Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Friendly Brand (formerly Friendly Farms) is stocked at 212 licensed dispensaries across California, with the deepest coverage in Los Angeles, Sacramento, San Diego, Santa Ana, and La Mesa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

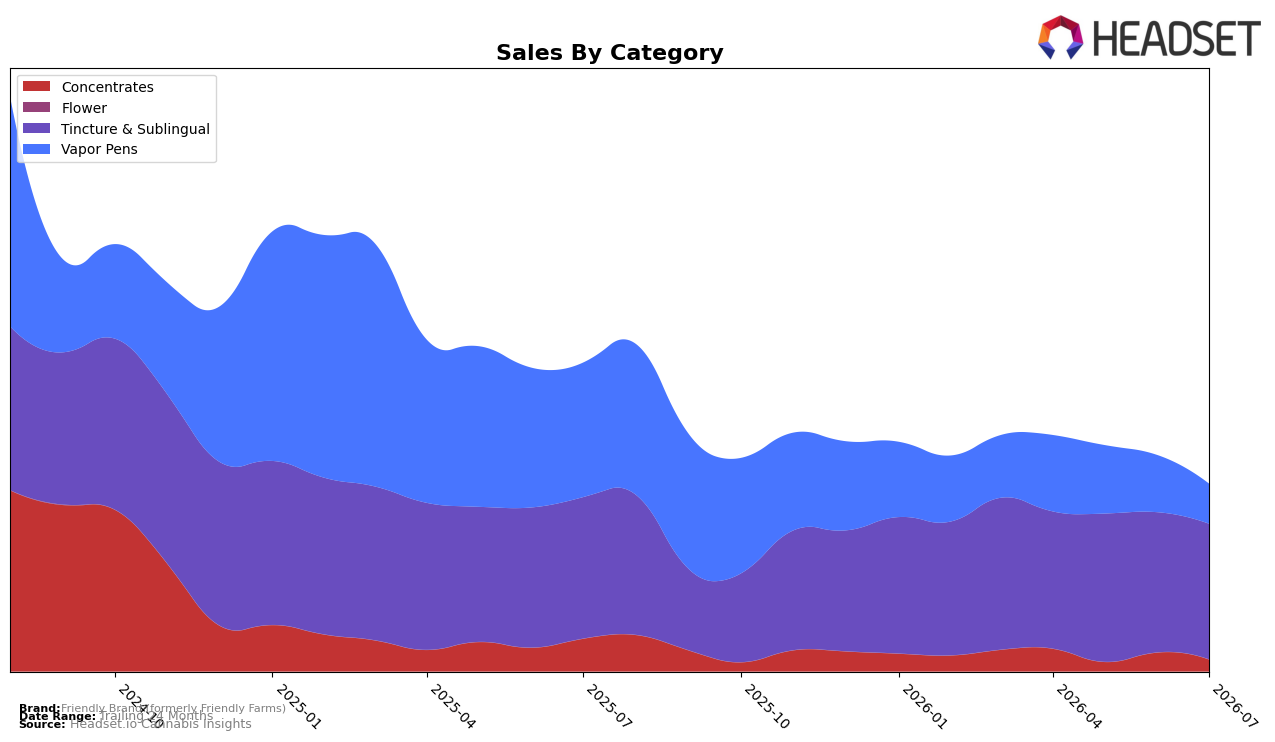

Friendly Brand (formerly Friendly Farms) concentrated 72.37% of July 2026 sales in Tincture & Sublingual, where year-over-year declined 4.15% and month-over-month fell 3.24%, while Vapor Pens at 21.34% share contracted 70.28% YoY and 29.84% MoM. Concentrates held 6.29% share with 63.82% YoY and 37.34% MoM declines, and the overall brand sales were down 39.28% YoY alongside an 8.02% YoY average price decrease to $27.77. In California Tincture & Sublingual, the brand sits at rank 6, and with the top category’s smaller YoY drop than the 70.28% YoY fall in Vapor Pens, the mix is pivoting toward a comparatively steadier tincture core even as MoM erosion persists.

