Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

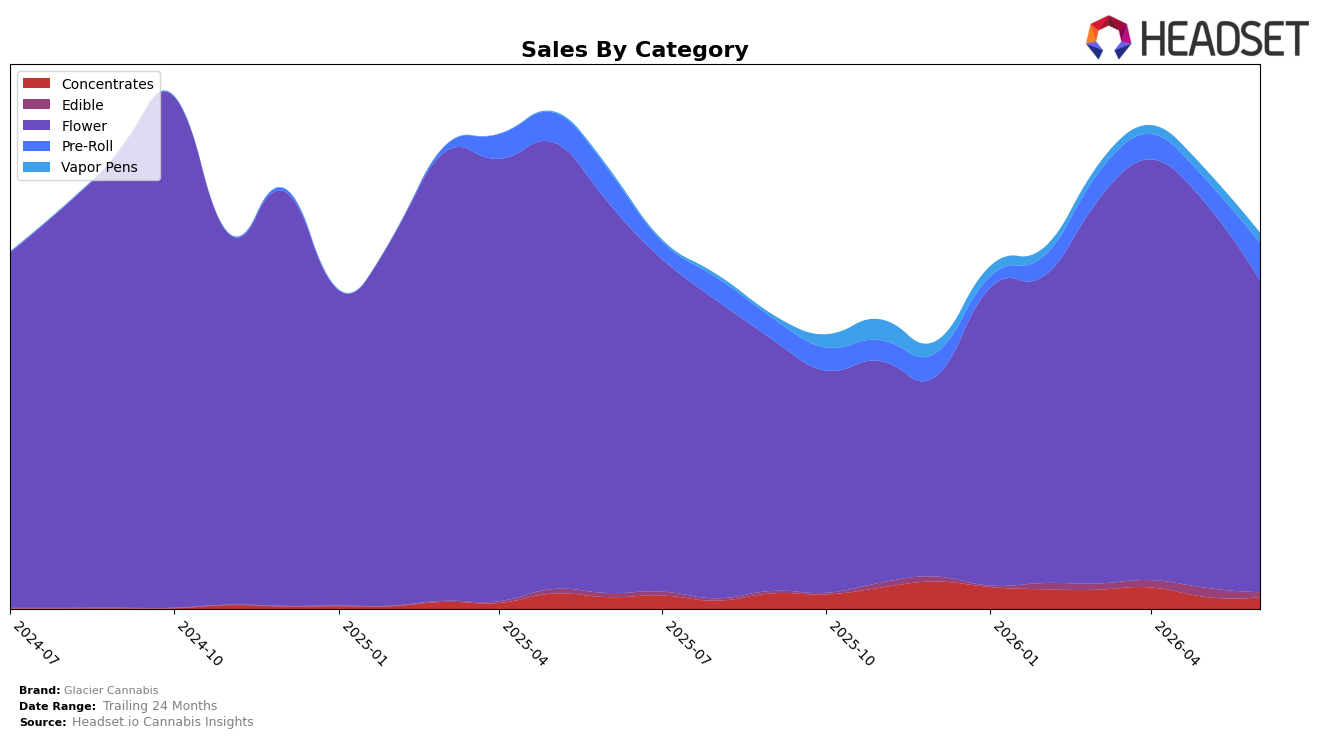

In June 2026, Glacier Cannabis concentrated 83.23% of sales in Flower, where year-over-year sales fell 20.17% and month-over-month declined 19.14%, while the brand’s overall sales were down 14.84% YoY and average price edged up 2.10%. Counterbalancing that contraction, Pre-Roll expanded to 9.97% share with 15.25% YoY growth and a 59.25% MoM surge, and Vapor Pens, though only 2.56% share, posted 419.71% YoY growth and a 1.58% MoM gain; meanwhile, Edible slipped 48.93% MoM despite 22.50% YoY growth, and Concentrates were flat YoY at 0.13% with a 2.31% MoM dip. The mix implies a pivot from a Flower-heavy profile toward inhalables variety, as rapid Pre-Roll and Vapor Pen gains are beginning to offset double-digit Flower declines.

Positioning-wise, a 23 rank in Flower in Michigan alongside a 20.17% YoY Flower decline and 19.14% MoM drop suggests diminishing leverage in the lead category, while a 59.25% MoM Pre-Roll lift and 419.71% YoY Vapor Pen growth indicate traction in impulse and convenience formats. With overall prices up 2.10% while Flower average price sits at 17.17 and Vapor Pens at 17.35, the brand is aligning closer to value-accessible inhalables, and the 48.93% MoM Edible contraction signals limited pull outside smokeable and vape segments. The pattern implies Glacier Cannabis can stabilize share by reallocating focus from Flower dominance toward faster-growing inhalable subcategories where momentum is measurable month to month.

