Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

PRUF Cultivar / PRŪF Cultivar is stocked at 66 licensed dispensaries across Oregon, with the deepest coverage in Portland, Medford, Coos Bay, Salem, and Bend. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

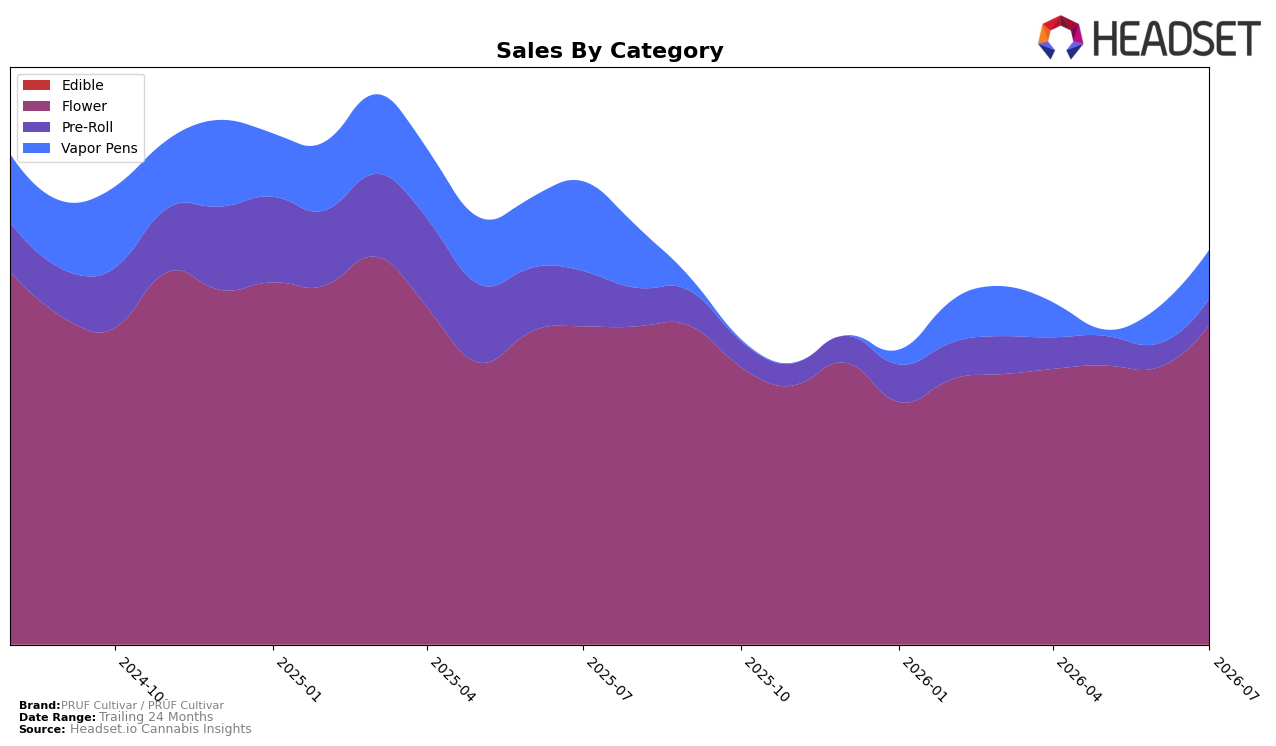

PRUF Cultivar / PRŪF Cultivar concentrated 81.07% of July 2026 sales in Flower, where sales grew 0.51% year over year and 15.45% month over month, while Vapor Pens held 12.30% share with a -45.71% year-over-year change but a 35.59% month-over-month rebound; Pre-Roll accounted for 6.62% share with -52.58% year-over-year and 10.82% month-over-month shifts. Despite a -14.75% brand-level year-over-year sales change and a -24.99% average price change, the brand held rank 1 in Flower in Oregon, implying that July 2026 gains were driven by mix-weighted Flower momentum and price-driven volume elasticity rather than broad category expansion.

