Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

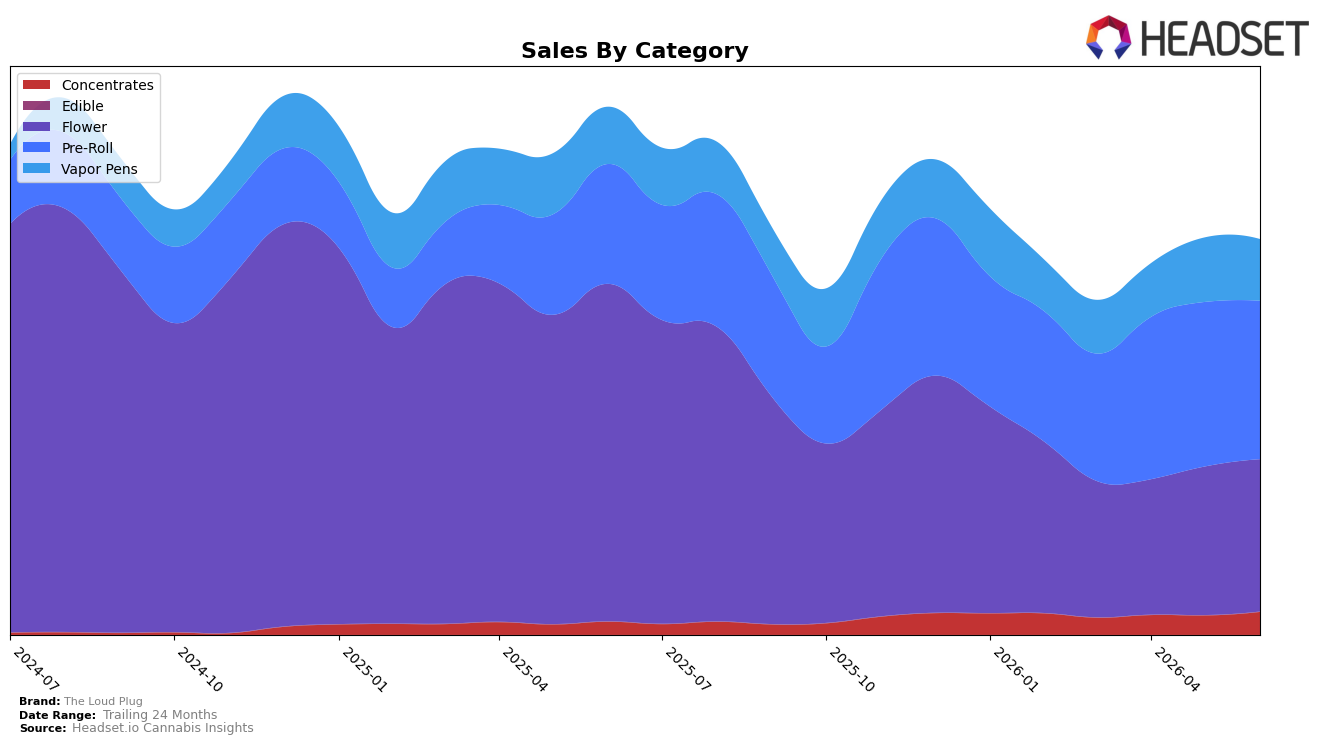

In June 2026, The Loud Plug’s mix tilted toward Pre-Roll at 40.13% share with year-over-year growth of 32.30% but a month-over-month dip of 3.71%, while Flower held 38.56% share with a year-over-year decline of 54.94% and a month-over-month rise of 2.55%. Vapor Pens accounted for 15.56% share, growing 7.78% year over year but falling 4.45% month over month, and Concentrates reached 5.74% share with a 76.95% year-over-year surge and an 18.59% month-over-month gain. Despite overall brand sales decreasing 25.15% year over year and average price falling 14.10%, the category mix is migrating toward faster-growing Pre-Roll and Concentrates, implying a pivot away from Flower is cushioning topline pressure.

Positioning-wise, the brand’s 11th rank in Pre-Roll in British Columbia combined with Pre-Roll’s 32.30% year-over-year growth and Vapor Pens’ 7.78% year-over-year lift suggests the volume engine is anchored in inhalables with lower average prices relative to Flower. The simultaneous 54.94% year-over-year contraction in Flower and 18.59% month-over-month expansion in Concentrates indicates a shift toward potency-driven niches that trade at tighter price points, which, alongside a 3.71% Pre-Roll month-over-month dip and a 2.55% Flower month-over-month uptick, points to near-term share balancing rather than wholesale category exit; the implication is that reinforcing value-tier Pre-Roll while nurturing Concentrates can defend rank trajectory and offset Flower drag.

Competitive Landscape

The Loud Plug sits at rank #11 in June 2026, improving 8 positions from #19 year over year, and rising 3 spots from #14 in March 2026 while also hitting its peak rank of #11 in June 2026; in contrast, Back Forty / Back 40 Cannabis climbed from #22 to #3 with a 263.3% year-over-year sales increase, and General Admission held #1 year over year despite a 18.9% sales decline. Compared with Weed Me nudging from #3 to #2 on a flat 0.1% sales change and Good Supply moving from #8 to #5 with 44.8% growth, The Loud Plug’s steady climb of 8 ranks year over year and 3 ranks quarter to date implies a late-entrance catch-up trajectory where continued incremental share gains are plausible but require outpacing faster risers concentrated in the top five.

Notable Products

Exotic Gas Live Resin Cartridge (1g) posted the steepest decline at -15.4% and slid to rank 2, while Venom OG Live Cured Resin Cartridge (1g) fell -14.3% at rank 3, indicating Vapor Pens lost share against Pre-Rolls. Drippyz Liquid Diamonds & Kief Infused Pre-Roll 5-Pack (2.5g) held rank 1 with only a -1.2% dip and captured the month’s largest dollar volume at $634,334, and four of the top ten are Pre-Roll SKUs including two other Drippyz variants that were down between -1.9% and -13.5%. The pattern implies The Loud Plug is leaning into multi-pack infused Pre-Rolls as the defensible anchor while single-gram Vapor Pens retrench, concentrating the portfolio around higher-repeat, value-forward formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.