Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Billo is stocked at 40 licensed dispensaries across Colorado, with the deepest coverage in Colorado Springs, Denver, Grand Junction, Aurora, and Thornton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

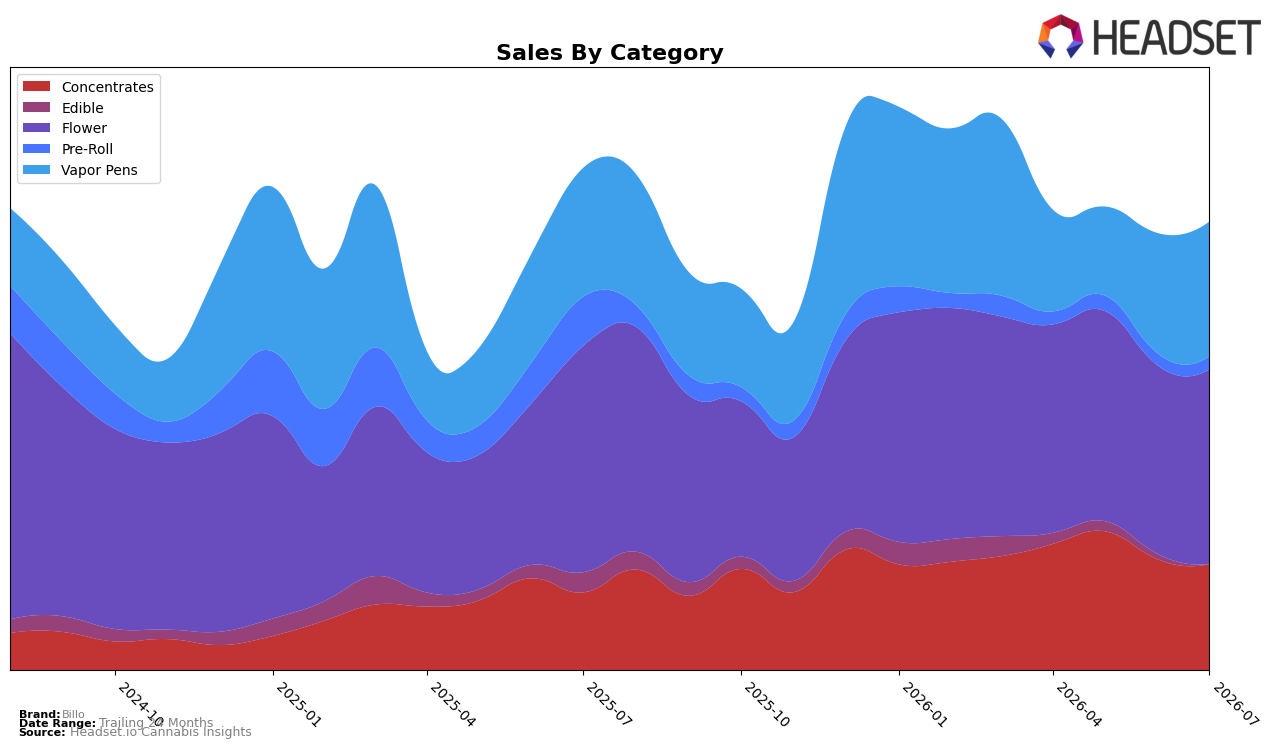

In July 2026, Billo’s mix concentrated in Flower at 43.25% share with a -14.05% year-over-year change but a 3.23% month-over-month lift, while Vapor Pens rose to 29.98% share on 4.49% YoY growth and an 11.72% MoM increase; by contrast, Concentrates reached 23.60% share with 36.28% YoY growth but slipped -4.21% MoM. Peripheral categories contracted sharply, with Pre-Roll at 3.00% share after -72.65% YoY despite an 8.65% MoM uptick, and Edible at 0.17% share after -96.36% YoY and -87.09% MoM. With average price up 20.65% YoY to $20.38 and Flower ranked 19th in Colorado Flower, the pattern implies Billo is leaning into higher-priced core segments while pruning low-scale lines, trading some volume for margin and category focus.

