Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

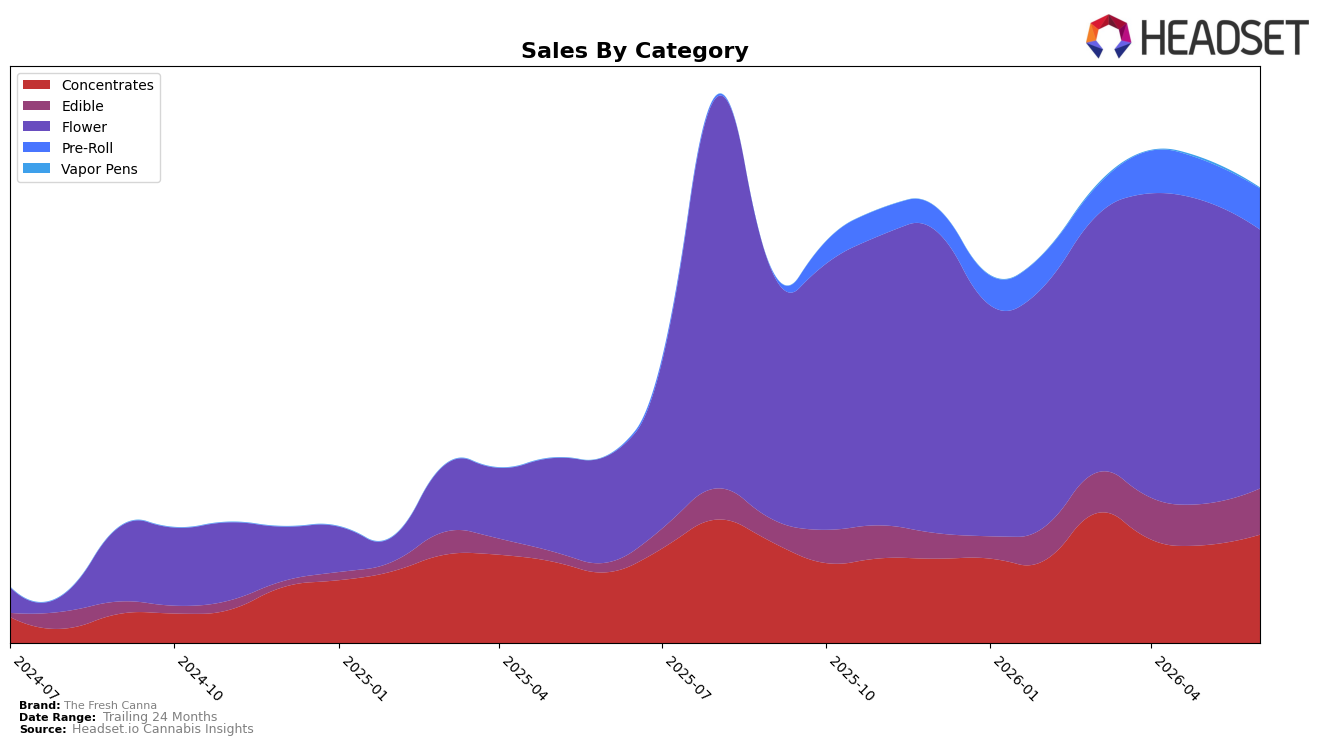

In June 2026, The Fresh Canna’s mix skews toward Flower at 56.96% share with year-over-year growth of 142.71% but a month-over-month decline of 14.44%, while Concentrates holds 23.81% share with 53.08% YoY growth and a 10.75% MoM increase. Edible has expanded to 10.10% share with 383.43% YoY growth and 11.63% MoM growth, and Pre-Roll sits at 9.00% share with a 1.70% MoM uptick alongside missing YoY data. Vapor Pens is minimal at 0.13% share with a 62.09% MoM drop and no YoY read. With Flower ranked 17th in Michigan and average brand price up 11.13% YoY to $14.53, the pattern implies reliance on Flower volume is moderating as incremental growth shifts to Edible and Concentrates despite Flower’s scale.

The combined MoM expansion in Concentrates (+10.75%) and Edible (+11.63%) against Flower’s MoM contraction (-14.44%) implies a deliberate tilt toward higher-momentum, non-Flower formats that can diversify revenue and reduce exposure to a single category, while maintaining Flower’s visibility at rank 17 in Michigan. Given Edible’s 383.43% YoY surge from a 10.10% share base and Concentrates’ 53.08% YoY lift at 23.81% share, the mix suggests headroom to trade up basket frequency without overextending price, as the brand’s 11.13% YoY average price increase to $14.53 coincides with category-level growth rather than a price-led pullback.

Competitive Landscape

The Fresh Canna sits at rank #17 in June 2026, improving 40 positions from #57 year over year, while slipping 1 spot from #18 in March 2026 and sitting 4 places below its peak of #13 in August 2025; meanwhile, High Minded held #1 both year over year and in June 2026 despite a -13.7% YoY sales change, and Goodlyfe Farms advanced from #5 to #2 with +44.1% YoY sales growth, indicating that The Fresh Canna’s 40-rank YoY climb puts it back in the competitive mid-tier but the 1-place quarter-over-quarter dip and 4-place gap from its August 2025 peak imply momentum that is stabilizing rather than accelerating.

Notable Products

Blue Raspberry Live Rosin Gummies 5-Pack (200mg) posted the steepest decline at -26.8% month over month while slipping to rank 6, and Watermelon Runtz Live Resin Gummies 5-Pack (200mg) also contracted by -11.2% at rank 7. Offsetting that, Red Raspberry Live Resin Gummies 5-Pack (200mg) climbed 34.7% MoM to rank 1 and Strawberry Lemonade Live Rosin Gummies 5-Pack (200mg) rose 21.7% to rank 3, concentrating momentum at the very top. With eight of the top ten in Edibles and only one Concentrates SKU at rank 10, June 2026 points to an edibles-led lineup that is consolidating around a few fast-moving fruit SKUs while mid-pack flavors lose share, implying portfolio pruning toward winners and less support for slower variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.