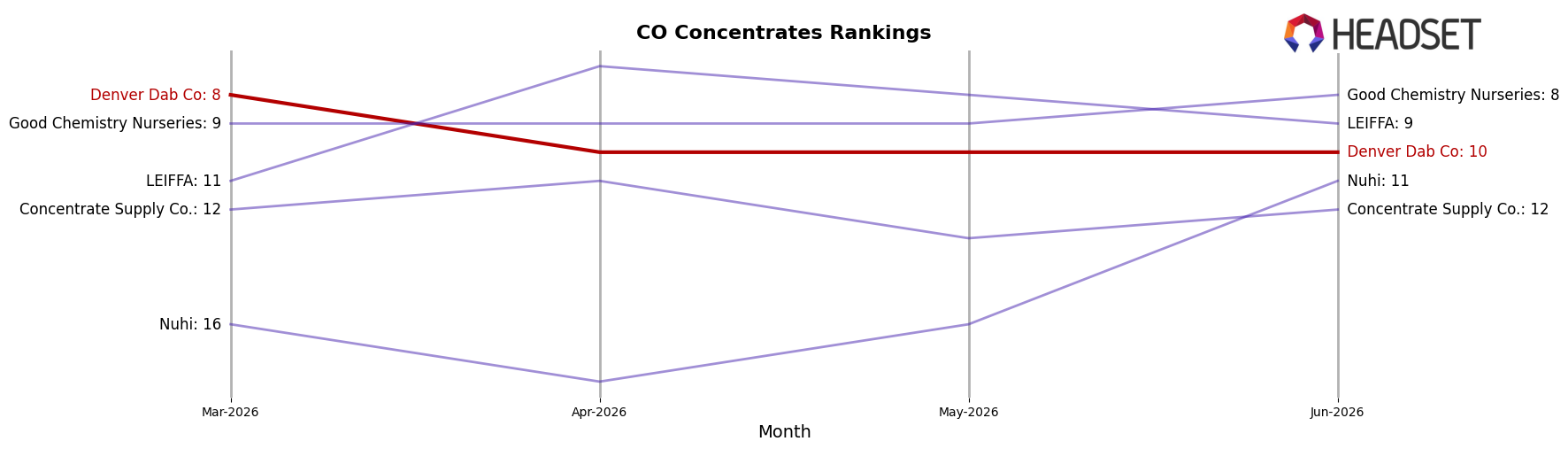

Denver Dab Co ranks #10 in Colorado Concentrates in June 2026, down 3 positions year over year from #7 and 2 spots below its March 2026 mark of #8, while still trailing its peak of #6 from July 2025; in contrast, Amber held #1 with 39.0% YoY sales growth and Nomad Extracts advanced from #5 to #3 with an 18.1% YoY lift, whereas 710 Labs remained #2 despite a -9.9% YoY decline, indicating Denver Dab Co’s rank erosion is less about category contraction and more about under-participation in the growth accruing to faster-moving leaders.

Notable Products

Gary Payton Sugar Wax (1g) delivered the standout move in June 2026 with a +68.9% month-over-month surge and a #2 rank, while Punch Breath Sugar Wax (1g) dropped -37.6% but still held a share of the upper tier at a tied #3 position. Two SKUs occupy the #3 slot, indicating rank compression at the top, and nine of the top ten are Concentrates (including wax and sugar wax forms), signaling a concentrated portfolio around a single format. This mix tells us Denver Dab Co is consolidating demand in wax and sugar wax while tolerating sharper SKU-level volatility to keep the overall category lead.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.