Market Insights Snapshot

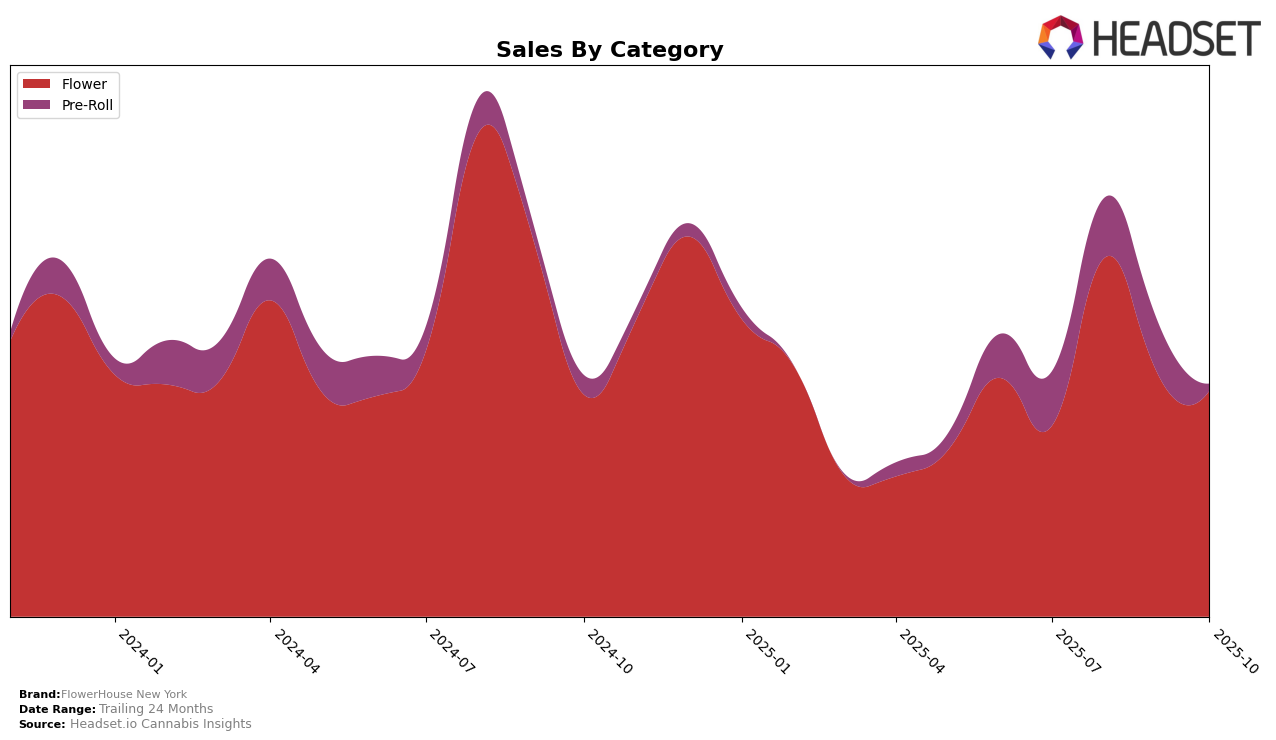

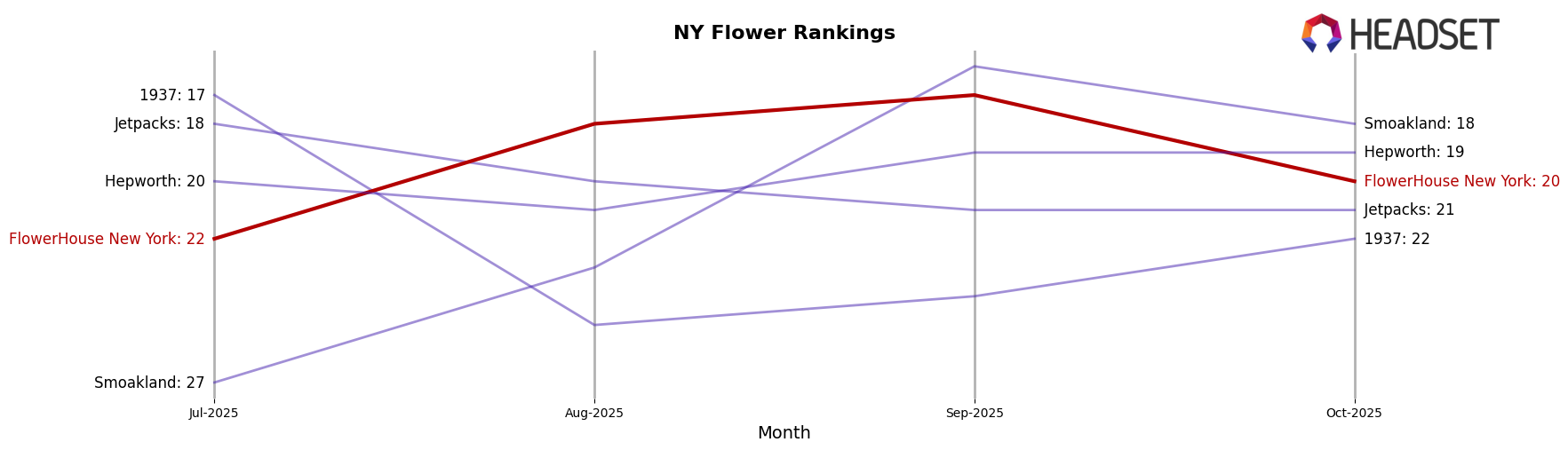

FlowerHouse New York has shown varied performance across different categories and states over the past few months. In the New York market, the brand's flower category has maintained a presence in the top 30, though it experienced some fluctuations. Starting from a rank of 22 in July, it improved to 18 in August, continued to 17 in September, but then fell back to 20 in October. This movement suggests a competitive landscape where FlowerHouse New York is managing to hold its ground but faces challenges in maintaining a consistent upward trajectory. Despite these fluctuations, the brand has demonstrated resilience, with sales figures indicating a notable peak in August.

In contrast, FlowerHouse New York's performance in the pre-roll category in New York has been more challenging. The brand did not break into the top 30 in July and August, and while it managed to reach rank 32 in September, it fell back significantly to 51 in October. This drop highlights the competitive nature of the pre-roll market and the difficulties FlowerHouse New York faces in gaining a foothold. The decrease in sales from September to October further underscores the need for strategic adjustments to improve their position in this category. These insights suggest that while FlowerHouse New York is a recognized player in the flower segment, it may need to innovate or adjust its strategy to improve its standing in the pre-roll market.

Competitive Landscape

