Where to Buy

Discos is stocked at 64 licensed dispensaries across Maryland and Oregon, 57 of them in Maryland, with the deepest coverage in Baltimore, Silver Spring, Hagerstown, Annapolis, and Bethesda. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

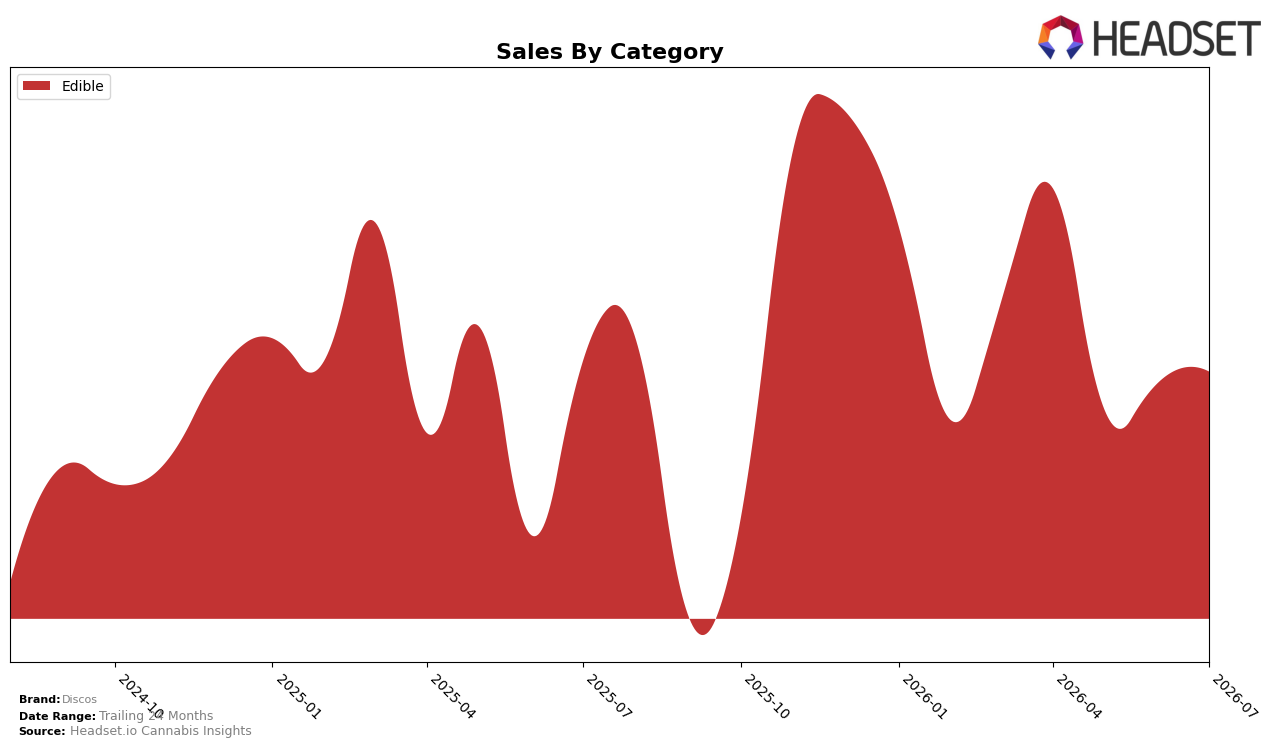

Market Insights Snapshot

In July 2026, Discos operated as a single-category brand with Edible accounting for 100.0% of sales, while Edible sales were down 1.11% year over year and up 1.26% month over month. Average price fell 17.29% year over year to $17.85, and overall brand sales were down 1.11% year over year despite a 23.72% lift versus 24 months prior; the net of these movements is that price compression outpaced unit expansion on a yearly basis but was partially offset by month-over-month velocity. The brand’s top market was Maryland, where Discos ranked 18th in Edible, indicating mid-pack placement alongside a modest 1.26% month-over-month recovery; taken together, the pattern implies the current mix concentrates all execution risk and opportunity in Edibles while near-term momentum is insufficient to reverse the year-over-year contraction.

Positioning-wise, a 100.0% Edible mix combined with a 17.29% year-over-year price decline and an 18th-place rank in Maryland suggests a value-leaning stance competing on accessibility rather than premium cues, with the 1.26% month-over-month sales lift indicating price-led trial more than durable share capture. With total brand sales down 1.11% year over year but up 23.72% over 24 months, the trajectory implies longer-cycle recovery potential if price elasticity continues to convert, yet the single-category exposure amplifies volatility risk unless rank advances from 18 to the mid-teens or price stabilizes within a low double-digit decline range; in short, the pattern implies Discos must translate discount-driven gains into sustained rank improvement to avoid further erosion.

Competitive Landscape

Discos sits at rank #18 in MD Edible as of July 2026, improving 3 positions year over year from #21 to #18, while holding flat versus April 2026 at #18; this places the brand at its peak rank of #18 in July 2026, yet still outside the top 15. In contrast, Incredibles advanced from #3 to #1 alongside a 26.0% YoY sales gain, and Wyld slipped from #1 to #4 with a -18.0% YoY sales change—indicating the upper tier remains fluid while mid-tier mobility is modest. The pattern implies Discos’ move from #21 to #18 and stasis at #18 across the last three months signal a ceiling effect: incremental rank gains likely require leapfrogging stagnating leaders rather than relying on background category churn.

Notable Products

CBD/THC/CBN 5:1:1 Wild Cherries Gummies 10-Pack (500mg CBD, 100mg THC, 100mg CBN) led July 2026 but slid 12.7% month over month while holding rank 1, and Sour Watermelon Live Resin Gummies 10-Pack (100mg) fell 17.3% at rank 5. In contrast, Milk Chocolate Bites 10-Pack (400mg) climbed 30.5% into rank 8 and Strawberry Live Resin Gummies 10-Pack (400mg) rose 22.8% at rank 9, indicating heavier-dose 400mg formats are gaining traction versus several 100mg gummies that declined 13.0% to 17.3%. With eight of the top ten in Edibles and multiple Live Resin Gummies spanning ranks 3 through 5 and 9, the assortment tilts toward gummies even as chocolate formats with higher potency rise, implying Discos is pivoting its product mix toward potency-tier diversity within Edibles rather than chasing a single flavor-led strategy.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.