Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Evermore Cannabis Company is stocked at 115 licensed dispensaries across Maryland and Oklahoma, 113 of them in Maryland, with the deepest coverage in Baltimore, Annapolis, Columbia, Hagerstown, and Rockville. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

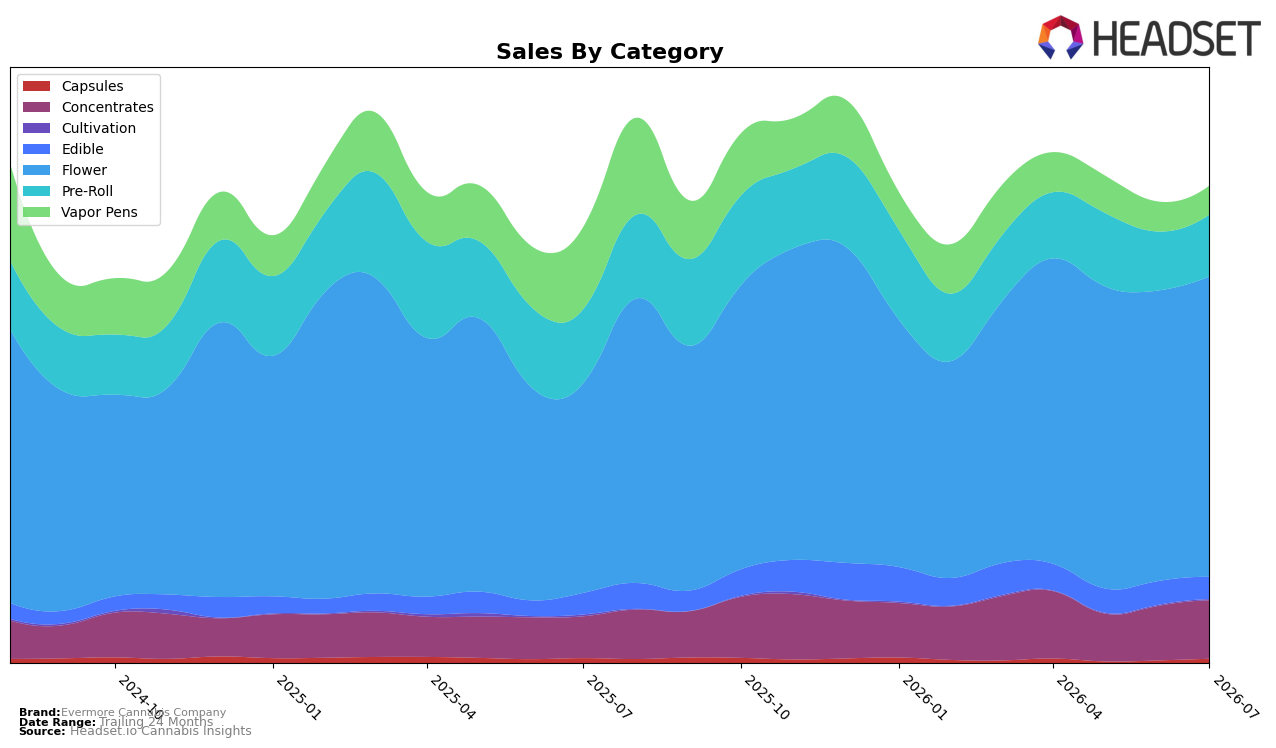

Evermore Cannabis Company concentrated 62.63% of July 2026 sales in Flower with year-over-year growth of 43.18% and month-over-month growth of 3.38%, while holding rank 6 in Flower within Maryland. Concentrates rose 39.11% YoY and 7.28% MoM to 12.31% share, whereas Pre-Roll fell 16.29% YoY despite a 4.82% MoM uptick to 13.03% share, signaling a pivot toward inhalables with higher growth velocity in Flower and Concentrates relative to Pre-Roll.

Vapor Pens contracted 64.08% YoY and 3.20% MoM to 6.19% share while Edible slipped 6.14% MoM despite a 3.19% YoY gain, suggesting portfolio de-emphasis in non-flower inhalables and ingestibles. With Capsules jumping 49.89% MoM but down 10.99% YoY to 1.06% share and the brand’s overall average price down 6.82% YoY to $29.75, the configuration points to a value-leaning, Flower-led stance that can support July 2026 brand sales growth of 9.63% YoY but may cap upside without renewed momentum in Vapor Pens.

