Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

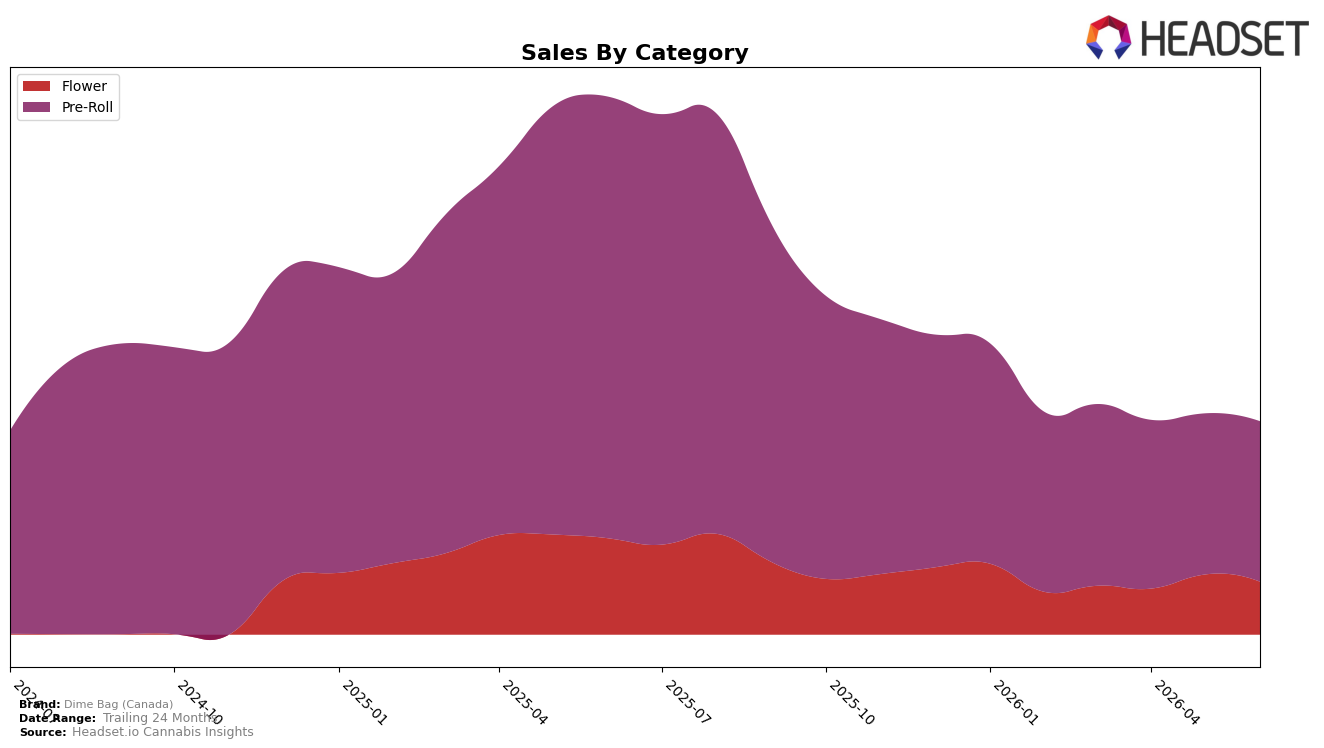

Dime Bag (Canada) derived 75.27% of June 2026 sales from Pre-Roll with a year-over-year decline of 63.72% and a month-over-month dip of 0.42%, while Flower accounted for 24.73% with a 45.21% year-over-year contraction and a sharper 12.00% month-over-month pullback; together these shifts align with a total brand year-over-year sales decline of 60.41%. Average price rose 23.65% year over year to $13.25 as Pre-Roll pricing held lower at $10.32 versus Flower at $96.95, implying mix protection concentrated in lower-priced units even as June 2026 category volumes contracted; the pattern indicates the brand is over-indexed to a declining Pre-Roll base and is using price/mix to offset volume pressure only marginally.

With Pre-Roll concentration at 75.27% and a category rank of 26 in Ontario Pre-Roll, the steeper 63.72% year-over-year drop in that anchor category versus the 45.21% decline in Flower suggests positioning risk tied to a single, weakening demand pool. The slight 0.42% month-over-month slip in Pre-Roll versus an 12.00% month-over-month slide in Flower indicates near-term stability around the core but limited upside, and the 23.65% annual price increase alongside a 24-month sales gain of 43.28% points to a strategy shifting toward fewer, higher-priced units; the implication is that sustaining share will require either diversifying away from Pre-Roll exposure or redefining value within Pre-Roll to climb from rank 26 in Ontario.

