Market Insights Snapshot

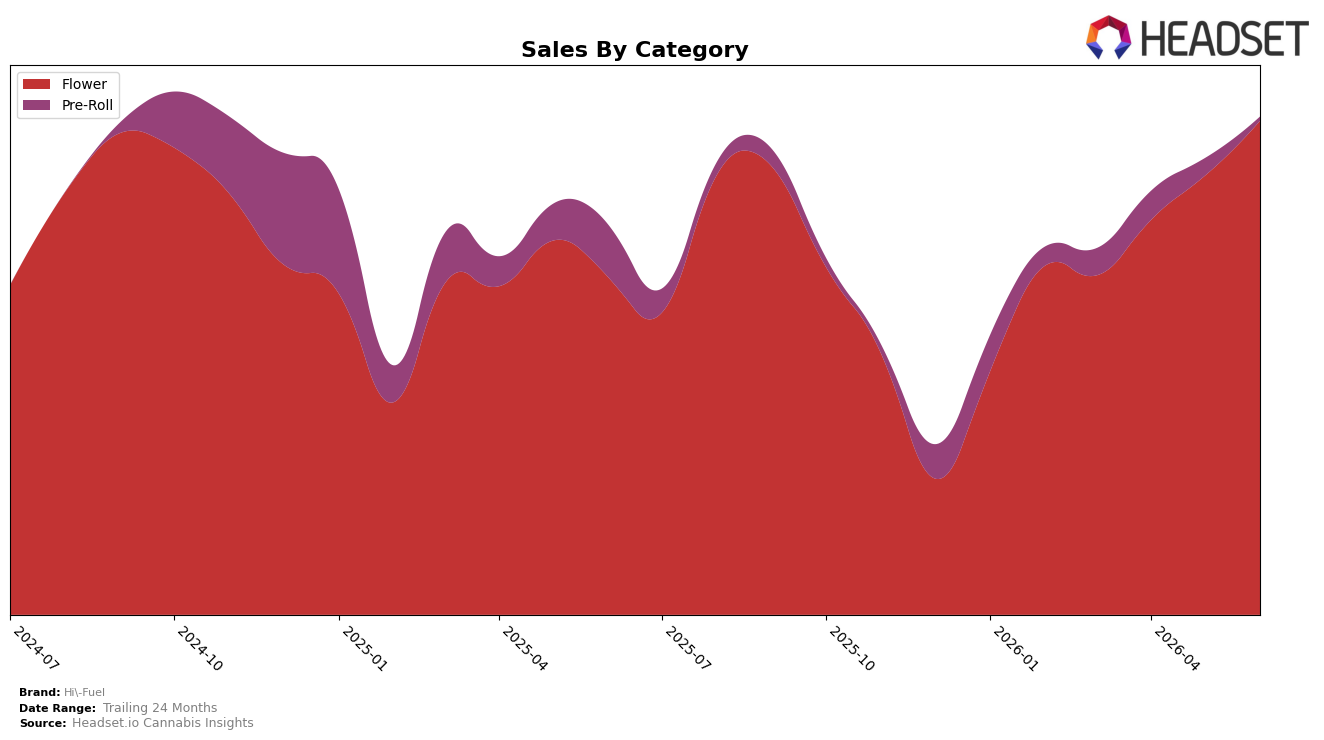

In June 2026, Hi-Fuel concentrated 99.23% of sales in Flower while Pre-Roll slipped to 0.77% share, with Flower up 46.40% year over year and 12.57% month over month versus Pre-Roll down 92.63% YoY and 77.77% MoM; this mix sat alongside a 27.75% brand-level YoY sales increase and a 40.62% YoY drop in average price. With Flower ranked 16th in Colorado and Pre-Roll shrinking steeply, the pattern implies deliberate price-led volume capture in Flower and an exit or deprioritization of Pre-Roll that concentrates risk but drives near-term rank stability in core Flower.

The widening gap—Flower’s 12.57% MoM growth against Pre-Roll’s 77.77% MoM contraction and a 46.40% YoY Flower lift versus a 92.63% YoY Pre-Roll decline—suggests Hi-Fuel is repositioning around a value-forward Flower strategy that trades margin for share and rank consistency. Holding the 16th position in Colorado Flower while average price fell 40.62% YoY and total sales rose 27.75% implies the brand’s near-term edge is volume scale in a single category, which strengthens shelf presence but heightens exposure to Flower price compression and limits diversification upside.

