Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Goldkine is stocked at 241 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Detroit, Inkster, Kalamazoo, and Monroe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

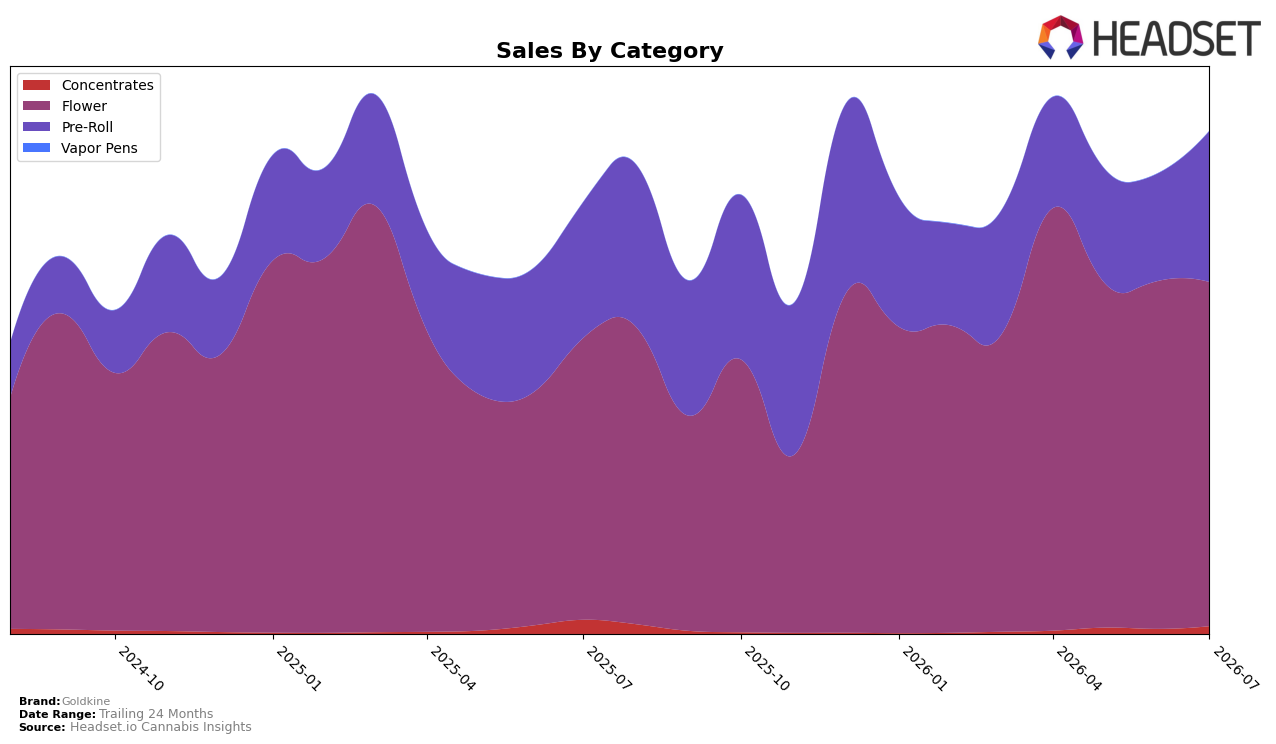

Goldkine concentrated 68.50% share in Flower with 22.21% year-over-year growth but a -1.08% month-over-month dip, while Pre-Roll reached 30.03% share with 11.19% year-over-year growth and a 40.50% month-over-month surge; Concentrates remained 1.47% share with -46.41% year-over-year contraction despite a 57.44% month-over-month rebound. Average price rose 10.37% year-over-year to $18.08, and in Michigan the brand’s Flower rank sits at 13, indicating depth in the core while near-term momentum comes from Pre-Roll’s step-up; the pattern implies reliance on Flower for scale but tactical volume is shifting to Pre-Roll to offset the monthly softness in Flower.

