Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

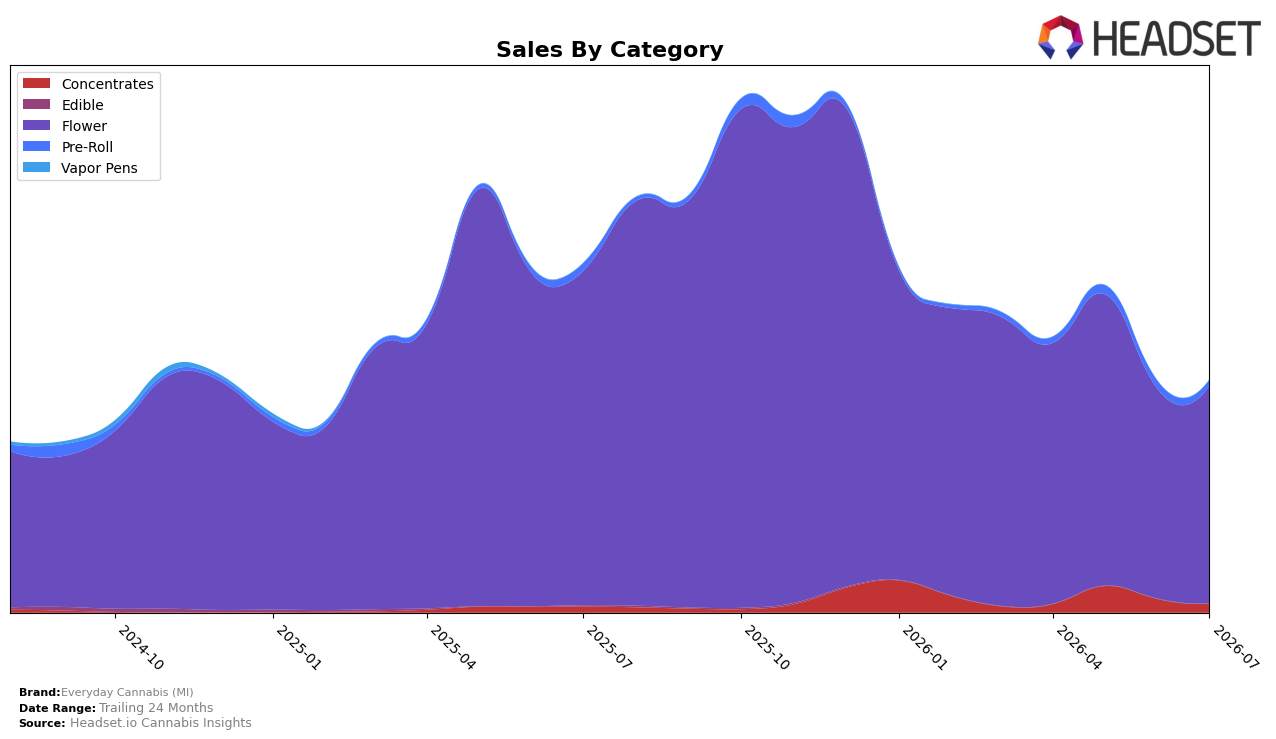

Everyday Cannabis (MI) concentrated 93.79% of July 2026 sales in Flower, with the category down 35.01% year over year yet up 3.87% month over month; in contrast, Concentrates held 3.74% share with a 52.83% YoY increase but a 34.54% MoM decline. Pre-Roll accounted for 2.48% share, sliding 22.28% YoY and 23.22% MoM, while the brand’s overall sales fell 33.49% YoY even as average price rose 36.66%. This mix indicates over-reliance on Flower as a single growth lever in Michigan, with short-term stability masked by category divergence and a rank of 11 in Flower suggesting mid-pack exposure to category volatility.

The shifts imply Everyday Cannabis (MI) is trading higher average price points in Flower (up 36.66% YoY brand-wide pricing against a 35.01% YoY volume/sales contraction in Flower) for near-term revenue defense, while a small but expanding Concentrates line (+52.83% YoY on 3.74% share) offers limited diversification. With Pre-Roll contracting both YoY and MoM and the brand positioned 11th in Flower, the path forward likely requires either deepening value in core Flower to convert the 3.87% MoM uptick into sustained share or reallocating toward faster-growing niches to reduce dependence on one category in Michigan; the thesis is that price-led strategy without mix shift will cap recovery given category-specific headwinds.