Competitive Landscape

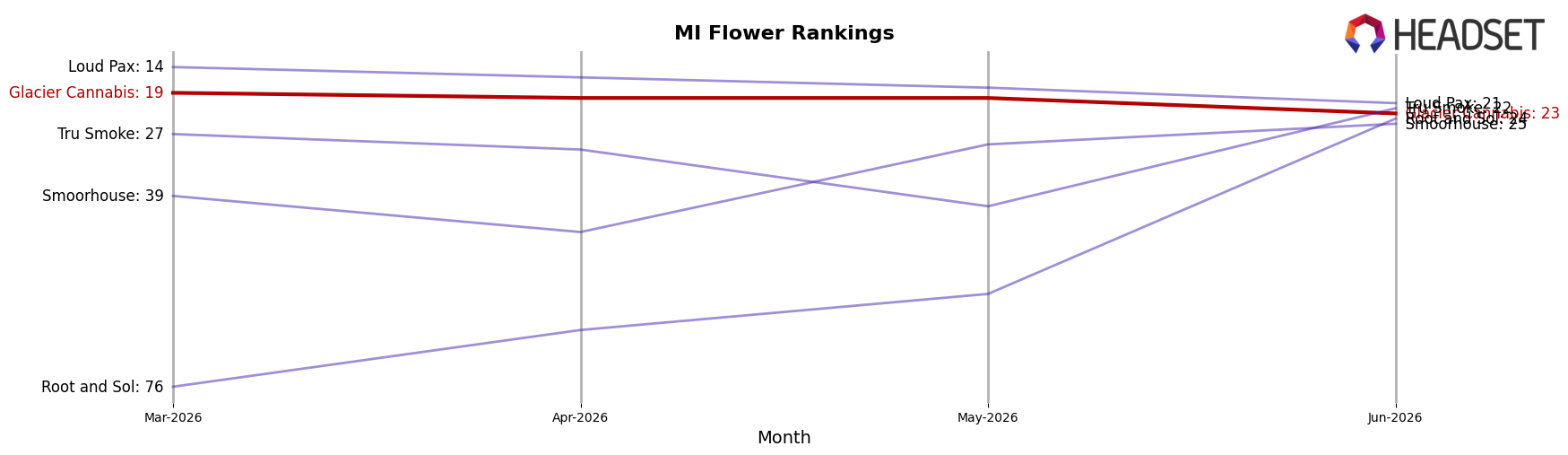

Glacier Cannabis sits at rank #23 in MI Flower in June 2026, down 4 positions year over year from #19, and 4 spots lower than its March 2026 placement at #19; this stands in contrast to Goodlyfe Farms rising from #5 to #2 and Mischief jumping from #13 to #5, while category leader High Minded held #1 with a -13.7% YoY sales change versus Mischief’s +146.1% surge. Compared with its historical peak of #10 in October 2024, the current #23 position marks a 13-rank slide, and the year-over-year decline from #19 to #23 coincides with rivals consolidating top-5 share, as Society C edged from #2 to #3 and Play Cannabis moved from #3 to #4. The pattern implies Glacier Cannabis has transitioned from a prior top-10 contender to a mid-20s player as faster-moving competitors expand, suggesting share defense rather than rank recovery is the near-term trajectory.

Notable Products

Maui Wowie Pre-Roll (1g) posted the steepest decline in June 2026 at -17.6% MoM while sliding to rank 3, indicating a pullback in Pre-Roll traction compared with Flower SKUs ascending to the top slots. Green Crack (1g) also fell -12.3% MoM and sits at rank 2, contrasting with Blast Chiller (Bulk) at rank 1 and Super Boof (Bulk) tied at rank 2, which signals that bulk Flower is consolidating the lead as single-gram and Pre-Roll formats lose share. Four of the top ten are bulk Flower entries clustered within ranks 1–8, and Apple Tartz (Bulk) holds rank 4 despite a $71,919 tally, implying that higher-volume pack sizes are driving placement even when absolute revenue varies. The pattern implies Glacier Cannabis is tilting toward bulk Flower dominance, prioritizing volume-oriented formats over smaller units and Pre-Rolls for near-term commercial gains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.