Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

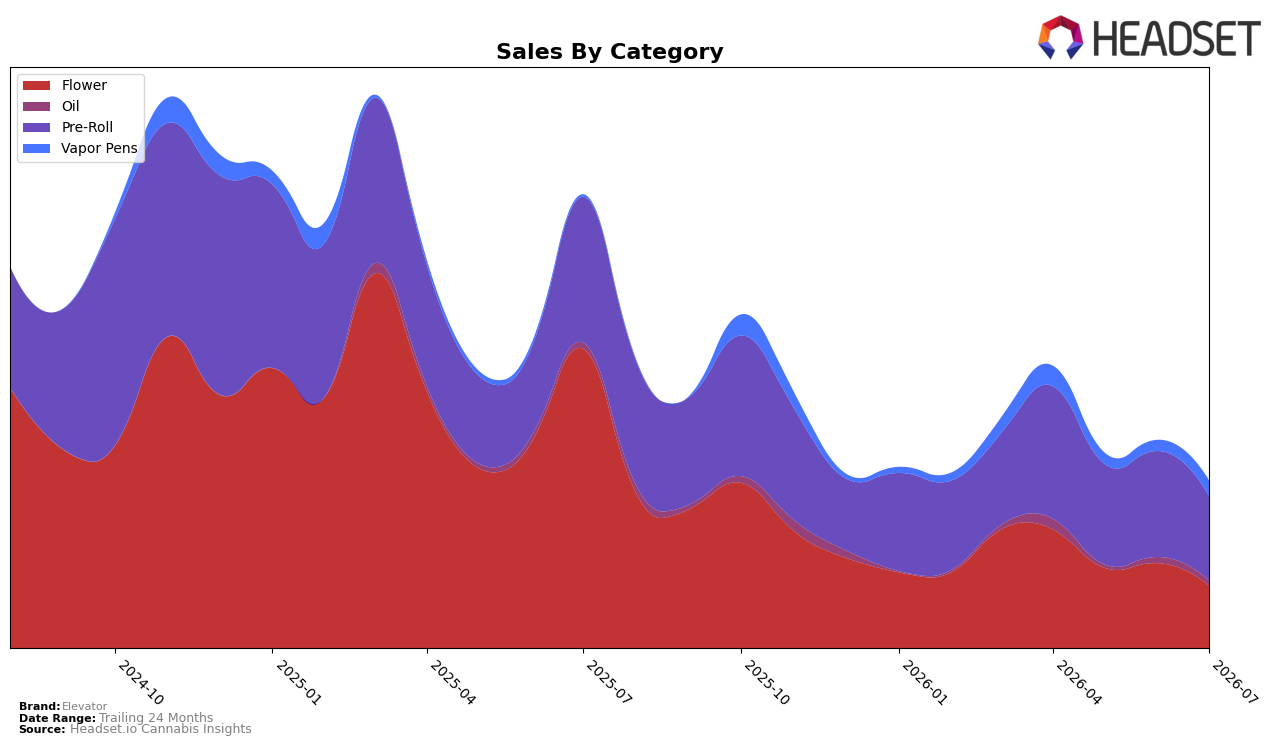

Elevator’s category mix in July 2026 tilted further toward Pre-Roll at 50.7% share with year-over-year sales down 42.1% and month-over-month down 20.2%, while Flower slid to 37.2% share with a 79.3% YoY decline and a 26.8% MoM drop. Vapor Pens expanded to 9.3% share on a 617.3% YoY surge and 42.1% MoM growth, whereas Oil held 2.8% share with an 18.2% YoY decline and 19.8% MoM contraction. With brand-level sales down 63.2% YoY and average price down 37.5% YoY to $16.57, the pattern implies a deliberate pivot away from high-velocity but compressing Pre-Roll and contracting Flower toward a higher-priced, faster-growing Vapor Pens lane, aiming to stabilize mix despite overall shrinkage.

The shift concentrates Elevator’s positioning around value-led inhalables anchored by Pre-Roll rank 14 in Saskatchewan and an emerging Vapor Pens foothold, as the 20.2% MoM Pre-Roll decline alongside a 42.1% MoM Vapor Pens increase suggests reallocation of demand and possibly shelf space. With Flower falling 79.3% YoY while Vapor Pens rose 617.3% YoY, the mix signals pursuit of margin resilience via higher ticket categories (Vapor Pens avg price $34.80 versus Pre-Roll $11.51), implying Elevator is trading assortment toward fewer, higher-value units to counteract price compression and protect rank consistency in Pre-Roll while cultivating a secondary growth pillar in Vapor Pens.

Competitive Landscape

Elevator sits at rank #14 in SK Pre-Roll in July 2026, sliding 4 positions year over year from #10, and down 3 spots since April 2026 when it was #11; this contrasts with Back Forty / Back 40 Cannabis holding #1 both this year and last while growing sales 83.9%, and Doobie Snacks climbing from #8 to #3 with 109.3% YoY sales growth. Despite Elevator’s historical peak at #1 in November 2024 and the category’s mix of gainers like BOLD moving from #3 to #2 (+81.9% YoY) and decliners like Spinach easing from #2 to #5 (-3.2% YoY), Elevator’s multi-period rank erosion implies share is getting redistributed toward faster-rising value and novelty players rather than cyclical volatility, signaling a need to re-anchor assortment or pricing to stem further drift.

Notable Products

Sativa Pre-Roll (0.5g) led July 2026 with a 113% month-over-month jump and the number 1 rank, while Indica Pre-Roll (0.5g) followed with a 101% increase at rank 2. In contrast, Hybrid Pre-Roll 7-Pack (3.5g) fell 60% to rank 7, and Fives Pre-Roll 5-Pack (2.5g) declined 44% at rank 5. With eight of the top ten coming from the Pre-Roll category and only two Flower SKUs present, the pattern implies Elevator is consolidating demand into single-stick formats even as multi-pack volatility introduces risk to sustained share.

Grape Kush (3.5g) advanced 53% to rank 4 and generated $21,953, whereas Indica Pre-Roll 5-Pack (2.5g) slipped 20% to rank 3. The steep 48% drop for Animal House Haze Pre-Roll 10-Pack (5g) at rank 8 alongside two triple-digit gainers at ranks 1 and 2 indicates mix polarization around value and convenience. The pattern implies Elevator’s short-term commercial direction favors high-velocity singles and a selective Flower presence over bulk multi-packs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.