Market Insights Snapshot

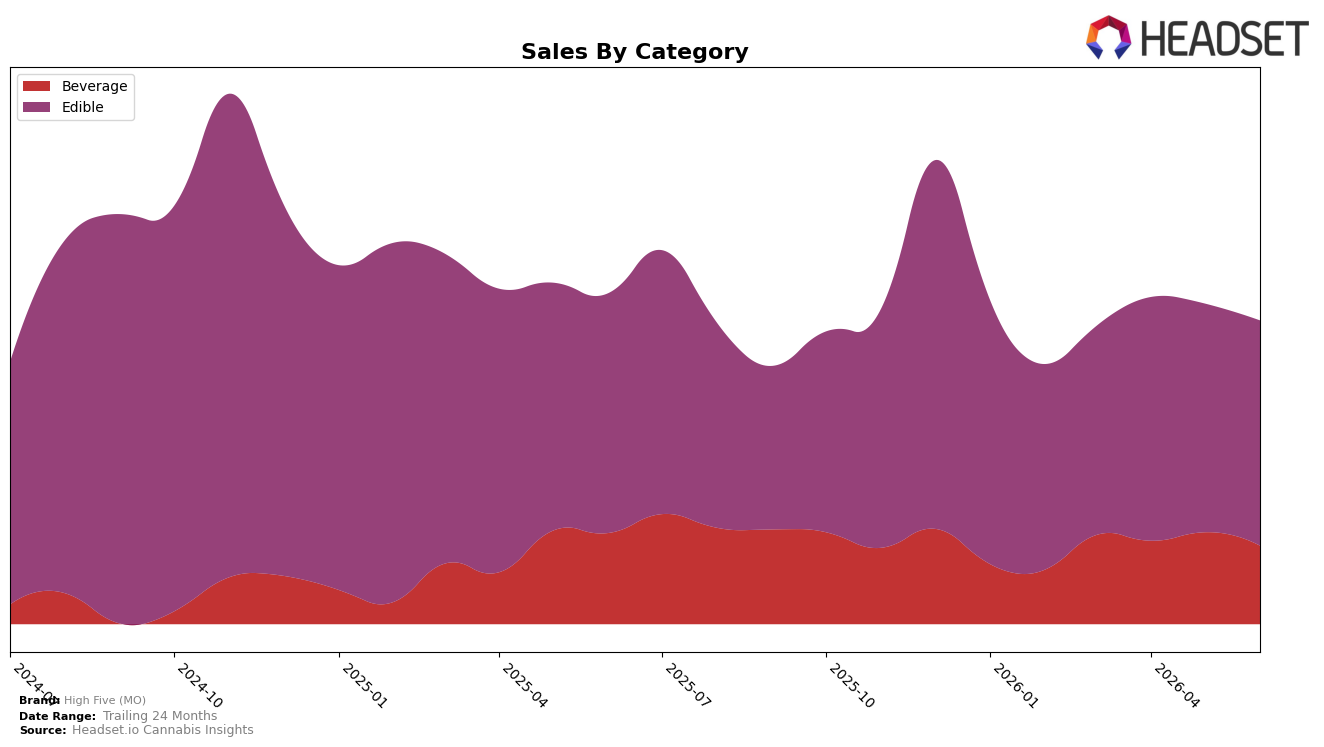

In June 2026, High Five (MO) concentrated 69.28% of sales in Edible with a year-over-year decline of 5.23% and a month-over-month dip of 1.30%, while Beverage accounted for 30.72% of sales but fell faster at 9.77% YoY and 10.29% MoM; average price in the portfolio inched up 0.22% to $26.56, with Edible averaging $25.45 versus Beverage at $29.46. Within Missouri Edible, the brand sat at rank 31, and the mix skews toward the relatively less-pressured Edible versus the steeper Beverage contraction, implying a defensive tilt that preserves share breadth even as total brand sales declined 6.67% YoY.

The sharper 10.29% MoM slide in Beverage alongside a milder 1.30% MoM decline in Edible indicates that High Five (MO)’s positioning leans into value-accessible Edibles (priced 13.64% below Beverage) to stabilize volume, while accepting near-term retrenchment in Beverage. With 69.28% of sales in Edible and a rank of 31 in Missouri Edible, the path to durable placement likely hinges on deepening Edible penetration and selectively pruning Beverage exposure, since the current price ladder and category weights point to incremental gains coming more from mix optimization than from broad price moves.