Competitive Landscape

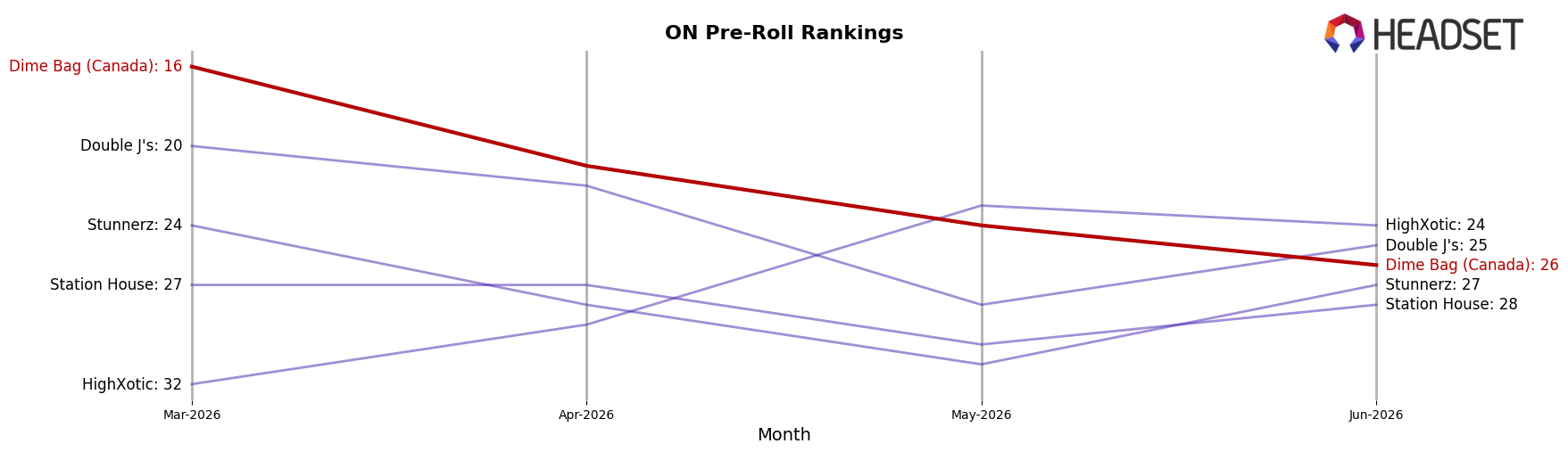

Dime Bag (Canada) sits at rank #26 in ON Pre-Roll in June 2026, down 20 positions year over year from #6, and 10 positions below its March 2026 rank of #16; the brand’s peak at #6 in August 2025 contrasts with today’s lower placement, indicating a multi-quarter slide. Meanwhile, Back Forty / Back 40 Cannabis climbed to #1 with a 3-position YoY improvement and 74.6% YoY sales growth, while General Admission edged up to #2 with a 1-position YoY gain despite a -17.9% YoY sales decline; in contrast, Jeeter rose to #4 with a 2-position YoY improvement even as sales fell -48.5%. This pattern implies Dime Bag (Canada)’s rank trajectory has shifted from a temporary dip to a share-loss trend as faster-moving leaders consolidate top-5 positions.

Notable Products

Doozies Tropical Pocket Puffs Pre-Roll 20-Pack (10g) delivered the standout surge in June 2026 with +132.8% MoM, vaulting into rank 7, while Pocket Rockets- Wildcat Serum Infused Pre-Roll 5-Pack (2.5g) also jumped +123.2% to rank 9; by contrast, Sweet Pocket Puffs Pre-Roll 4-Pack (2g) slid -12.9% at rank 3 and Spicy Pocket Puffs Pre-Roll 4-Pack (2g) fell -11.4% at rank 4. Diesel Pocket Puffs Pre-Roll 4-Pack (2g) held rank 1 with a -1.8% dip and Tropical Pocket Puffs Pre-Roll 4-Pack (2g) rose +1.6% at rank 2, indicating share concentration at the top even as volatility deepens in the mid-tier. Four of the top ten are Pre-Roll Pocket Puffs SKUs, and the entry of a 20-pack format alongside an infused 5-pack suggests a pivot toward value-multipack and potency-led options over single large Flower formats, where Kush Dreams (28g) dropped -13.8% at rank 8 and Purple Poison (28g) declined -5.9% at rank 6. This mix implies Dime Bag (Canada) is shifting commercial emphasis toward diversified Pre-Roll formats that capture both basket-size and trade-up to infused, using multipacks to stabilize rank while Flower cedes momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.