Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

NOBO is stocked at 89 licensed dispensaries across Colorado, Maine, and Michigan, 54 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Boulder, Aurora, and Northglenn. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

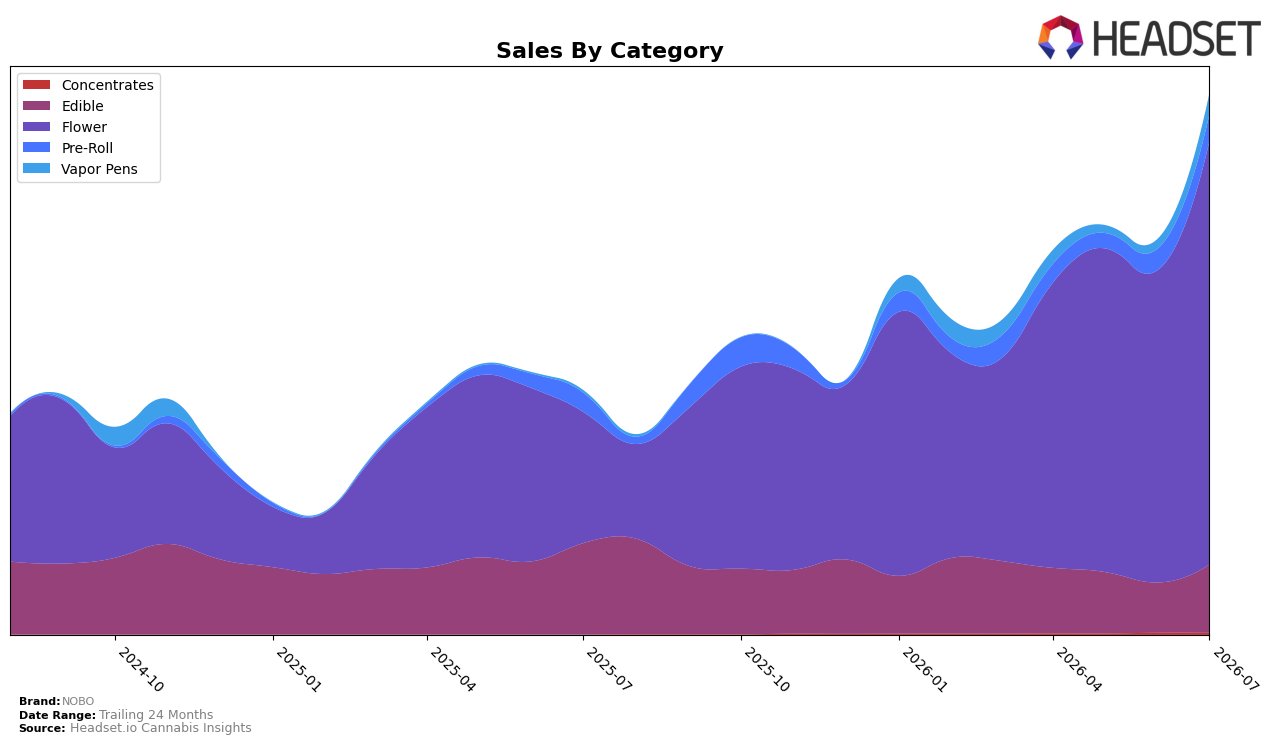

In July 2026, NOBO’s mix tilted heavily toward Flower at 78.33% share with year-over-year growth of 222.92% and month-over-month growth of 35.46%, while Vapor Pens, though only 3.86% of mix, surged 831.23% YoY and 119.96% MoM, signaling a fast-expanding secondary pillar. Edible contracted 25.24% YoY despite a 36.15% MoM lift, and Pre-Roll advanced 40.62% YoY with 25.28% MoM, as Concentrates slipped 3.26% MoM off a minimal 0.31% share. With the average price up 64.87% YoY to $15.41 alongside category-specific price points (Flower at $26.43 and Vapor Pens at $18.05), the pattern implies NOBO is scaling higher-ticket formats while relying on Flower volume to drive overall 122.24% brand sales growth YoY.

