Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Harney Brothers Cannabis is stocked at 191 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Newburgh, Albany, and Brooklyn. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

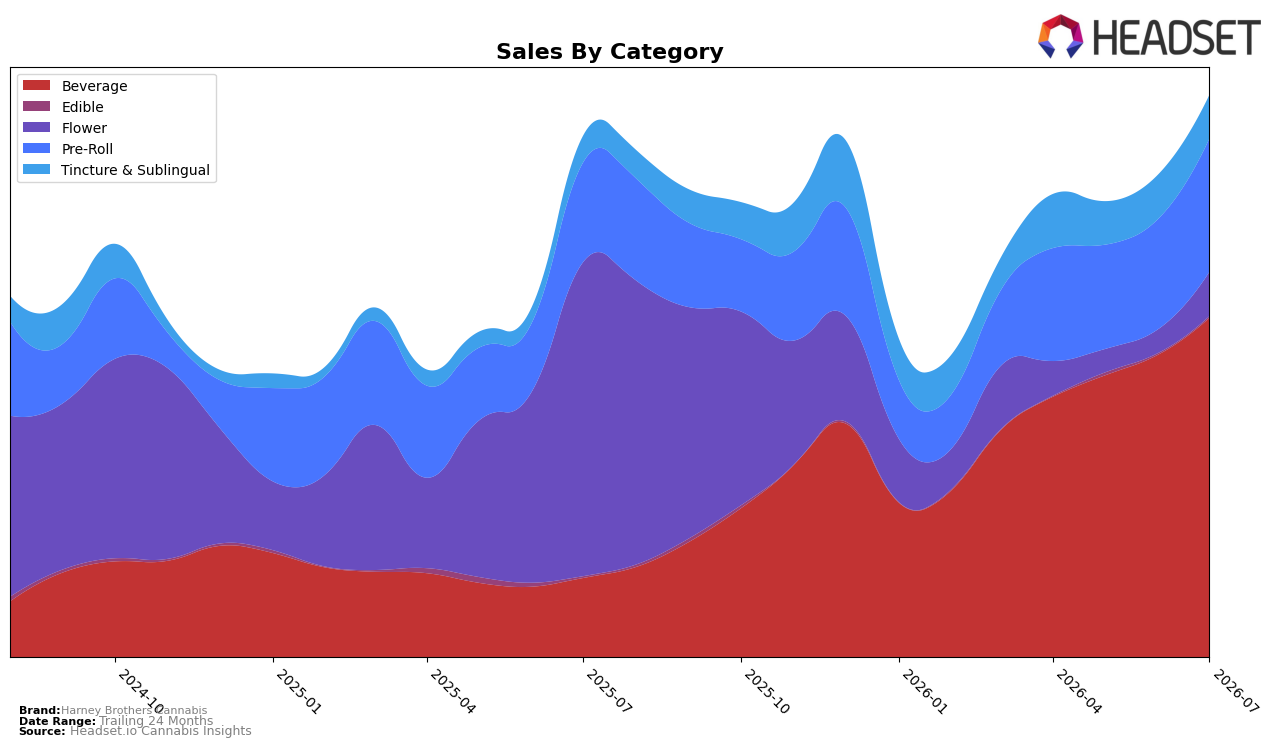

Harney Brothers Cannabis concentrated 60.15% of July 2026 sales in Beverage with 327.37% year-over-year growth and 12.20% month-over-month growth, while Pre-Roll held 23.69% share with 33.56% YoY and 20.85% MoM. Flower shrank to 7.93% share after an -85.77% YoY decline but bounced 84.28% MoM, and Tincture & Sublingual at 7.83% grew 61.60% YoY despite a -1.65% MoM slip. Edible remained peripheral at 0.40% share with -3.43% YoY and 5.18% MoM. With Beverage ranked 3 in New York and the brand’s average price down 62.42% YoY to $7.85, the pattern points to a deliberate pivot toward volume-led Beverage gains while compressing price to widen reach.

The expanding Beverage mix alongside accelerating Pre-Roll MoM growth implies a two-tier demand capture: high-frequency drinkers fueling baseline share and Pre-Roll supplying incremental trips, which can sustain the 7.78% brand sales YoY lift even as Tincture & Sublingual softens MoM. The extreme YoY contraction in Flower paired with a sharp 84.28% MoM rebound suggests selective SKU or distribution re-entry rather than a full-category comeback, indicating portfolio focus where velocity is proven. Holding rank 3 in New York Beverage while pricing down materially implies the brand is trading elasticity for share, positioning itself as a value-access gateway in ready-to-drink formats and using Pre-Roll momentum to stabilize basket size.

Competitive Landscape

Harney Brothers Cannabis is ranked #3 in NY Beverage in July 2026, improving 4 positions year over year from #7, while holding steady at #3 over the last three months; that rise contrasts with Ayrloom maintaining #1 despite a -5.4% sales change year over year and Layup holding #2 alongside a 155.5% year-over-year sales increase. Against the next tier, High Peaks sits at #4 with +40.8% sales growth year over year, while Tune slid from #3 to #5 with a -26.6% decline, indicating Harney Brothers Cannabis’s rank ascent comes amid mixed competitor momentum and implies the brand’s trajectory is consolidating a top-three position rather than chasing the top spot in the immediate term.

Notable Products

CBD/THC 1:1 Peach Black Tea (10mg CBD, 10mg THC, 16oz) posted a -9.8% month-over-month change to rank 3 in July 2026, while CBD/THC 1:1 Hibiscus Herbal Tea (10mg CBD, 10mg THC, 16oz) rose +14.9% to hold rank 1, indicating share is consolidating at the very top even as a key flavor softens. CBD/THC 1:1 Half Baked Lemonade & Tea (10mg CBD, 10mg THC, 16oz) advanced +10.2% at rank 2 versus Sour Diesel Pre-Roll (1g) at rank 4 with a faster +30.3% trajectory but outside the beverage core, and eight of the top ten are Beverage SKUs. The pattern implies the beverages portfolio remains the commercial anchor while a single pre-roll acts as a testing wedge for non-beverage trial rather than a pivot.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.