Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

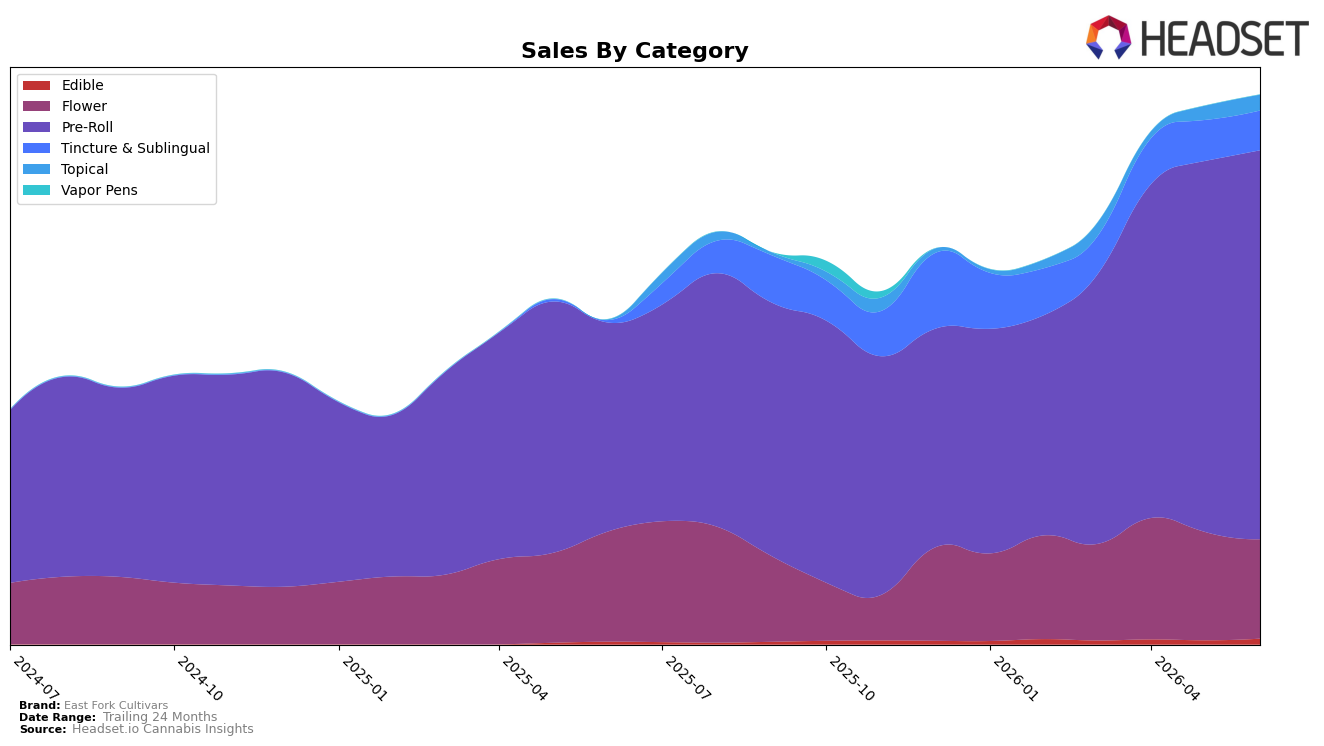

In June 2026, East Fork Cultivars concentrated 70.88% of sales in Pre-Roll, where year-over-year growth reached 86.36% and month-over-month rose 4.87%, while the brand held rank 21 in Pre-Roll within Oregon. Flower contracted to an 18.07% share with a -9.85% year-over-year decline and an -8.34% month-over-month slide, as Tincture & Sublingual expanded to 7.19% share with 1,757.06% year-over-year growth despite a -2.96% month-over-month dip. Smaller lines added momentum: Topical held 2.82% share with 3,612.85% year-over-year growth and 11.84% month-over-month, and Edible reached 1.04% share with 114.48% year-over-year and 40.35% month-over-month gains. The mixture indicates a pivot toward inhalables anchored by Pre-Roll scale, with fast-growing wellness and ingestible niches supplying incremental breadth that can buffer volatility in Flower.

The tilt toward Pre-Roll alongside elevated average price growth of 5.30% and a brand-level 69.42% year-over-year sales increase implies pricing power tied to format preference, while the rank 21 position in Oregon Pre-Roll sets a mid-pack baseline to climb. The simultaneous contraction in Flower (-9.85% year-over-year, -8.34% month-over-month) and outsized surges in Topical (3,612.85% year-over-year, 11.84% month-over-month) and Tincture & Sublingual (1,757.06% year-over-year, -2.96% month-over-month) suggest a barbell: one pole in high-velocity Pre-Roll and another in differentiated wellness formats. The pattern points to a positioning opportunity to leverage Pre-Roll scale to gain distribution while using Topical and Tincture & Sublingual growth to diversify baskets and stabilize seasonality.

