Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Glorious Cannabis Co. is stocked at 509 licensed dispensaries across Michigan, Massachusetts, and Arizona, 410 of them in Michigan, with the deepest coverage in New Buffalo, Detroit, Grand Rapids, Ann Arbor, and Monroe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

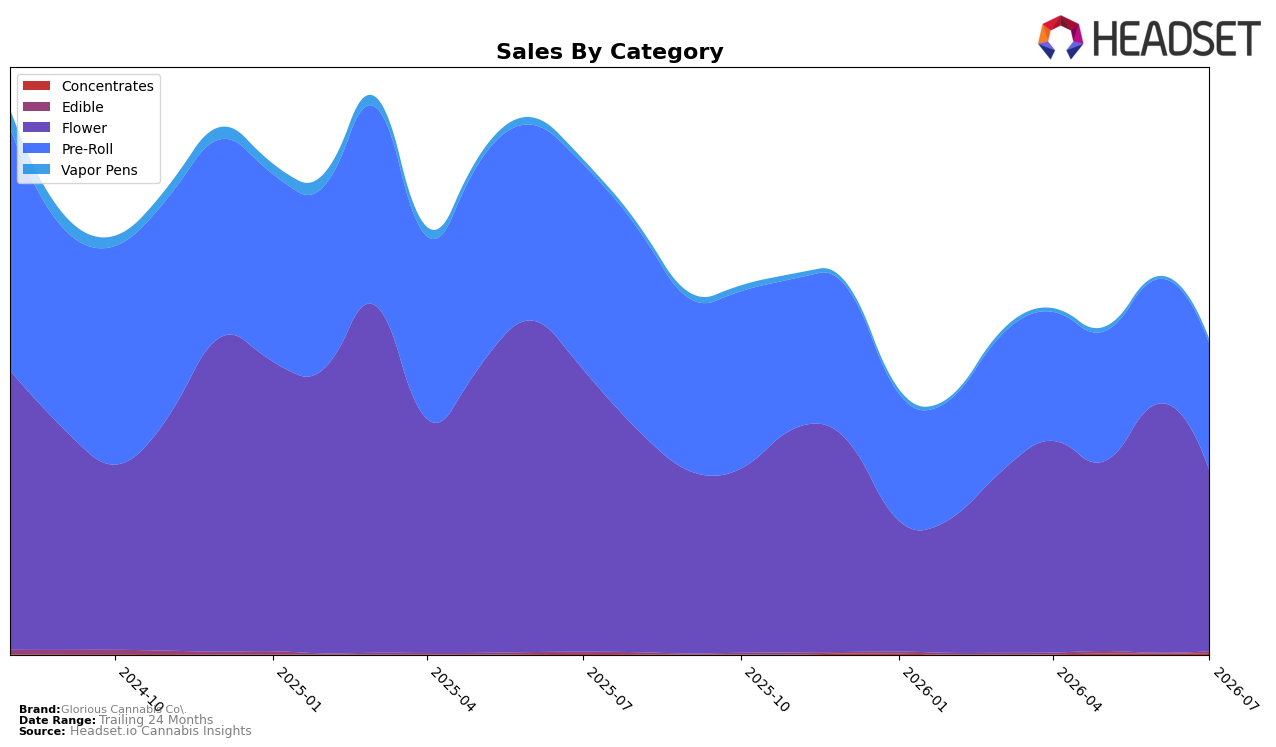

In July 2026, Glorious Cannabis Co. derived 57.42% of sales from Flower with a year-over-year decline of 36.08% and a month-over-month drop of 27.52%, while Pre-Roll held 40.23% share with a 38.40% YoY contraction but a 1.54% MoM uptick; Vapor Pens remained a small 1.34% share yet jumped 65.87% MoM despite a 6.07% YoY dip. Edible was just 0.54% share but surged 277.82% MoM alongside Concentrates at 0.46% share with 109.01% YoY growth and 34.97% MoM growth, and the brand’s average price rose 8.77% YoY as overall brand sales fell 36.47% YoY. The mix shows a heavy tilt to Flower and Pre-Roll that is compressing on a YoY basis, with nascent diversification in Vapor Pens, Edible, and Concentrates offering small but faster-moving pockets that can offset category-level drag.