With Flower still the anchor at 68.50% share and rank 13 in Michigan, the -1.08% month-over-month in that category alongside a 40.50% month-over-month lift in Pre-Roll signals a rebalancing toward lower-priced, faster-turn formats as price rose 10.37% year-over-year. The 57.44% month-over-month lift in Concentrates against a -46.41% year-over-year drop suggests opportunistic inventory or promo-driven recovery rather than a durable base, so positioning hinges on maintaining Flower’s 22.21% year-over-year trajectory while letting Pre-Roll’s 30.03% share capture incremental baskets; this mix implies defending core rank via Flower consistency while using Pre-Roll spikes to smooth month-to-month volatility.

Competitive Landscape

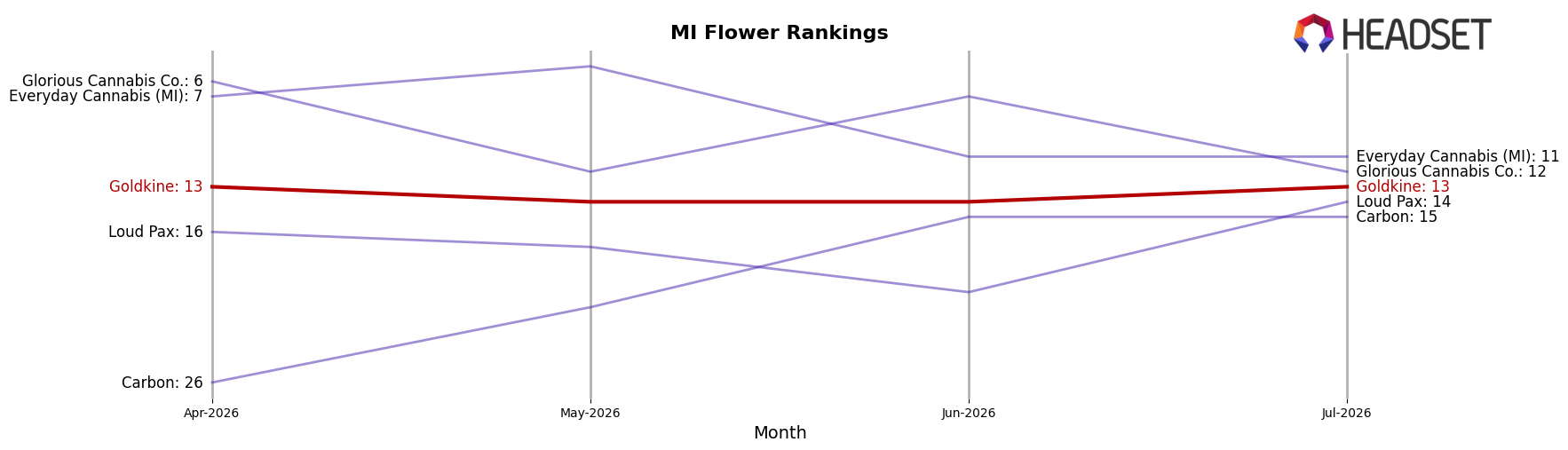

Goldkine sits at rank #13 in MI Flower for July 2026, improving 7 places from #20 year over year, while holding flat versus three months ago at #13; the brand’s peak position of #12 in February 2025 indicates it is hovering just outside the top 10. In contrast, High Minded stayed at #1 year over year despite a 12.5% YoY sales decline, and Mischief advanced from #10 to #4 with a 59.4% YoY sales increase, signaling that upward mobility is still achievable for faster-growing peers. The pattern implies Goldkine’s rank trajectory is stabilizing near the threshold of the top tier, but without a step-change in velocity it risks being bypassed by faster risers climbing multiple ranks per year.

Notable Products

Pure Michigan Infused Pre-Roll (1g) posted the largest month-over-month surge at 63.4% and climbed into rank 3, while Blueberry Crumble Infused Pre-Roll (1g) fell 14.4% yet held rank 1. Cherry Punch Infused Pre-Roll (1g) gained 10.1% at rank 2, creating a top-three stack where two SKUs expanded while the leader contracted, which implies mix rebalancing toward faster-moving line extensions in July 2026. Eight of the top ten are Pre-Roll SKUs, with only one Flower entry at rank 8, and the 5‑Pack format sits at rank 10 with $34,017, signaling deeper commitment to pre-roll dominance and multi-format coverage rather than broad strain diversification.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.