Competitive Landscape

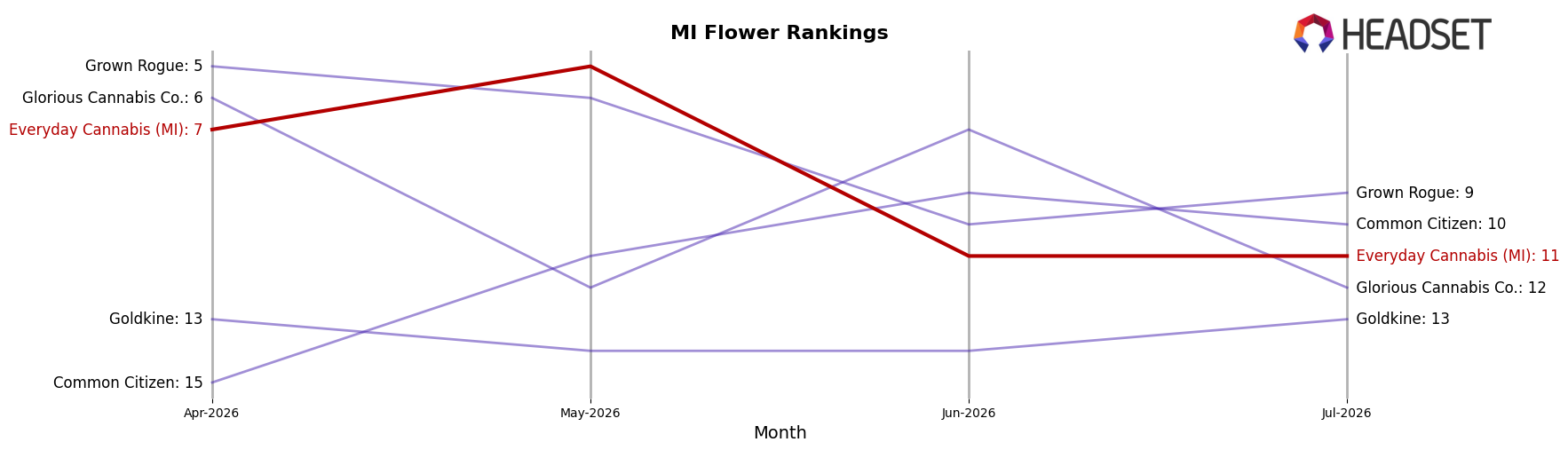

Everyday Cannabis (MI) sits at rank #11 in MI Flower in July 2026, down 5 spots from #6 in July 2025, and also down 4 positions versus #7 in April 2026; the brand’s earlier peak at #1 in November 2025 contrasts with a mid-2026 slide that puts it outside the top 10. Meanwhile, High Minded held #1 year over year despite a -12.46% sales change, and Mischief climbed from #10 to #4 with +59.39% YoY sales growth, indicating that competitors are converting momentum into rank gains while Everyday Cannabis (MI) yields share. The combination of a 5-place YoY drop and a 4-place decline over three months implies a trajectory of lost competitive position that will likely persist unless mix or distribution shifts reverse the trend.

Notable Products

Sour Banana Sherbert Pre-Roll (1g) posted the steepest shift in July 2026 with a -18.9% month-over-month drop while sliding to rank 4, whereas RS-11 Pre-Roll (1g) climbed 40.3% MoM to rank 2. Hashbar OG Pre-Roll (1g) in rank 1 added 6.9% MoM, and three of the top five are Pre-Roll SKUs, concentrating momentum at the value-entry point. The top-five Pre-Roll tilt alongside Neon Sunshine (28g) anchoring rank 10 with a single large-format Flower play implies the brand is polarizing demand between accessible Pre-Rolls and bulk Flower, setting up a price-tiered strategy over mix optimization.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.