Market Insights Snapshot

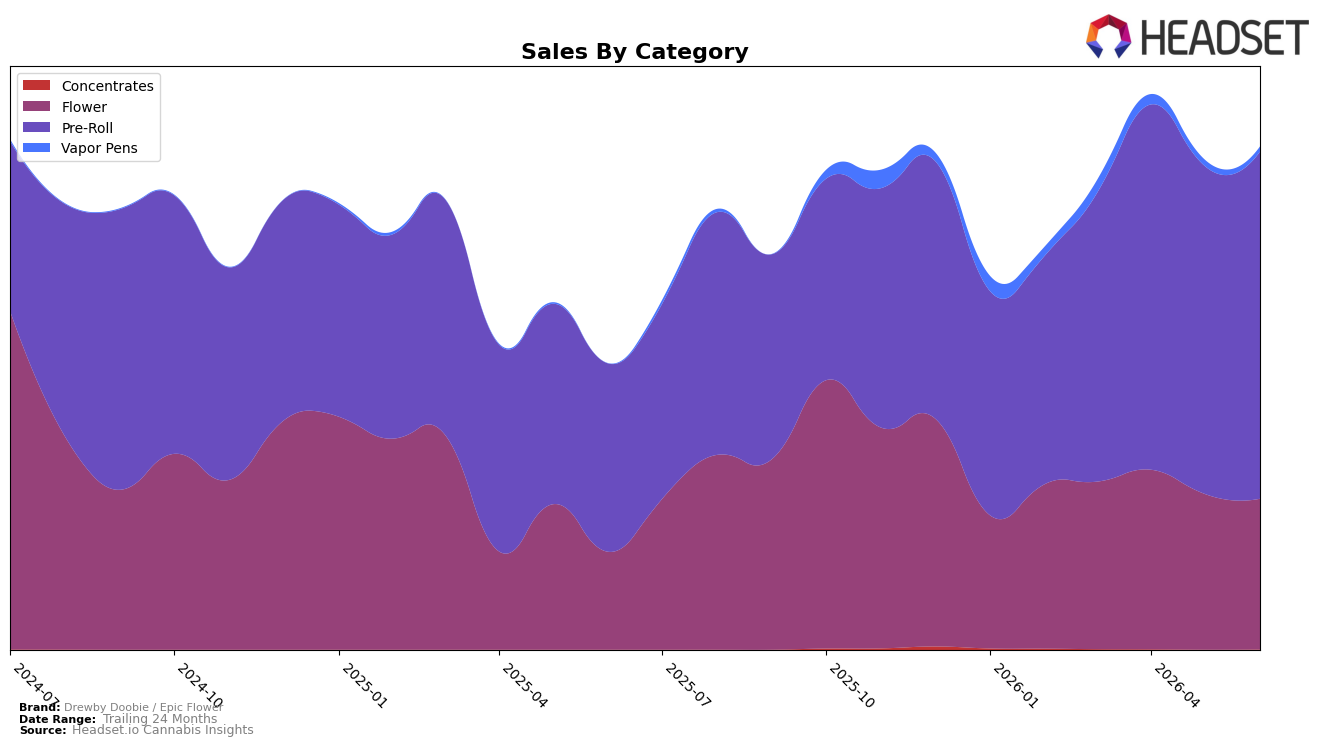

In June 2026, Drewby Doobie / Epic Flower concentrated 69.05% of sales in Pre-Roll with year-over-year growth of 84.49% and month-over-month growth of 5.84%, while Flower carried 29.95% share with 54.19% YoY but a -3.25% MoM slide; Vapor Pens held 0.97% share with a -20.05% MoM decline, and Concentrates were 0.04% with no MoM read. The brand’s average price rose 0.96% YoY to $14.45 as category price points split, with Pre-Roll at $12.27 versus Flower at $23.82, implying the expanding, lower-priced Pre-Roll mix is driving the 75.91% YoY brand sales gain but capping further near-term price-led upside.

With Pre-Roll as the top category and a rank of 13 in Oregon Pre-Rolls, the 5.84% MoM lift in Pre-Roll alongside a -3.25% MoM in Flower indicates the brand is leaning into volume over premiumization, reinforced by Pre-Roll’s 69.05% share versus Flower’s 29.95%. This mix shift, paired with a 0.96% YoY average price increase and a 24-month sales lift of 34.90%, implies positioning as a value-forward Pre-Roll player where incremental share gains are more likely to come from distribution and pack architecture than pricing power.

