Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

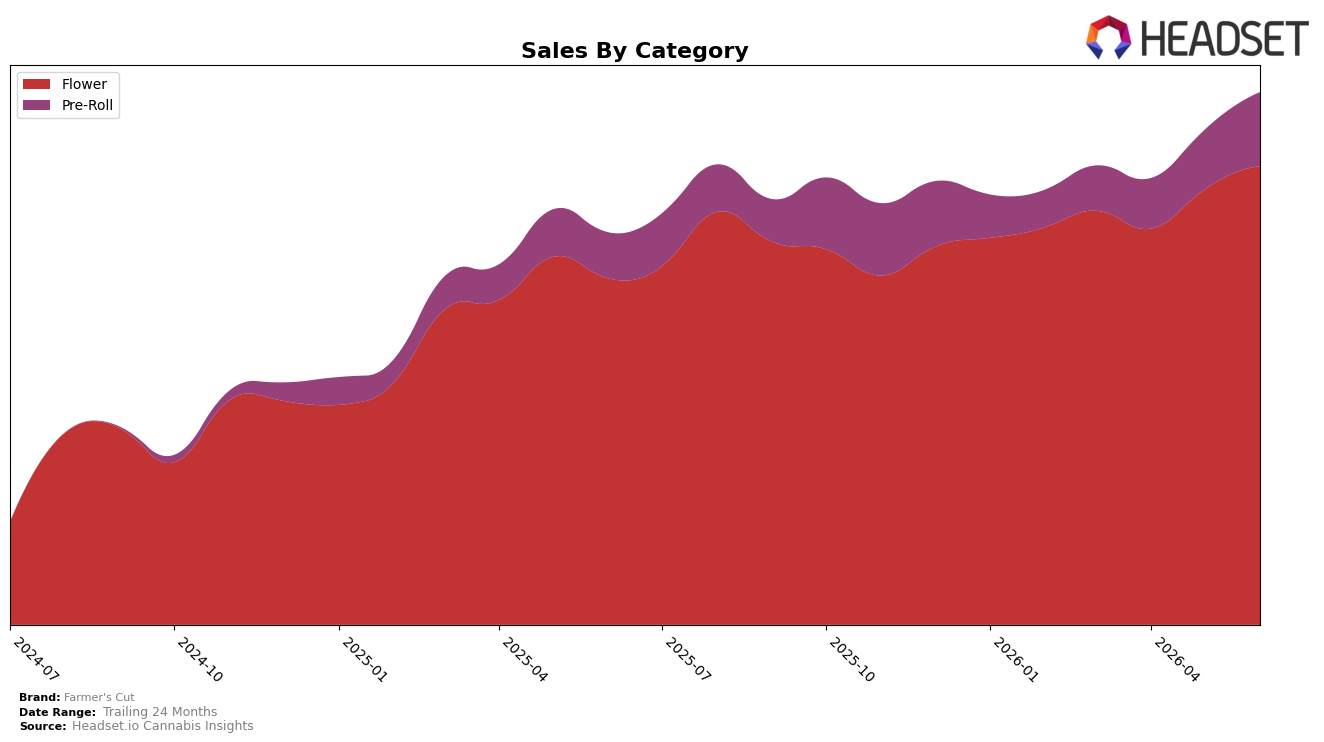

In June 2026, Farmer's Cut concentrated 86.16% of sales in Flower, with Pre-Roll at 13.84%, and Flower ranked 1 in Massachusetts while Pre-Roll rose faster month over month at 23.89% versus Flower’s 5.40%. Year over year, Pre-Roll expanded 61.35% compared to Flower’s 32.42%, while the brand’s average price fell 9.49% alongside a category-weighted tilt toward lower-price-per-unit Pre-Roll at $4.88 versus Flower at $30.32. The pattern implies deliberate mix broadening: maintaining a rank of 1 in Flower in Massachusetts while using rapid Pre-Roll growth to diversify revenue and cushion against price compression.

The mix shift — Pre-Roll adding 23.89% month over month and 61.35% year over year while Flower holds 86.16% share and 1st rank — suggests Farmer's Cut is trading some average price for volume reach, as evidenced by a 9.49% brand-wide price decline alongside 35.79% year-over-year sales growth. With Flower still contributing 86.16% of sales but growing slower than Pre-Roll by 28.93 percentage points year over year, the brand’s positioning favors scale in the core while seeding a second pillar that can lift total share without eroding the flagship rank in Flower.

Competitive Landscape

Farmer's Cut is ranked #1 in Massachusetts Flower in June 2026, improving 2 positions year over year from #3, and edging up 1 spot from #2 three months ago; that rise to a peak rank of #1 in June 2026 coincides with competitors moving in the opposite or slower directions, as Simply Herb slipped from #1 to #2 while posting a -1.6% year-over-year sales change and Perpetual Harvest held at #3 despite a 7.7% gain. Meanwhile, High Supply / Supply rose from #5 to #4 on 16.7% year-over-year growth and Root & Bloom jumped from #16 to #5 on 158.9% growth, yet neither converted those gains into a higher rank than #4 or #5, indicating Farmer's Cut’s ascent to #1 is driven less by absolute growth and more by outperforming rivals in rank momentum across the last three and twelve months.

Notable Products

Gas O Lina Pre-Roll (1g) posted the standout move in June 2026 with +99.2% month over month to rank #2, while Glazed Apricot Lime Pre-Roll (1g) fell 39.6% to rank #7, creating a sharp divergence within the same format. Northern Lime Lights Pre-Roll (1g) held #1 with +16.1% MoM, and four of the top ten are Pre-Roll SKUs, indicating assortment depth concentrated in a single category. Gas O Lina (3.5g) surged +91.9% MoM to rank #5 and was the only Flower SKU in the top ten, generating $111,476 as a single-format outlier. The pattern implies Farmer's Cut is leaning into Pre-Roll-led velocity while testing a cross-format ladder on Gas O Lina to build a brand line that can travel beyond Pre-Roll.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.