Competitive Landscape

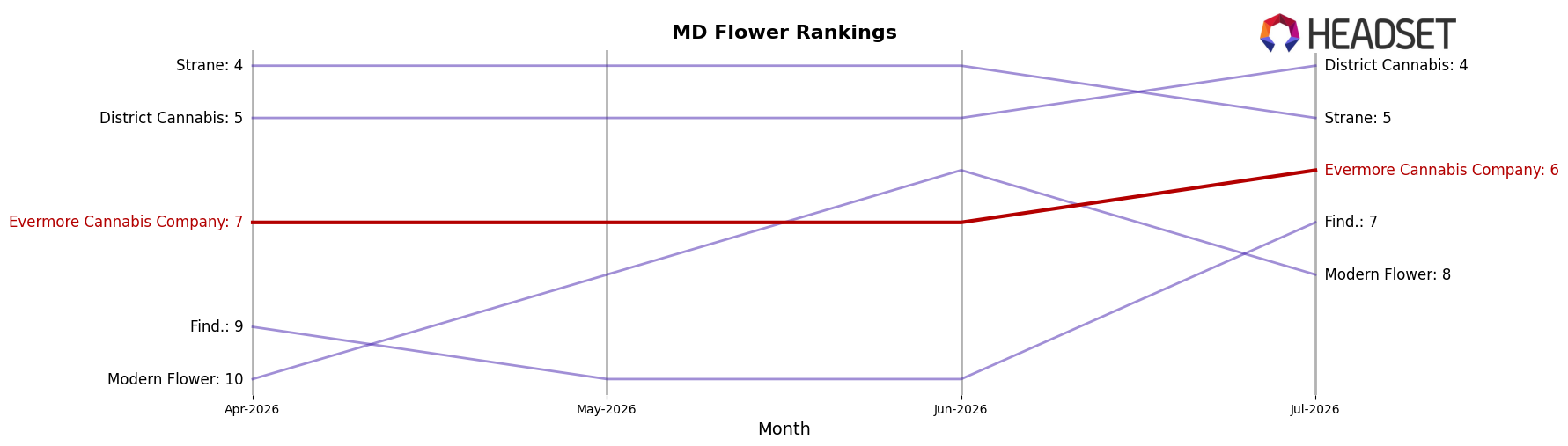

Evermore Cannabis Company sits at rank #6 in MD Flower in July 2026, an upward move of 7 positions from #13 year over year, and a 1-rank gain from #7 in April 2026; however, it remains one slot below its peak of #5 from December 2025 and trails SunMed, which held #1 both this year and last, while RYTHM advanced from #3 to #2 with 47.9% YoY sales growth, and Strane moved from #8 to #5 with 82.3% YoY growth; the pattern—steady climb but ceding ground to faster risers—implies Evermore’s trajectory is improving but risks being capped near the mid‑top tier unless it accelerates gains against peers advancing multiple ranks in the same period.

Notable Products

Orange Drizzle (3.5g) posted the standout surge in July 2026 with a month-over-month gain of 43.99% while climbing to rank 5, contrasted against Rainbow Push Pop #4 (3.5g) slipping 5.41% yet holding rank 1. Patapeake Shortbread (3.5g) advanced 37.16% to rank 2, and Sunset Octane (3.5g) added 17.66% at rank 4, indicating Flower now anchors positions 1 through 5 as four of the top ten are Flower SKUs. Midnight Circus (3.5g) rose 29.25% at rank 9, and Pre-Roll entrants lacked visible momentum with Happy J's - Funky Guava Pre-Roll 2-Pack (1g) debuting at rank 3 without a comparable prior baseline and Sunset Octane Pre-Roll 2-Pack (1g) up 29.33% but capped at rank 6. The pattern implies Evermore Cannabis Company is consolidating around mid-tier Flower velocity spikes while tolerating modest erosion at the flagship, signaling a push to broaden the Flower bench rather than concentrate volume in a single hero SKU.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.