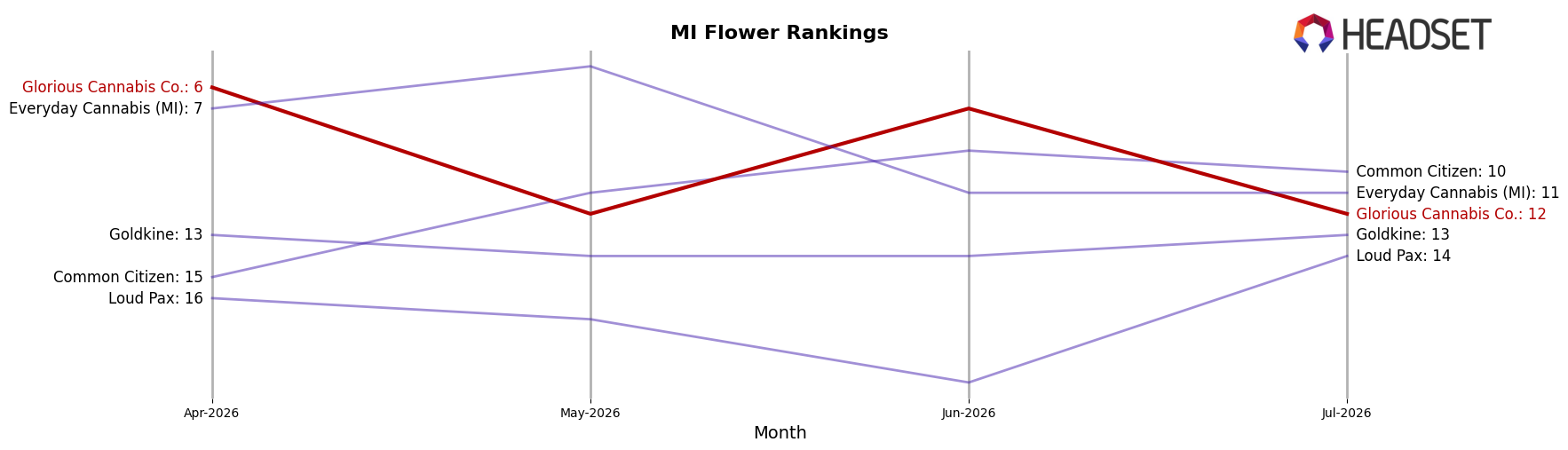

Given a rank of 12 in Flower in Michigan and a 57.42% reliance on Flower, the 27.52% MoM pullback there likely weighed disproportionately on July 2026 results, while the 1.54% MoM lift in Pre-Roll partially cushioned impact; however, the 8.77% YoY increase in average price alongside a 36.47% YoY sales decline indicates price/mix is not defending volume in core categories. The triple-digit momentum in Edible (277.82% MoM) and Concentrates (109.01% YoY) and the 65.87% MoM gain in Vapor Pens signal workable adjacency footholds, but at a combined 2.34% share these are too small to rebase performance unless expanded; the implication is that stabilizing Flower plus scaling the faster-growing adjacencies is required to improve positioning rather than relying on price increases to carry July 2026 performance.

Competitive Landscape

Glorious Cannabis Co. sits at rank #12 in Michigan Flower in July 2026, down four positions from #8 year over year, with a steeper three-month slide from #6 to #12 indicating a recent six-place drop; in contrast, High Minded held #1 year over year but did so while posting a 12.46% sales decline, and Mischief climbed from #10 to #4 alongside a 59.39% sales increase, while Glorious Cannabis Co.’s peak at #5 in March 2025 versus today’s #12 shows a seven-rank retreat that implies loss of velocity against faster risers. The directional pattern—falling four ranks YoY and six ranks in the last three months while peers like Goodlyfe Farms advanced from #5 to #3 with 36.83% growth—implies Glorious Cannabis Co. is ceding share to momentum brands and must counter short-term deterioration to avoid drifting out of the top 15.

Notable Products

Fire Styxx - Royal Punch Infused Pre-Roll (1g) posted the steepest decline in July 2026 at -19.8% while sliding to rank 3, contrasted by Fire Styxx - Shipwrecked Infused Pre-Roll (1g) up 33.5% at rank 6, implying a rotation within the lineup rather than category softness. Fire Styxx - Glitter Apples Infused Pre-Roll (1g) rose 40.8% to rank 1 while Fire Styxx - Tigers Breath Infused Pre-Roll (1g) fell 11.3% at rank 5, and eight of the top ten are Pre-Roll variants within the Fire Styxx family, concentrating demand in a single format. With Fire Styxx - Razzberry Diesel THCA Infused Pre-Roll (1g) up 28.6% at rank 8 and Unicorn Tears down 19.1% at rank 10, volatility is SKU-specific rather than category-wide. The pattern indicates Glorious Cannabis Co. is leaning into Fire Styxx Pre-Rolls as the commercial core, prioritizing flavor and THCA variants to cycle winners while pruning underperformers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.