Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sapphire Farms is stocked at 235 licensed dispensaries across Michigan and New York, 143 of them in Michigan, with the deepest coverage in Detroit, New Buffalo, Monroe, Ypsilanti, and Ann Arbor. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

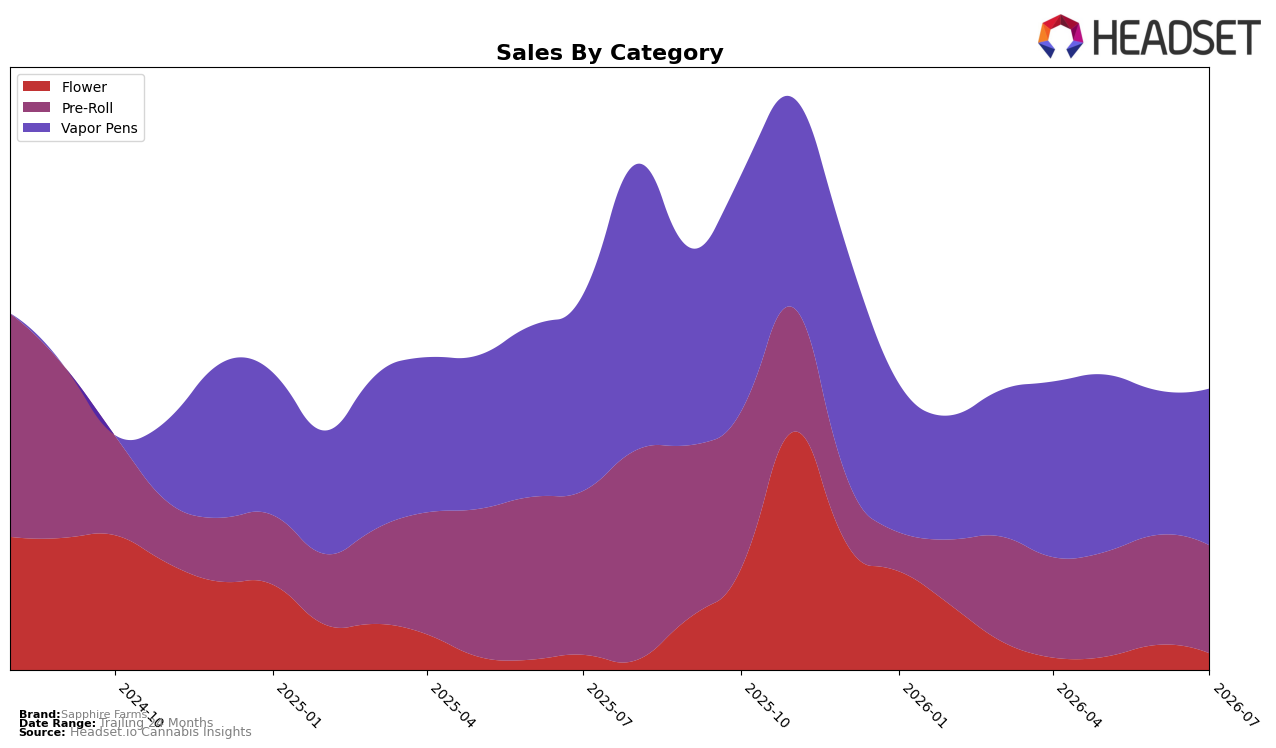

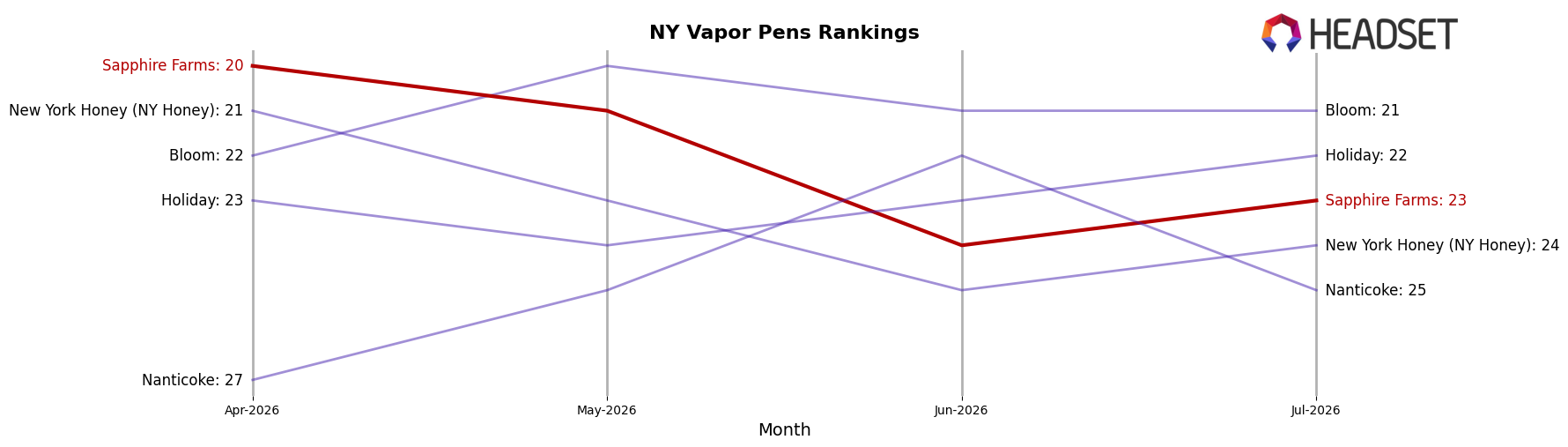

In July 2026, Sapphire Farms leaned further into Vapor Pens at 55.76% share while Pre-Roll held 38.36% and Flower 5.88%; within that mix, Vapor Pens grew 8.55% month over month despite a -20.28% year-over-year decline, whereas Pre-Roll slipped -1.84% MoM on a steeper -34.19% YoY and Flower fell -33.82% MoM even as it rose 10.15% YoY. The overall brand saw sales down -25.13% YoY alongside an 8.44% YoY increase in average price, and the brand’s Vapor Pens ranked 23rd in New York, implying a portfolio anchored by a category with improving recent velocity but lingering annual drag compared to last year.

The widening Vapor Pens mix (+8.55% MoM vs. Pre-Roll’s -1.84% MoM) paired with a higher average price (+8.44% YoY) signals a price-led, higher-ticket tilt that may be trading customers up within a shrinking annual base (-25.13% YoY), while the sharp Flower pullback (-33.82% MoM despite +10.15% YoY) suggests promotional or inventory timing rather than a durable volume engine. With Vapor Pens at 55.76% share and ranked 23rd in New