Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

Hight concentrated 55.17% of June 2026 sales in Flower while 44.83% came from Pre-Roll, with Flower up 1,489.76% year over year but down 47.03% month over month, and Pre-Roll up 8,018.97% year over year and up 63.79% month over month. Despite an overall average price falling 40.57% year over year to $18.76, category pricing split with Flower averaging $26.91 and Pre-Roll at $13.67, implying that June 2026 growth leaned on lower-priced velocity in Pre-Roll as Flower retrenched month over month.

These shifts move Hight toward a two-lane positioning where Pre-Roll’s 63.79% month-over-month expansion offsets Flower’s 47.03% month-over-month pullback, keeping the mix nearly balanced at 44.83% versus 55.17% and reducing exposure to a single category shock. With New Jersey Flower rank at 46 and Flower prices materially higher than Pre-Roll ($26.91 vs. $13.67), the pattern implies headroom to trade down within Pre-Roll for share capture while maintaining Flower as a premium anchor, using June 2026’s category divergence to calibrate price-pack architecture rather than chase volume solely in Flower.

Competitive Landscape

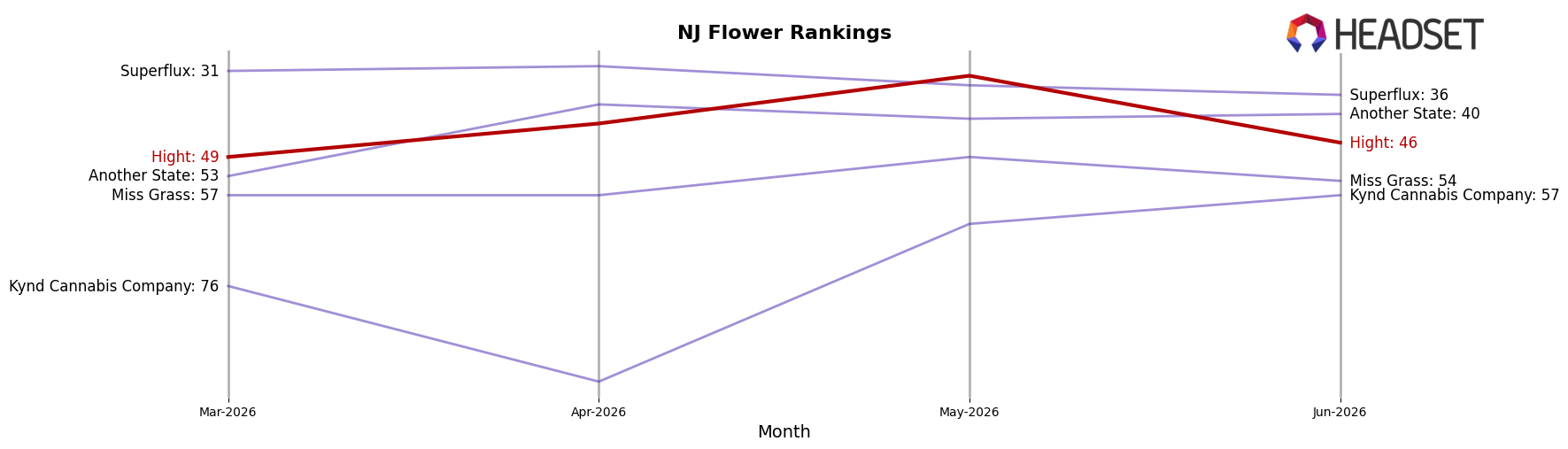

Hight sits at rank #46 in New Jersey Flower in June 2026, improving 33 positions year over year from #79, and edging up 3 spots from #49 in March 2026 while retreating 14 places from its peak at #32 in May 2026; in the same period, Find. climbed from #12 to #1 with 225.99% YoY sales growth and Ozone held near the top at #2 despite a 10.61% YoY sales decline, indicating Hight’s recent pullback after a May 2026 peak is more about short-term volatility than a reversal of a broader upward rank trend.

Notable Products

Cheddar Cheeze (3.5g) posted the steepest decline in June 2026 at -33.3% while slipping to rank 4, whereas Pineapple Donut Smalls (7g) surged +57.4% to rank 2 with $48,220 in sales, creating a split storyline inside Flower. Lemon Fresh (3.5g) also contracted -15.9% yet held rank 1, so the top slot is now defended by a shrinking SKU as momentum shifts to value-driven pack sizes. Four of the top ten are Pre-Roll SKUs clustered at ranks 3 through 10, indicating assortment gravity is tilting toward multi-pack inhalables even as Flower remains the ticket to rank 1. The mix implies Hight’s commercial direction is pivoting toward accessible, higher-count formats while legacy Flower leaders require pricing or format refresh to prevent further share transfer.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.