The heavier 81.07% reliance on Flower, coupled with rank 1 in Oregon Flower and a 15.45% month-over-month lift there versus a 35.59% month-over-month swing in Vapor Pens, points to a positioning anchored in core Flower leadership with selective re-engagement in Vapor Pens. Given Vapor Pens' -45.71% year-over-year and Pre-Roll's -52.58% year-over-year alongside a -24.99% brand average price change, the pattern implies PRUF Cultivar / PRŪF Cultivar is trading price for volume in its anchor category while keeping adjacent categories as opportunistic plays rather than growth pillars.

Competitive Landscape

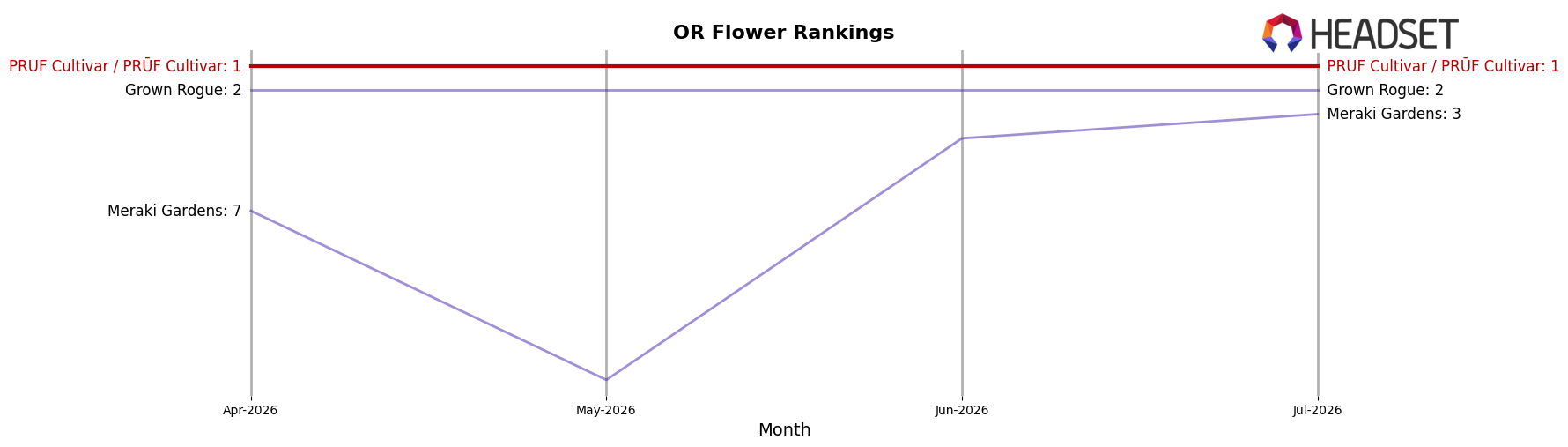

PRUF Cultivar / PRŪF Cultivar holds rank #1 in Oregon Flower with no year-over-year rank change from #1 to #1, and no three-month shift from #1 in May 2026 to #1 in July 2026; meanwhile, Grown Rogue advanced from #3 to #2 year over year while posting a 53.5% sales increase, and Otis Garden jumped from #12 to #4 alongside an 86.2% sales lift, indicating faster momentum among chasers than the category leader. With Meraki Gardens improving from #5 to #3 on 13.6% growth and Bald Peak sliding from #2 to #5 with a 15.5% decline, the competitive set is rotating beneath a stable #1, which implies PRUF Cultivar / PRŪF Cultivar’s flat rank trajectory at the peak is defensible today but increasingly exposed to upward pressure from rapidly climbing rivals.

Notable Products

Sherb n' Runtz (1g) delivered the headline move with a 106.9% month-over-month surge to rank 1, while Velvet Rain (1g) advanced 25.1% to rank 4. Bulk formats clustered across the leader board, with six of the top ten SKUs in Bulk and occupying ranks 2, 3, 6, 7, 9, and 10, indicating volume is consolidating outside single-gram units even as the top spot is held by a 1g SKU. The coexistence of a triple-digit 1g jump at rank 1 and steady Bulk presence within ranks 2–10 implies PRUF Cultivar / PRŪF Cultivar can use a hero 1g to pull trial while maintaining throughput via Bulk, pointing to a dual-track assortment strategy optimized for both basket entry and back-bar volume.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.