The heavier 21.34% mix weight in Vapor Pens combined with a 29.84% MoM contraction versus a 3.24% MoM dip in Tincture & Sublingual implies near-term exposure to volatility that is outpacing the core category’s decline, while the 6.29% Concentrates share and 37.34% MoM drop amplify downside without offsetting scale. Holding rank 6 in California Tincture & Sublingual alongside a 4.15% YoY decline versus the brand’s 39.28% YoY sales drop suggests positioning that leans on tinctures as the defensible anchor, implying that stabilizing or rebuilding share will likely come from deepening presence in Tincture & Sublingual while deprioritizing faster-falling adjuncts.

Competitive Landscape

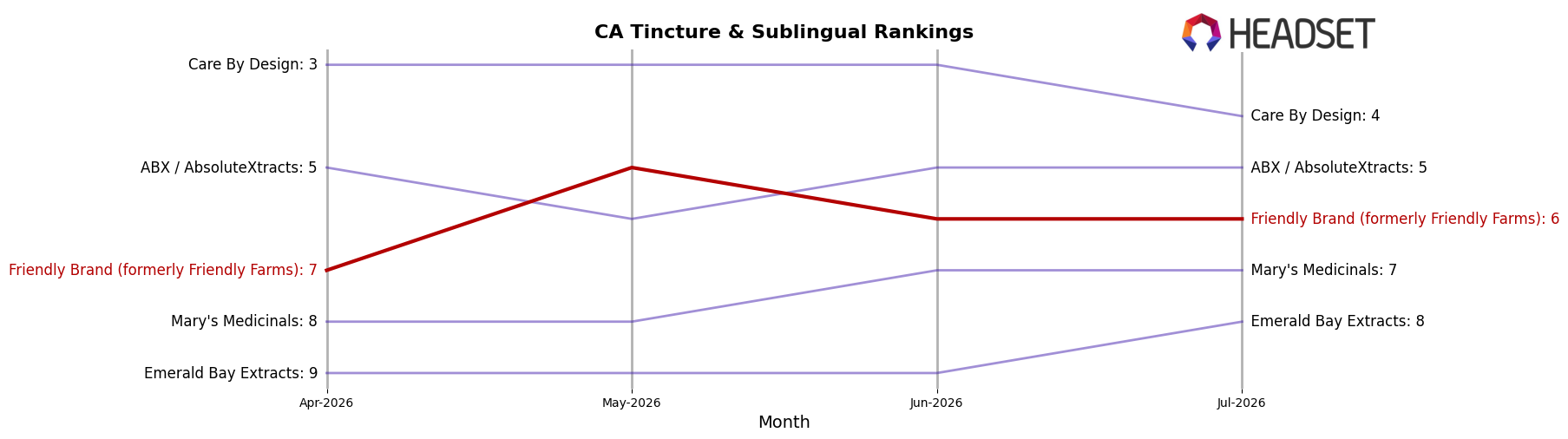

Friendly Brand (formerly Friendly Farms) is ranked #6 in California Tincture & Sublingual for July 2026, unchanged from #6 year over year, while improving one spot from #7 in April 2026 and coming off a peak of #5 in May 2026; in contrast, Yummi Karma advanced from #2 to #1 with a 15.99% year-over-year sales increase and ABX / AbsoluteXtracts climbed from #7 to #5 with 30.19% growth, whereas Papa & Barkley slid from #1 to #2 alongside a 13.54% decline. The combination of a flat year-over-year rank at #6 and a recent dip from a #5 peak implies Friendly Brand is holding share but risks ceding ground to faster risers unless it converts short-term fluctuations into sustained rank gains.

Notable Products

Bubba Kush Full Spectrum Tincture (1000mg THC, 30ml) delivered the headline move in July 2026 with a +150.4% month-over-month surge into rank 2, while Blue Hawaiian Full Spectrum Tincture (1000mg THC, 30ml, 1oz) slipped -9.1% to rank 5. The top spot held steady as Blue Dream Full Spectrum Tincture (1000mg THC, 30ml) rose +6.4% and maintained rank 1, and two SKUs without prior baselines entered at ranks 4 and 8. With all top-10 items concentrated in Tincture & Sublingual and one SKU falling -48.4% at rank 9, the pattern implies Friendly Brand (formerly Friendly Farms) is consolidating around a few high-velocity tinctures rather than broadening into adjacent formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.