York, the immediate positioning priority is to convert the recent category momentum into sustained share capture, as the current mix favors a single category that is rebounding sequentially but still underperforms year over year.

Competitive Landscape

Sapphire Farms sits at rank #23 in NY Vapor Pens for July 2026, down 4 positions year over year from #19, and 3 positions below its April 2026 mark of #20, while still trailing its peak of #11 from August 2025; in contrast, Fernway climbed from #3 to #1 with a 46.8% year-over-year sales increase, and Jetty Extracts surged from #22 to #4 alongside a 199.3% year-over-year lift, indicating that Sapphire Farms’ relative decline in rank alongside competitors’ upward mobility points to share being reallocated toward faster-rising leaders.

Notable Products

Fire OG Pre-Roll (1g) posted the standout movement in July 2026 with a +50.2% MoM surge, rising into rank 5, while Cookies N Kush Pre-Roll (1g) fell -22.4% MoM at rank 2. Black Cherry Trop Pre-Roll (1g) led the lineup at rank 1 with +41.5% MoM and $31,801 in sales, contrasting with Purple Palm Tree Delight Pre-Roll (1g) sliding -15.0% MoM at rank 6. With all top-10 SKUs in the Pre-Roll category, the concentration implies Sapphire Farms is leaning into a focused pre-roll portfolio where momentum skews toward a few flavor-led SKUs rather than broad-based lift.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.