Competitive Landscape

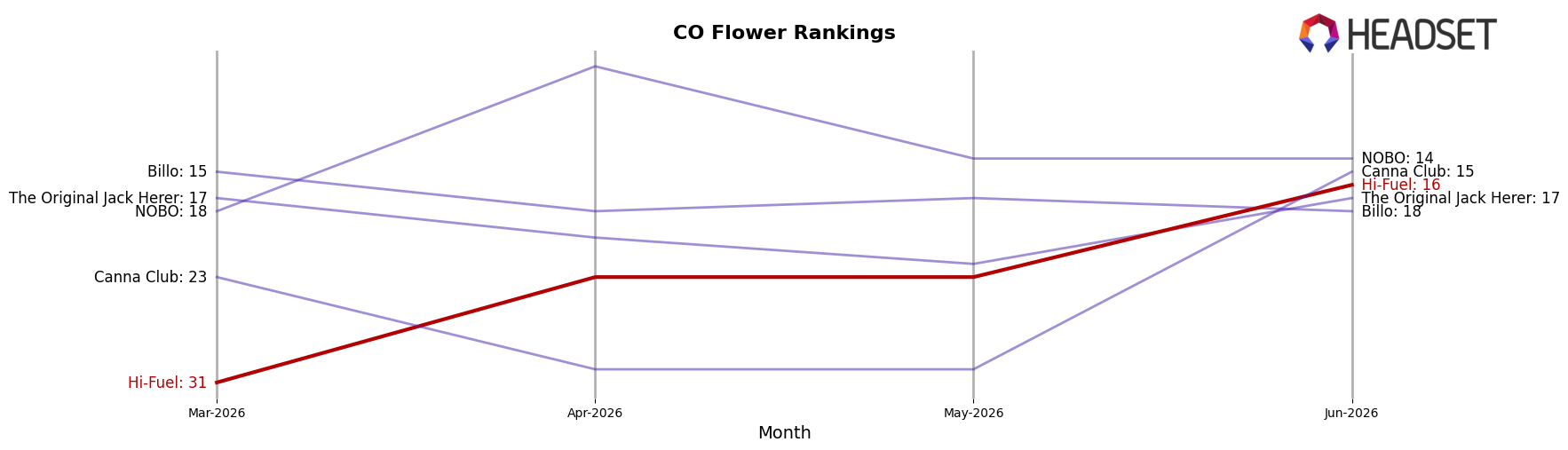

Hi-Fuel sits at rank #16 in CO Flower in June 2026, a 14-place climb from #30 year over year, and a 15-position rise from #31 three months ago; the ascent coincides with hitting a peak rank of #16 in June 2026 and closing a multi-rank gap versus top-tier players. In contrast, Good Chemistry Nurseries slipped from #1 to #3 while posting a -2.83% sales change, whereas Natty Rems surged from #28 to #5 alongside a 220.97% sales lift, indicating that Hi-Fuel’s move from #30 to #16 is outpacing some incumbents but trailing the acceleration of the fastest risers. The pattern implies Hi-Fuel’s rank trajectory is transitioning from mid-pack to contender status, with sustained share capture needed to convert the 14-rank YoY gain into durable top-10 positioning.

Notable Products

Subzero (1g) posted the standout move in June 2026 with a +947.5% month-over-month surge to rank 1, while Permanent Chimera (Bulk) slid -56.7% to rank 8, indicating share is consolidating at the extremes rather than the middle. Lemon Rosé (Bulk) fell -47.1% at rank 7 as Chimera (3.5g) held a top-10 position at rank 10, and with eight of the top ten SKUs in Flower formats the portfolio is heavily concentrated in one category. Tahitian Sherb (Bulk) entered at rank 2 without a prior comparison and Lemon Rose (3.5g) sat at rank 9, and the $39,063 captured by Subzero (1g) suggests a pivot toward premium, fast-moving single-gram offerings alongside bulk volatility. The pattern implies Hi-Fuel is leaning into a barbell mix of high-velocity small formats and selectively supported bulk lines, prioritizing rapid-turn hero SKUs while pruning underperforming Flower variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.