May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

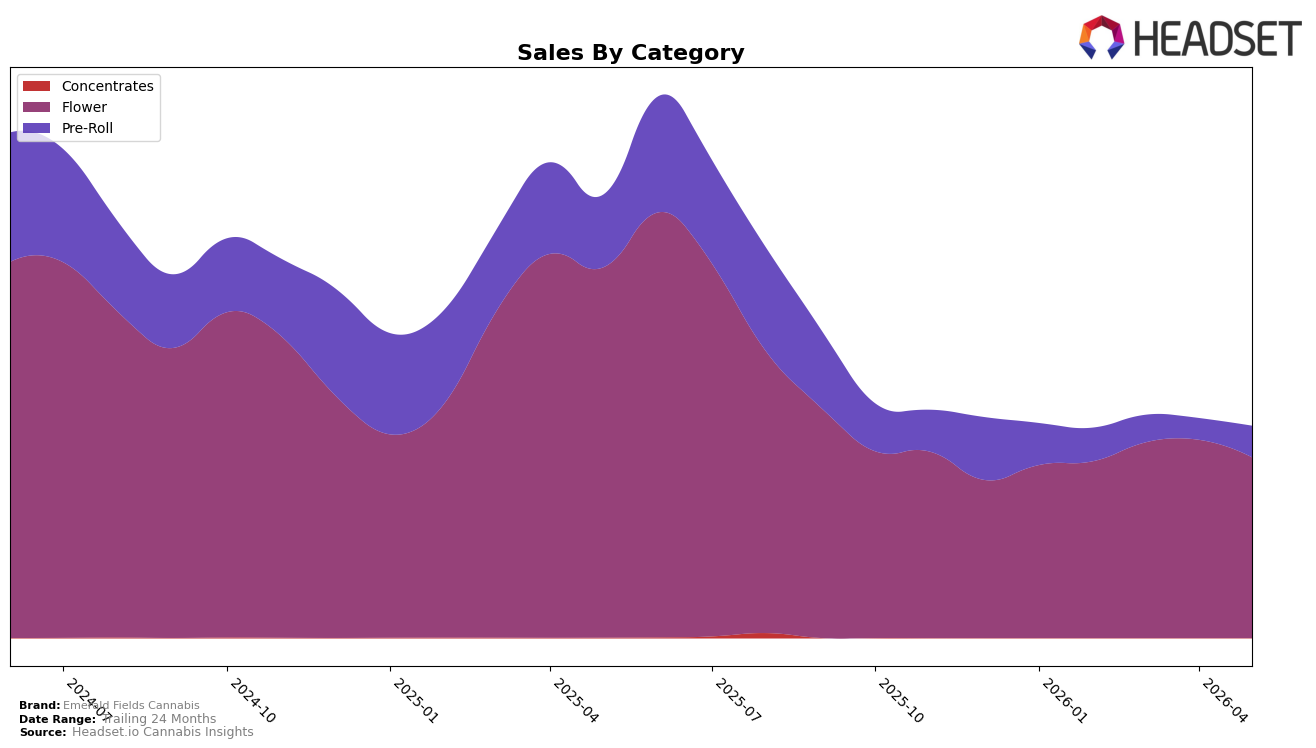

In May 2026, Emerald Fields Cannabis concentrated 85.23% of sales in Flower while Pre-Roll accounted for 14.77%, with Flower down 51.26% year over year and Pre-Roll down 56.85% year over year. Month over month, Flower declined 8.87% while Pre-Roll rose 45.89%, and the brand’s average price fell 27.63% year over year alongside a total brand sales decline of 52.22% year over year. With Flower ranked 11 in Oregon and the overall 24-month sales contraction of 53.56%, the pattern implies a reliance on discounted Flower that is losing velocity while Pre-Roll is emerging as the tactical volume lever despite its smaller base.

The mix shift, where a 8.87% monthly Flower drop coincides with a 45.89% monthly Pre-Roll gain, suggests price-sensitive consumers are trading into lower-ticket formats as the brand’s average price sits at $9.59 and is 27.63% lower year over year. Given Flower’s 85.23% share versus Pre-Roll’s 14.77% share and a Flower category rank of 11 in Oregon, the immediate implication is that defending rank requires stabilizing Flower while using Pre-Roll’s momentum to broaden entry points; the year-over-year sales drops of 51.26% in Flower and 56.85% in Pre-Roll indicate that promotional gains are not yet offsetting structural demand erosion.

