Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

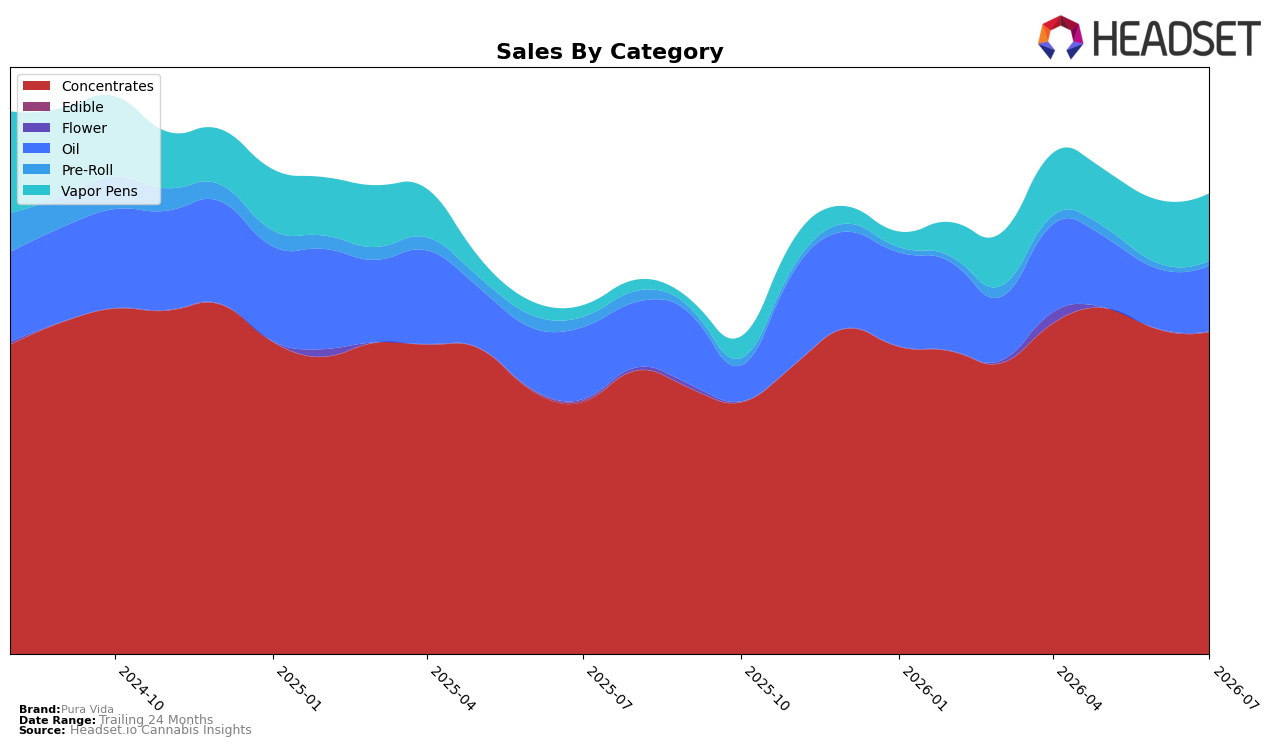

Pura Vida’s category mix in July 2026 concentrated 70.13% of sales in Concentrates, where sales grew 27.76% year over year but slipped 0.79% month over month; Vapor Pens expanded to 14.58% share with a 487.71% year-over-year surge and 6.16% month-over-month lift, while Oil held 14.25% share despite an 8.67% year-over-year decline and a 9.74% month-over-month gain. Pre-Roll contracted to 1.04% share with a 51.85% year-over-year drop and a 9.39% month-over-month decline. With a rank of 2 in Concentrates in Ontario, the mix implies the brand is anchored in a leading category while actively reallocating growth toward Vapor Pens and stabilizing Oil; the pattern points to deliberate diversification to mitigate single-category volatility.