The mix shift suggests a two-speed strategy: defend and expand Flower scale while incubating Vapor Pens as the next growth engine, with July 2026’s 119.96% MoM inflection implying acceleration rather than one-off volatility, and a 3.86% share that can expand without cannibalizing the 12.58% Edible base. Given a 6th rank in Flower in Michigan and Flower’s 78.33% share, improving rank efficiency in that lead category becomes the near-term lever, while the outsized YoY of 831.23% in Vapor Pens offers a secondary path to diversify revenue concentration and reduce reliance on single-category swings.

Competitive Landscape

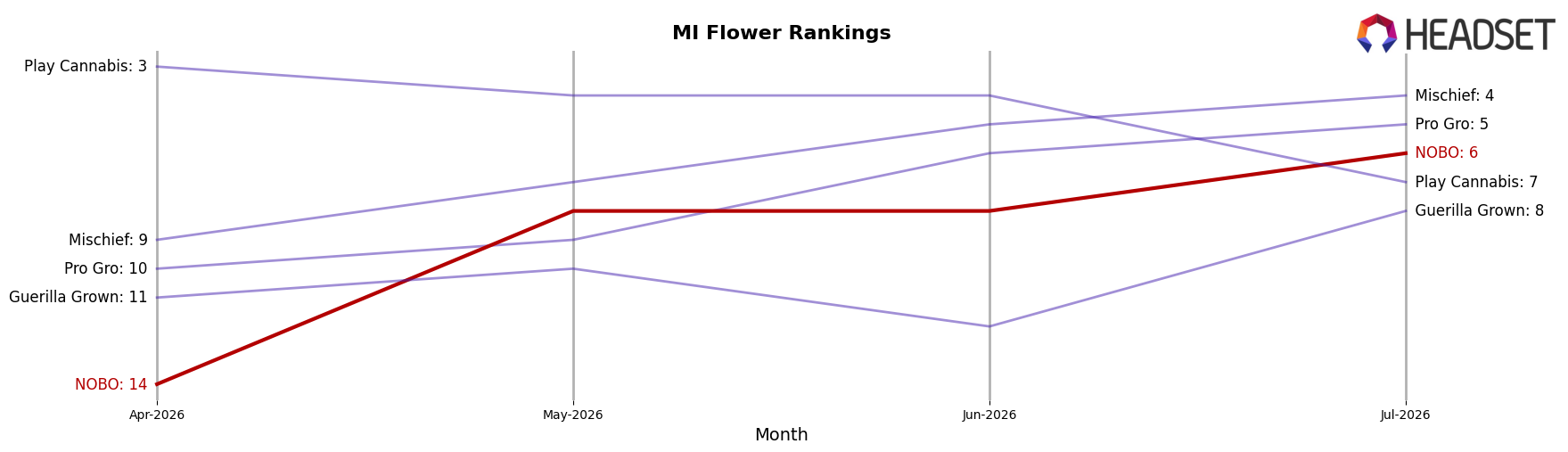

NOBO ranks #6 in Michigan Flower in July 2026, a 19-place climb from #25 year over year, and up 8 positions from #14 in April 2026; this matches a new peak rank of #6 in July 2026, narrowing the gap to the top five. Meanwhile, High Minded held #1 with a -12.5% year-over-year sales change, and Mischief moved from #10 to #4 alongside a 59.4% sales increase, indicating NOBO’s ascent from #25 to #6 is occurring amid mixed competitor momentum and implies that sustained gains over the next quarter could convert proximity to the top five into durable share capture.

Notable Products

THC/CBN 2:1 Purple Pear Sleep Gummies 10-Pack (200mg THC, 100mg CBN) posted the steepest movement in July 2026 with a -14.8% month-over-month decline while holding rank 3, signaling softness in sleep-oriented formulations even as Edibles occupied ranks 1 through 5. Green Apple Gummies 10-Pack (200mg) led at rank 1 with a 0.0% reported MoM change baseline while Cherry Gummies (200mg) in rank 4 inched up +1.8%, and four of the top five are Edible SKUs, indicating concentration around fruit-forward gummies rather than diversification into vapes or beverages. Double Burger (28g) reached rank 8 with $606,045 despite a 0.0% reported MoM change baseline and Lemon Cherry Runtz (28g) at rank 6 underscores that large-format Flower holds secondary share without displacing Edibles from the top-five concentration. The mix implies NOBO is anchored in mainstream gummies with incremental flavor rotation, while Flower provides volume ballast rather than category leadership.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.