Market Insights Snapshot

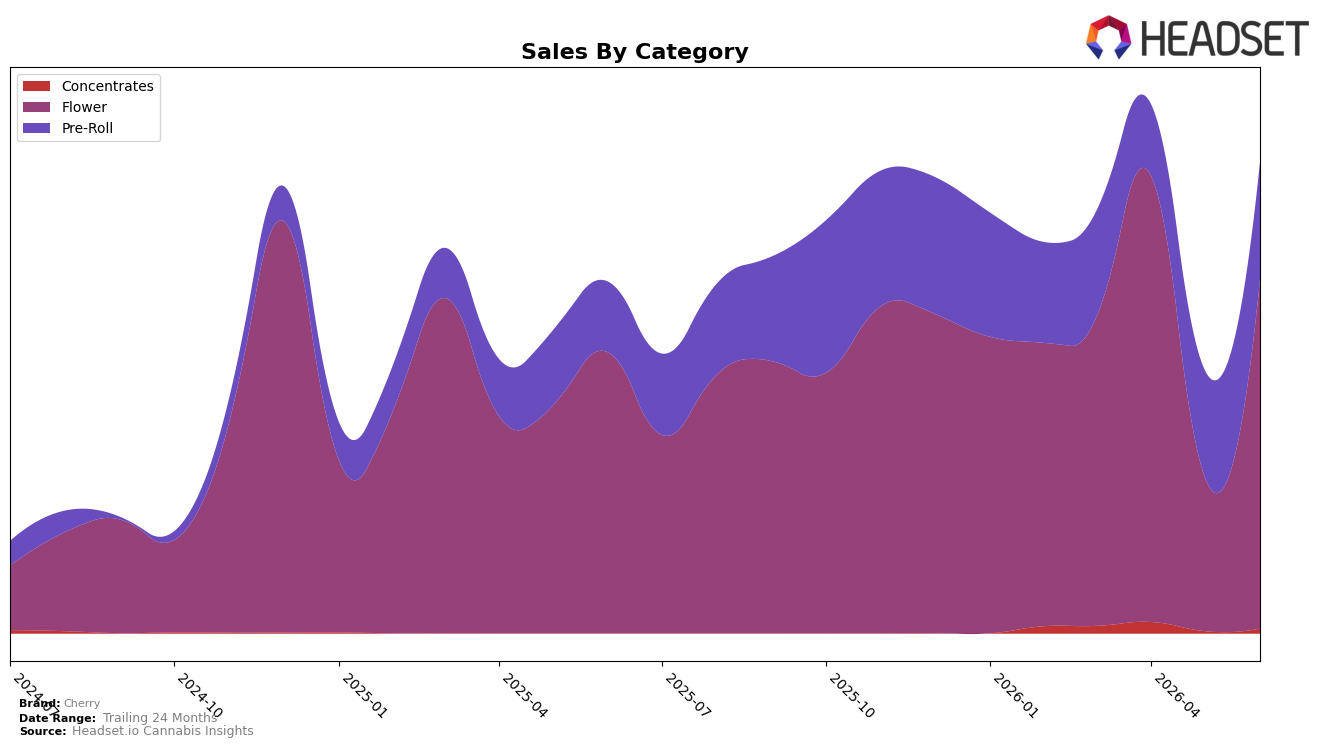

Cherry concentrated 74.11% of June 2026 sales in Flower with a 126.41% month-over-month surge and 24.31% year-over-year growth, while Pre-Roll held 24.90% share with 9.89% MoM and 66.33% YoY gains; Concentrates remained 0.99% share but jumped 111.65% MoM. Despite a 49.49% YoY drop in average price alongside 34.06% YoY brand sales growth, the category mix skewed more heavily to Flower, indicating a volume-led expansion where price elasticity and mix-shift toward lower-priced units likely outweighed pricing pressure.

The pivot toward Flower, coupled with a 31st rank in Flower in Colorado, suggests Cherry is competing most on throughput rather than premium positioning, as a 126.41% MoM lift in its largest category outpaced the 9.89% MoM in Pre-Roll. With Pre-Roll’s 66.33% YoY growth versus Flower’s 24.31% YoY, Cherry’s medium-term gains are diversified, yet the June 2026 spike implies near-term shelf strategy and promotions are optimized for Flower unit acceleration, positioning the brand to trade share on volume now while keeping Pre-Roll as a secondary growth pillar.

