Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

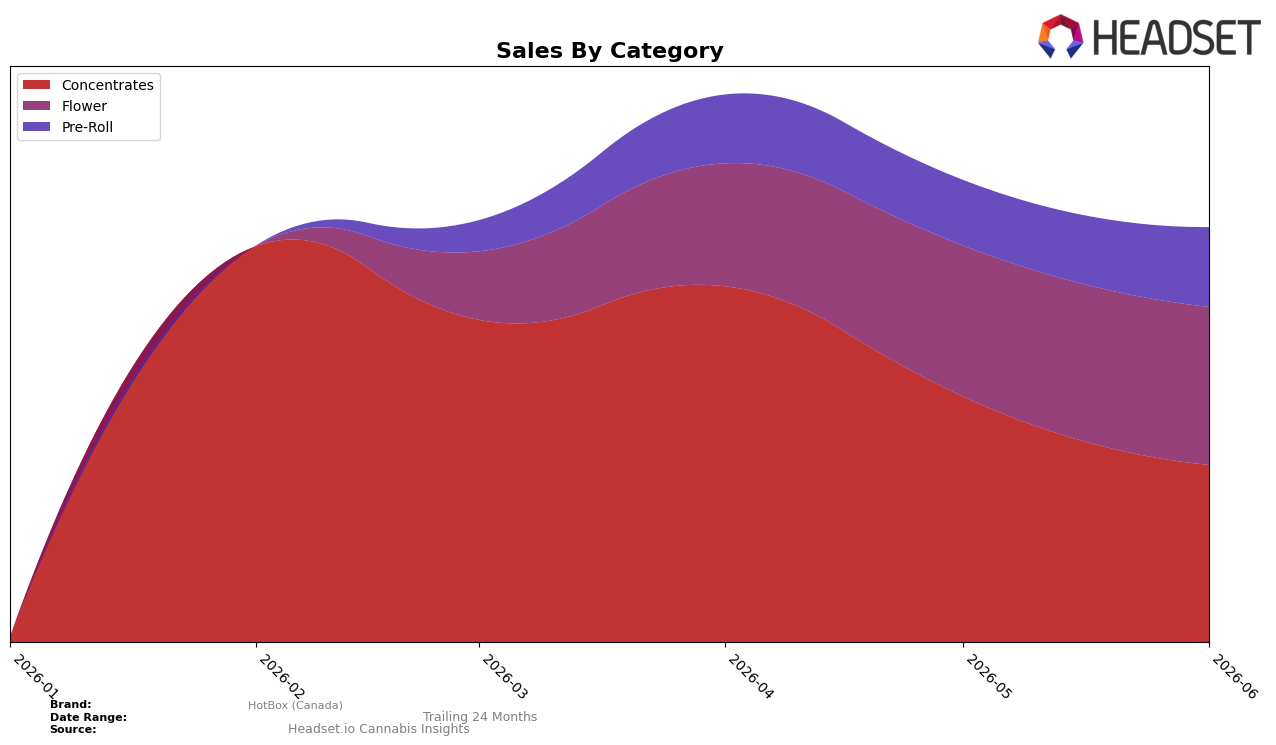

HotBox (Canada) concentrated its June 2026 mix in Concentrates at 42.72% share with a month-over-month decline of 27.90%, while Flower held 38.08% share with a 4.64% month-over-month gain and Pre-Roll reached 19.21% share with a 21.73% month-over-month increase. Average prices diverged materially across the mix, with Concentrates at $35.44 versus Flower at 67.91 and Pre-Roll at 15.35, indicating that the largest share category carried mid-tier pricing while the rising Pre-Roll segment remained value-oriented; this pattern implies a shift toward lower-priced volume growth as premium-priced Flower expands more slowly than Pre-Roll but offsets part of the Concentrates pullback.

In positioning terms, the 27.90% month-over-month drop in Concentrates alongside a 21.73% month-over-month rise in Pre-Roll suggests wallet share is rotating from extract-led baskets to accessible inhalables, while the 4.64% month-over-month gain in Flower keeps HotBox (Canada) present in higher-ticket trips. With a rank of 63 in Flower in Alberta and a 38.08% internal share for Flower versus 19.21% for Pre-Roll, the current mix implies HotBox (Canada) is leaning on breadth across price tiers to stabilize share rather than concentrating on a single flagship form factor, positioning the brand to trade customers between value Pre-Rolls and premium Flower as Concentrates volatility persists.

Competitive Landscape

HotBox (Canada) sits at rank #63 in AB Flower for June 2026, improving 33 positions from #96 in March 2026, and setting a new peak rank at #63 in June 2026 while the year-over-year rank is unavailable. In contrast, Pure Sunfarms advanced to #1 with a +4 YoY rank change and +20.1% sales growth, while Back Forty / Back 40 Cannabis holds #2 with a +2 YoY rank change despite a -23.5% sales decline; this juxtaposition indicates that top-tier share is fluid even with mixed sales trends. The combination of a 33-rank climb over three months and a first-time peak at #63 implies HotBox (Canada) is moving from the long tail toward mid-pack relevance, but sustained advancement will require converting short-term rank momentum into consistent month-over-month share gains.

Notable Products

Sour Diesel RSO Dabber (1g) posted the steepest move in June 2026 with a -42.3% month-over-month drop and sat at rank 7, while Rockstar Kush Pre-Roll (1g) surged 112.9% month-over-month to rank 1. Death Bubba Shatter (1g) declined -10.6% and ranked 3, contrasting with Game Over (14g) up 13.5% at rank 2. Three of the top ten are Pre-Roll SKUs and four are Concentrates, indicating a polarized mix where value-driven Pre-Rolls are gaining share as several concentrates retrench.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.