Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Green State derived 98.95% of sales from Concentrates with a 41.78% year-over-year increase but a 27.49% month-over-month decline, while Pre-Roll held 1.05% share with 160.59% year-over-year growth and a 47.05% month-over-month drop. The brand’s average price fell 3.89% year over year to $14.57, and Concentrates pricing sat at $14.79 alongside a category rank of 30 in Washington. The combination of high Concentrates dependence and concurrent month-over-month pullbacks in both categories implies volume volatility concentrated in a single segment, suggesting June’s contraction was driven more by mix and seasonality than by broad pricing pressure.

With Concentrates at 98.95% share and Pre-Roll at 1.05%, the 27.49% month-over-month decline in the core category versus a steeper 47.05% month-over-month contraction in the nascent Pre-Roll indicates limited diversification is amplifying swings in overall performance. Given a 41.60% brand-level year-over-year sales increase alongside a 30th-place Concentrates rank in Washington, the mix points to a mid-pack positioning reliant on depth within a single category rather than breadth across formats, implying that modest expansion of Pre-Roll share could buffer monthly volatility without undermining the Concentrates-led identity.

Competitive Landscape

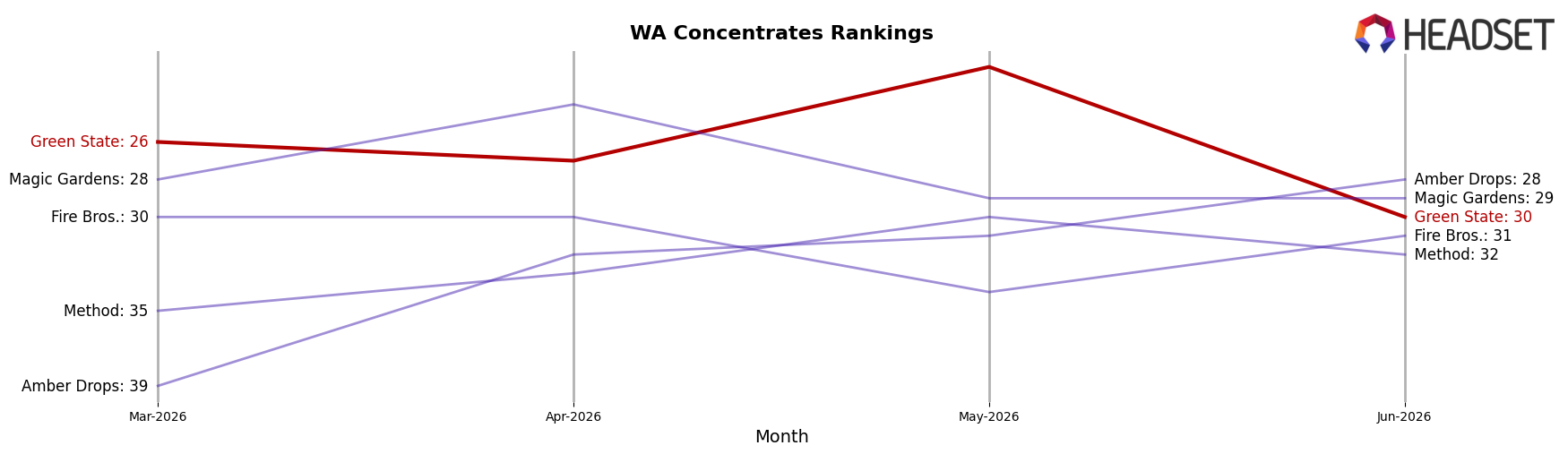

Green State sits at rank 30 in Washington Concentrates in June 2026, improving 14 positions from rank 44 year over year while slipping 4 spots from rank 26 in March 2026; the brand’s peak was rank 21 in August 2024, placing the current position 9 ranks below that high. In the same June 2026 snapshot, Ooowee held rank 1 with a year-over-year sales decline of 6.8% while staying flat at rank 1, and Constellation Cannabis advanced from rank 7 to rank 3 on 44.1% sales growth, indicating that upward mobility is occurring near the top even as the leader contracts; this contrast implies Green State’s rank trajectory—up year over year but down versus three months ago—signals mid-tier volatility where gains are attainable but require momentum against faster-rising rivals.

Notable Products

Redneck Wedding Hash Rosin (1g) led the movement in June 2026 with a month-over-month decline of 47.4% and a rank at 2, while Jabba OG Hash Rosin (1g) fell 37.0% at rank 3; in contrast, Ice Cream Cake Rosin (1g) rose 45.2% to rank 1 with $8,610 in sales. Five of the top six SKUs posted double-digit declines between 14.6% and 47.4%, and four of the top ten dropped more than 16.4%, indicating that gains are concentrated in a narrow winner rather than broad-based. With eight of the top ten positioned in Concentrates and multiple Ice Cream Cake variants appearing together in the top seven, the lineup is clustered in one form factor and flavor family. The pattern implies Green State is leaning into a hero-SKU strategy within Concentrates, trading breadth for deeper push behind a single fast-rising strain line.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.