Competitive Landscape

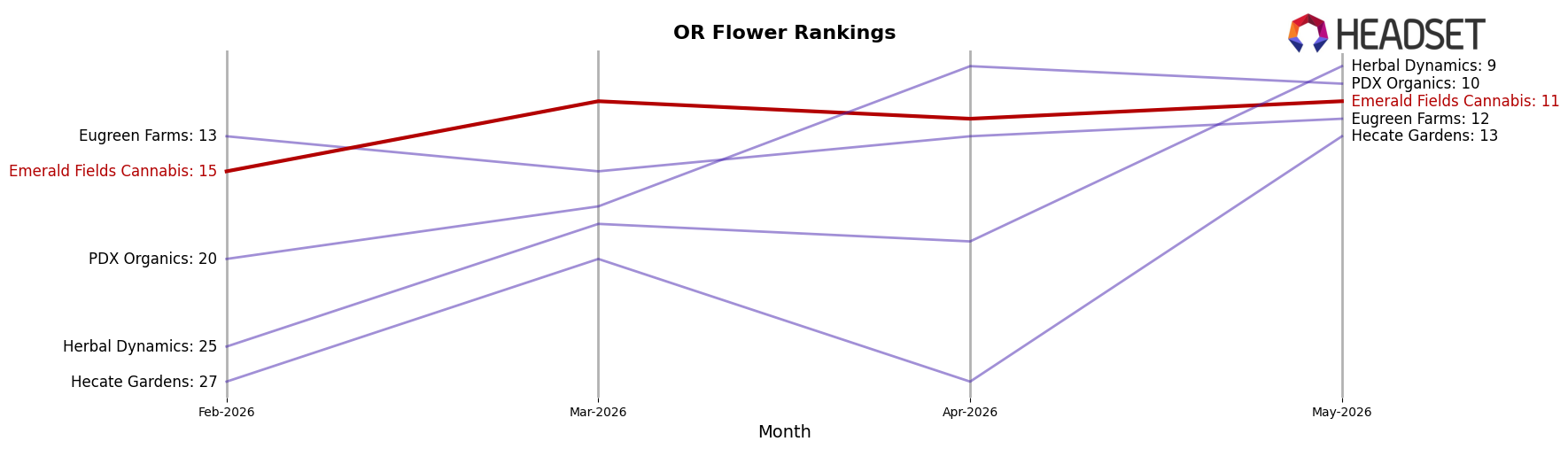

Emerald Fields Cannabis sits at rank #11 in OR Flower in May 2026, a 8-position drop from its #3 spot in May 2025, while improving 4 positions from #15 in February 2026; against this, PRUF Cultivar / PRŪF Cultivar held #1 with a 23.9% year-over-year sales increase and Grown Rogue climbed to #2 from #7 alongside a 51.1% year-over-year gain. The brand’s historical ceiling of #2 in June 2025 contrasts with a current double-digit rank, while Otis Garden moved to #5 from #20 with 101.4% year-over-year growth and Bald Peak holds #3 despite a 12.6% sales decline, indicating Emerald Fields Cannabis faces upward pressure from faster-rising peers and its rank trajectory implies share is being ceded to competitors accelerating faster than its recent rebound pace.

Notable Products

Blueberry Muffin #4 (1g) posted the standout movement in May 2026 with a month-over-month increase of 117.3% and rose into rank 5, while Small Axe Pre-Roll (1g) fell 46.0% to rank 9 and Small Axe Pre-Roll 2-Pack (2g) declined 39.0% to rank 8. Modified Watermelon (28g) grew 46.2% and held rank 7, and four of the top ten are Flower SKUs while four are Pre-Roll SKUs, indicating a split focus across inhalable formats. Blue Sunshine (1g) led at rank 1 with $10,985 while Blue Sunshine Pre-Roll 2-Pack (1g) sat at rank 3, showing brand equity concentrated around the Blue Sunshine line despite Pre-Roll softness at ranks 8 and 9. The mix implies Emerald Fields Cannabis is tilting toward premium Flower velocity and hero-line extensions while legacy Pre-Roll variants face pruning or repositioning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.