Competitive Landscape

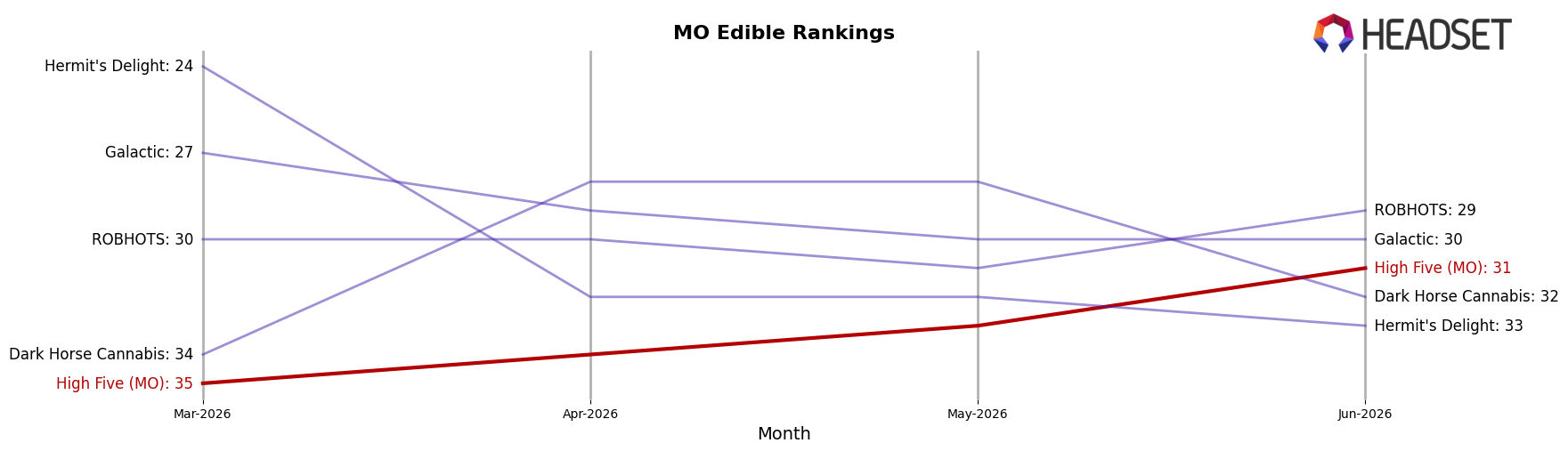

High Five (MO) sits at rank #31 in MO Edible in June 2026, improving 2 positions year over year from #33 and 4 positions since March 2026 from #35, while still 13 spots below its peak at #18 in September 2024; in contrast, Good Day Farm advanced from #4 to #2 as its sales grew 19.4% YoY, and Smokiez Edibles slid from #2 to #5 alongside a 23.4% YoY sales decline. Compared with the stable #1 position for Gron / Grön despite a 13.1% YoY sales drop and the climb of Good Taste from #8 to #4 on 65.3% YoY growth, High Five (MO)’s modest rank gains and distance from its prior #18 peak imply recovery is occurring but the brand is not yet reclaiming prior share in a tier where leaders are consolidating positions despite mixed sales trends.

Notable Products

Huckleberry Lemonade Gummies 20-Pack (100mg) posted the steepest decline at -37.2% and slid to rank 9, while Sour Green Apple Gummies 20-Pack (500mg) fell -32.2% at rank 8, indicating demand is rotating away from certain legacy fruit flavors. At the top, THC/CBN 1:1 Sweet Dark Cherry Gummies 20-Pack (100mg THC, 100mg CBN) retained rank 1 despite a -1.6% dip, and Sour Blue Raspberry High Dose Gummies 20-Pack (500mg) climbed 31.6% to rank 2, showing a split between sleep-oriented 1:1 and high-dose formats. Beverage Stiribles weakened with the 500mg pack down -21.8% at rank 6 and the 300mg pack down -9.5% at rank 7, while the 100mg pack rose 12.8% to rank 4, suggesting price-potency steps are too wide and pulling volume toward the entry format at around $17,090 in June 2026 sales for the 500mg SKU. With seven of the top ten as Edible SKUs and contrasting momentum between high-dose gummies and mid-to-high potency beverage powders, the mix implies High Five (MO) is consolidating around functional gummy use-cases while reassessing premium potency tiers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.