The divergence between Vapor Pens’ 11.72% MoM rise and Concentrates’ -4.21% MoM, alongside Flower’s 3.23% MoM lift and a -10.63% brand sales YoY outcome, implies Billo’s positioning is pivoting toward steady, premium-leaning inhalables rather than breadth across smaller formats. With Flower still the anchor at 43.25% share but facing -14.05% YoY, and Concentrates delivering 36.28% YoY against a monthly pullback, Billo’s near-term edge likely comes from balancing rank-anchored Flower presence (19th in Colorado) with faster-turn Vapor Pens at 29.98% share, using price elevation and mix shift to stabilize revenue despite category-level volatility.

Competitive Landscape

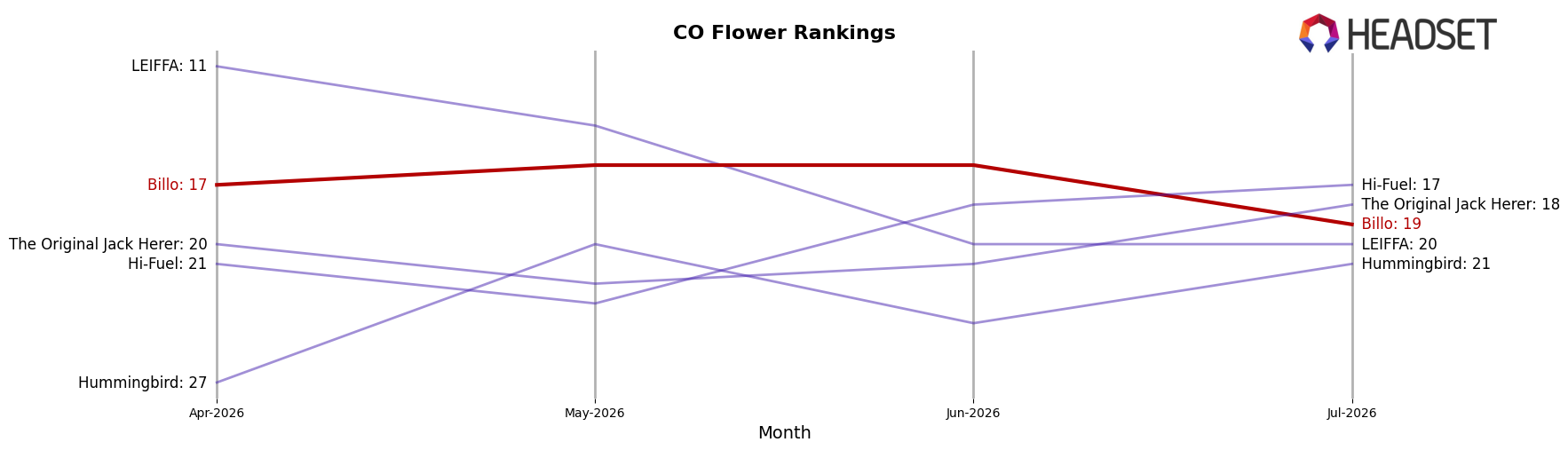

Billo ranks #19 in Colorado Flower in July 2026, down 8 positions year over year from #11, and 2 spots lower than April 2026 when it held #17; the brand’s peak at #7 in January 2026 contrasts with this multi-month slide. In the same July 2026 period, Seed & Strain Cannabis Co. rose from #2 to #1 with 76.23% year-over-year sales growth, while Good Chemistry Nurseries declined from #1 to #3 with an 8.70% sales contraction, indicating that leadership is rotating at the top even as Billo’s position moves from the top 10 to outside the top 15. The pattern implies Billo’s rank trajectory is drifting toward the middle tier, and without a reversal toward January 2026’s #7 level, share will consolidate among faster-rising leaders.

Notable Products

Gorilla Glue #4 (Bulk) posted the standout move in July 2026 with a +181.3% month-over-month surge to rank 1, while Garlic Sherbert (Bulk) fell -19.5% to rank 3, widening the performance gap within Billo’s Flower lineup. With Maple Nectar (Bulk) entering at rank 2 and Lilac Diesel (3.5g) at rank 7, four of the top ten are Flower SKUs, indicating concentration at the category’s top even as Galactic Goldrush Sugar Wax (1g) rose +36.6% to rank 5. The split between a triple-digit gainer at rank 1 and a double-digit decliner at rank 3 signals a deliberate tilt toward bulk Flower velocity, with Concentrates supplying secondary momentum rather than share leadership.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.