Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Headliners is stocked at 52 licensed dispensaries across Massachusetts, with the deepest coverage in Boston, Springfield, Framingham, Greenfield, and Pittsfield. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

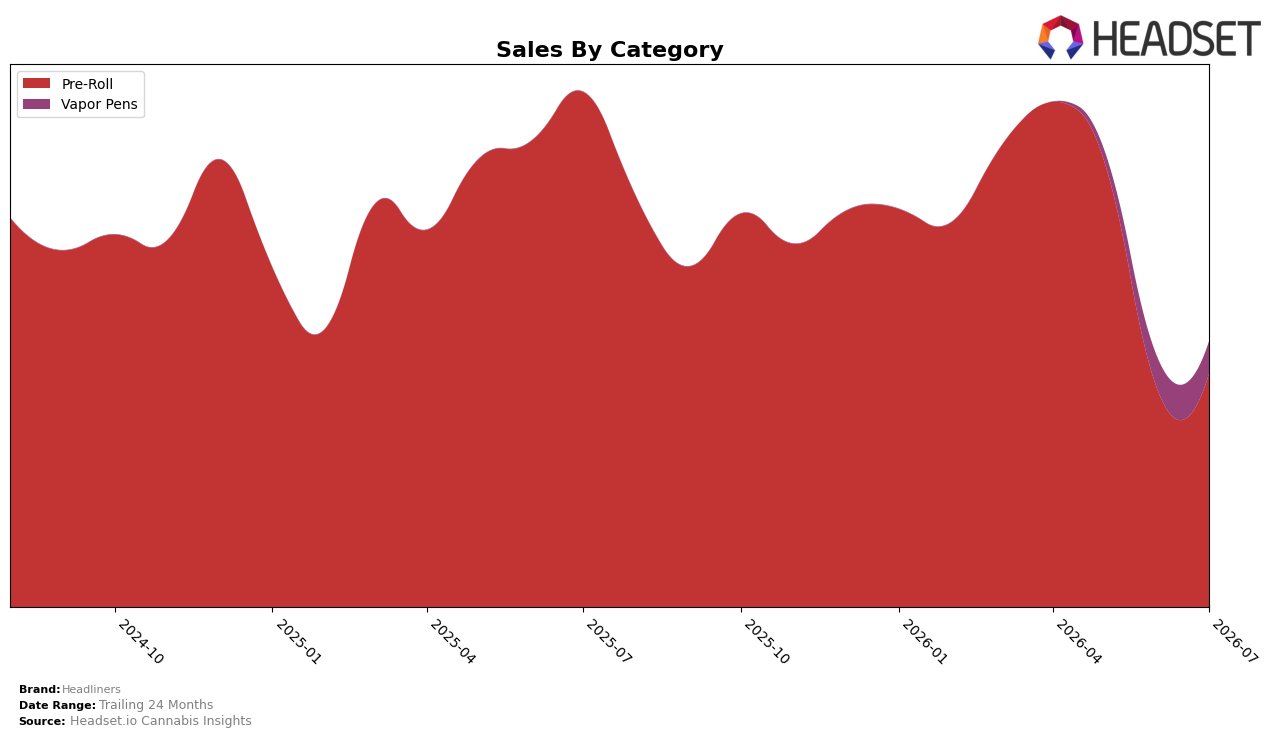

In July 2026, Headliners concentrated 87.90% of sales in Pre-Roll, with Vapor Pens at 12.10%, while overall brand sales fell 48.52% year over year and average price rose 8.73%. Within Pre-Roll, sales declined 54.75% YoY but improved 7.60% month over month, whereas Vapor Pens lacked a YoY baseline but inched up 0.97% MoM; this mix skew indicates reliance on a category with a steep annual contraction alongside a modest near-term recovery. With Pre-Roll ranked 47th in Massachusetts and the top state identified as Massachusetts, the brand’s category emphasis aligns with a mid-pack position; the pattern implies that short-term MoM stabilization in Pre-Roll is insufficient to offset deep YoY erosion, so maintaining a Pre-Roll-heavy mix keeps Headliners anchored to a structurally shrinking base.