Competitive Landscape

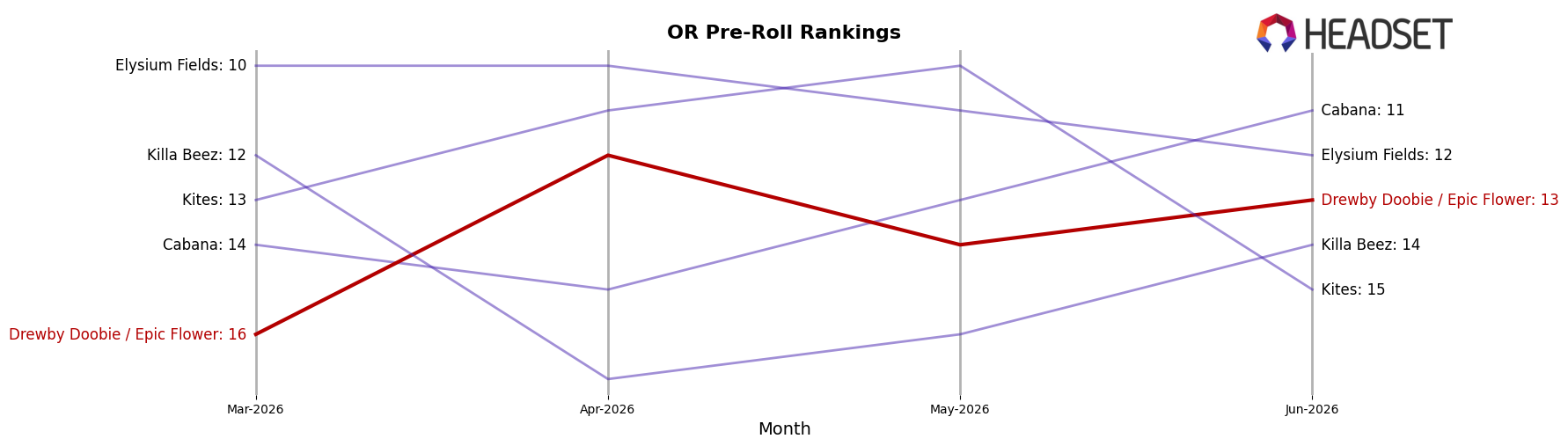

Drewby Doobie / Epic Flower sits at rank #13 in Oregon Pre-Roll for June 2026, improving 16 positions from #29 year over year, and up 3 spots from #16 in March 2026; however, it remains one position below its peak rank of #12 reached in April 2026. In contrast, STiCKS moved from #2 to #1 while growing sales 164.98% year over year, and Kaprikorn climbed from #5 to #2 with 113.36% sales growth, whereas Portland Heights slipped from #3 to #4 alongside a 26.34% sales decline. The pattern implies Drewby Doobie / Epic Flower’s rank momentum is positive but may be capped near the low teens unless it accelerates relative gains against leaders that are posting triple-digit growth.

Notable Products

Supreme Lee Hi Pre-Roll 10-Pack (5g) posted the steepest decline in June 2026, down 33.4% MoM while sitting at rank 9, and Gorilla Breath Pre-Roll 10-Pack (5g) also contracted 25.8% MoM at rank 2, indicating demand compression at both the high and lower ends of the leaderboard. In contrast, Punch Breath Pre-Roll 10-Pack (5g) slipped 10.8% MoM at rank 8 and Headlights Pre-Roll 10-Pack (5g) eased 4.9% MoM at rank 3, pointing to milder pullbacks among mid-ranked staples. Eight of the top ten are Pre-Roll SKUs, with White Chocolate Chip Pre-Roll 10-Pack (5g) holding rank 1 and $19,372 in sales, while Jack Herer (3.5g) holds rank 5 as the lone Flower standout, which suggests portfolio concentration is tilting toward multi-pack Pre-Rolls over single-strain Flower. The pattern implies Drewby Doobie / Epic Flower is leaning into volume-driven Pre-Roll formats even as volatility at ranks 2 and 9 signals a need to balance flagship retention with SKU churn management.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.