Competitive Landscape

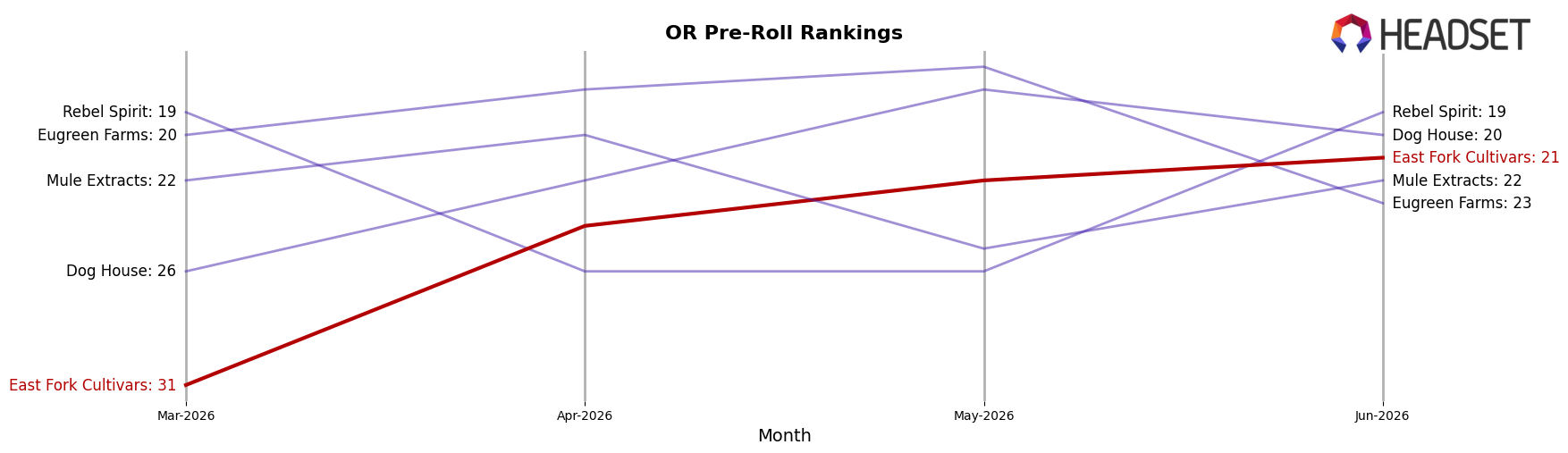

East Fork Cultivars sits at rank 21 in OR Pre-Roll in June 2026, improving 18 positions year over year from rank 39 and jumping 10 spots since March 2026 when it was rank 31; this climb to a new peak rank of 21 in June 2026 contrasts with STiCKS holding rank 1 versus rank 2 a year earlier and Hellavated slipping to rank 3 from rank 1, indicating East Fork Cultivars is gaining relative momentum even as leaders consolidate. With Kaprikorn moving up to rank 2 from rank 5 while Portland Heights fell to rank 4 from rank 3, East Fork Cultivars’ ascent alongside mixed competitor trajectories implies the brand is transitioning from fringe presence toward the competitive middle, with rank volatility suggesting headroom but also pressure to convert rank gains into durable share.

Notable Products

Pineapple Jager Pre-Roll (0.5g) delivered the standout move in June 2026 with a 185.25% month-over-month surge into rank 2, outpacing Create - Jelly Delight Pre-Roll (0.5g) at rank 1 with a 54.56% gain and Relax - Blue Orchid Pre-Roll (0.5g) at rank 3 with a 19.32% rise. Jelly Delight (1g) in Flower slid 30.35% to rank 4 while Pre-Rolls held ranks 1–3 and 5, indicating a shift in shopper preference toward smaller-format inhalables over loose flower.

Across the top ten, six SKUs are Pre-Rolls including a 7-pack offering at rank 10 that still grew 8.07%, while the highest raw sales figure in the set came from Create Jelly Delight Pre-Roll 7-Pack (3.5g) at $15,808. The mix suggests East Fork Cultivars is consolidating around Pre-Roll velocity and bundle formats as primary volume drivers, with single-gram flower absorbing the downside risk.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.