The simultaneous 7.60% MoM uptick in Pre-Roll and 0.97% MoM lift in Vapor Pens, against a 48.52% YoY brand decline and a Pre-Roll YoY drop of 54.75%, implies headroom to rebalance toward the higher-priced Vapor Pens, whose average price of $43.06 materially exceeds the $7.62 in Pre-Roll. With 87.90% of volume tied to Pre-Roll while the brand holds rank 47 in Massachusetts Pre-Roll, the mix constrains share momentum; shifting even several share points from Pre-Roll toward Vapor Pens could dilute exposure to the steep YoY drag and reposition the brand toward a price-led, smaller-volume tier that better supports margin as average price rose 8.73%.

Competitive Landscape

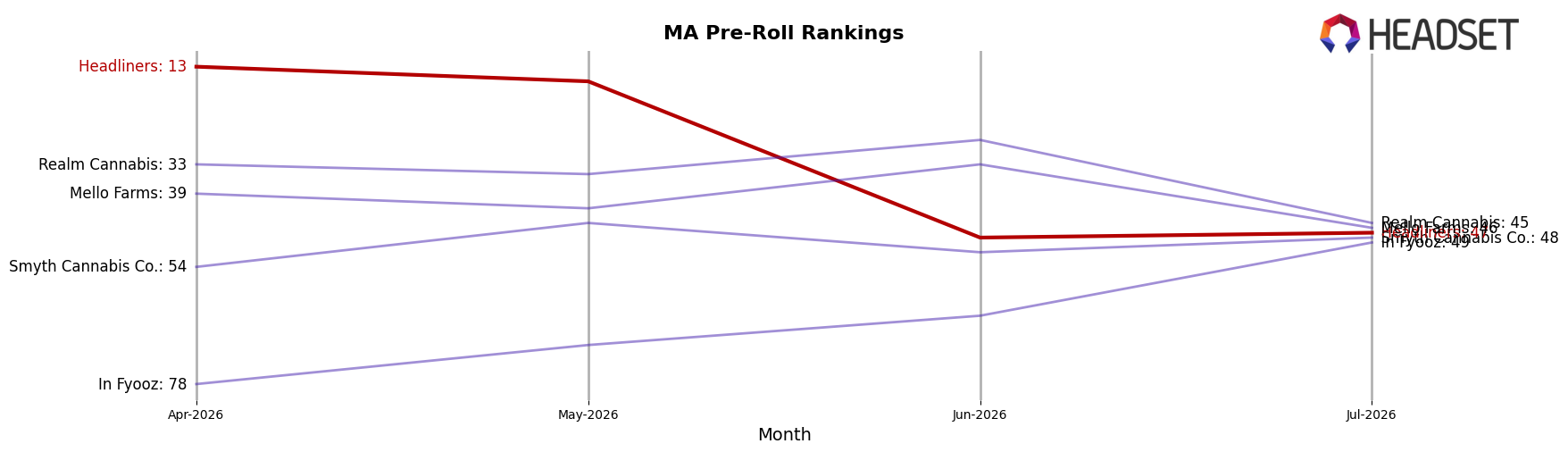

Headliners sits at rank #47 in MA Pre-Roll in July 2026, down 29 positions from #18 year over year and 34 positions from #13 in April 2026, while category leaders moved the other direction as Jeeter held #1 both this year and last and Cali-Blaze advanced from #16 to #2 with a 241.1% YoY sales gain; the brand’s slide from #13 three months ago to #47 now, contrasted with Nature's Heritage improving from #4 YoY to #3 current alongside a 41.9% YoY increase, indicates share is consolidating toward faster-rising competitors, implying Headliners must reverse momentum quickly or cede further ranking ground as leadership hardens at the top.

Notable Products

Champagne Cookies Pre-Roll (1g) posted the steepest movement in July 2026 with a -29.1% month-over-month slide while holding rank 2, and Perfect Cell Pre-Roll (1g) also declined -12.3% at rank 9, indicating demand volatility concentrated in single-gram SKUs rather than pack formats. In contrast, Pura Vida Pre-Roll (1g) rose 27.3% month over month to rank 7, while Rainbow Guava Pre-Roll (1g) sat at rank 1 with $10,047 in sales, and eight of the top ten are single-gram Pre-Roll SKUs, pointing to a lineup leaning on 1g variety rather than multi-pack depth. The mix suggests Headliners is prioritizing breadth within 1g Pre-Rolls, which concentrates risk in fast-cycling singles and calls for selective support of rising SKUs while pruning underperforming strains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.