In the competitive landscape of the New York flower category, FlowerHouse New York has experienced fluctuating rankings over the past few months, indicating a dynamic market presence. Starting at rank 22 in July 2025, FlowerHouse New York climbed to 18th in August, further improved to 17th in September, but then dropped back to 20th in October. This volatility suggests a competitive environment where brands like Smoakland and Jetpacks are also vying for market share. Notably, Smoakland showed a consistent upward trend, reaching 16th place in September before slightly dropping to 18th in October, while Jetpacks maintained a steady presence around the 20th rank. Meanwhile, 1937 experienced a decline in rank over the same period, which could indicate opportunities for FlowerHouse New York to capitalize on shifting consumer preferences. Despite these challenges, FlowerHouse New York's sales figures reveal a robust performance, particularly in August, suggesting strong brand loyalty and potential for growth in the competitive New York flower market.

Notable Products

In October 2025, the top-performing product for FlowerHouse New York was Indica Pre-Roll (1g) in the Pre-Roll category, which climbed to the number one spot with sales of 5235 units. Sativa Pre-Roll (1g), previously holding the top rank from July to September, dropped to second place. Astro Candy (3.5g) in the Flower category made its debut at third place, indicating a strong market entry. Slapaya Infused Pre-Roll 2-Pack (1g) moved from third in September to fourth in October, while Melon Infused Pre-Roll 2-Pack (1g) entered the rankings at fifth place. Notably, the shift in rankings suggests a dynamic market with changing consumer preferences for FlowerHouse New York's product offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.