Competitive Landscape

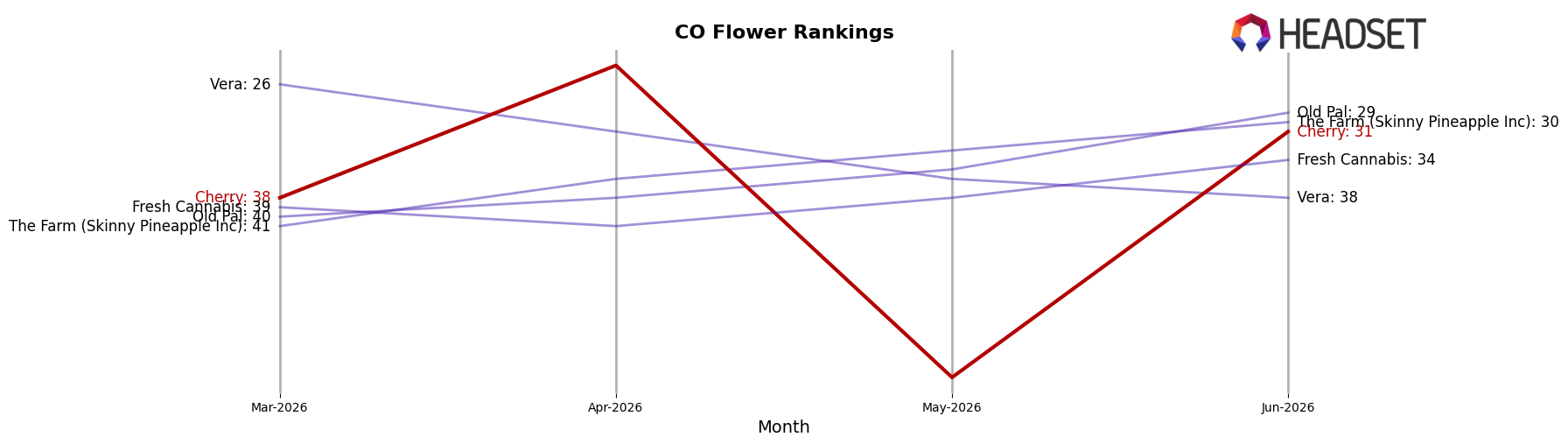

Cherry is ranked #31 in CO Flower in June 2026, improving 10 positions from #41 year over year and rising 7 spots from #38 since March 2026; however, it sits 7 places below its April 2026 peak at #24, indicating mid-year slippage after a spring rise. In contrast, Seed & Strain Cannabis Co. moved from #2 to #1 with 62.79% year-over-year sales growth, while Good Chemistry Nurseries fell from #1 to #3 with a -2.83% sales decline, showing upward pressure at the top end even as Cherry’s relative gains are off-peak. This combination of a 10-rank year-over-year climb and a 7-rank quarter-over-quarter rise, paired with a retreat from the #24 peak, implies Cherry’s trajectory is improving but not yet sustaining top-25 competitiveness.

Notable Products

Cherry x Ajoya - Hybrid Pre-Roll (1g) posted the steepest movement in June 2026, dropping 15.2% month over month to rank 6 while Cherry x Ajoya - Indica Pre-Roll (1g) fell 8.0% at rank 3, indicating softening demand in pre-rolls relative to flower. Ripened Citrus Popcorn (Bulk) holds rank 1 with no reported month-over-month figure and Blockberry (3.5g) sits at rank 2, while four of the top ten are Flower SKUs clustered between ranks 1 and 9, pointing to category concentration at the top of the chart. Cherry x Ajoya - Sativa Pre-Roll (1g) declined 5.0% at rank 4 against stable top-two flower placements and $34,486 in sales for Ripened Citrus Popcorn (Bulk), suggesting mix is tilting toward bulk and eighths over single pre-rolls. The pattern implies Cherry’s commercial direction is consolidating around Flower formats, with pre-roll volatility ceding share to bulk/value-oriented flower that anchors the upper ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.