These shifts suggest Pura Vida is reinforcing a premium-extract identity while broadening inhalable touchpoints: a 27.76% year-over-year lift in Concentrates alongside a 0.79% month-over-month dip indicates a maturing core, whereas a 487.71% year-over-year jump and 6.16% month-over-month rise in Vapor Pens signal acquisition or SKU expansion feeding incremental share. The 8.67% year-over-year decline but 9.74% sequential growth in Oil indicates a pricing or assortment reset that is regaining traction, and the 51.85% year-over-year drop with a 9.39% month-over-month decline in Pre-Roll confirms de-prioritization. Net effect: the brand is trading short-term breadth (Pre-Roll pullback) for depth in extracts and pens, positioning for higher repeat in Concentrates while using Vapor Pens as the near-term growth engine.

Competitive Landscape

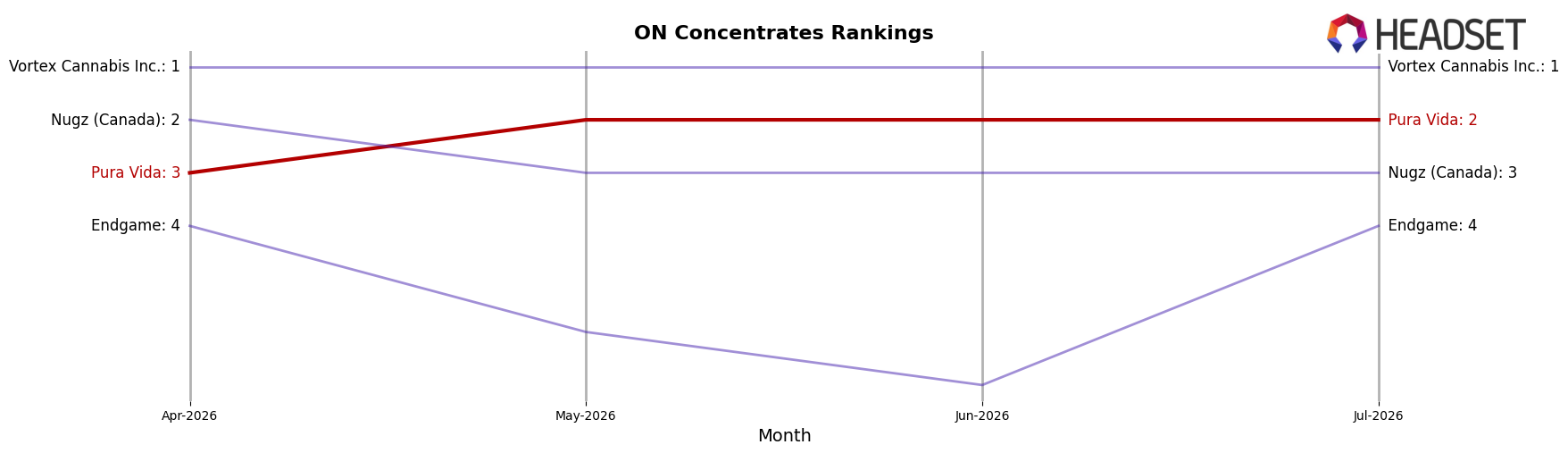

Pura Vida ranks #2 in ON Concentrates as of July 2026, up two positions from #4 year over year, and one position from #3 in April 2026; this climb coincides with a peak rank of #2 in July 2026 and places it directly behind Vortex Cannabis Inc., which held #1 both year over year and in July 2026 while growing sales 10.8%, and ahead of Nugz (Canada) at #3 with a 1.2% sales lift as well as Endgame, which slid from #2 to #4 with a 42.0% sales decline; the directional gap suggests Pura Vida’s upward rank trajectory is driven more by relative share gains against weakening incumbents than by absolute market expansion, implying continued pressure to convert that position into sustained share against the stable #1.

Notable Products

Pineapple Express Jumbo Slab Shatter (1.2g) posted the steepest movement in July 2026 with a -25.8% month-over-month drop and slid to rank 5, while Venom OG Jumbo Slab Shatter (1.2g) moved up on a +27.5% lift to rank 7. At the top, Sativa Honey Oil Dispenser (1g) held rank 1 with a +4.6% gain, and Pineapple Express Live Resin Cartridge (1g) advanced to rank 2 on +17.7% growth. With six of the top ten coming from Concentrates and performance splitting between a -25.8% contraction and +27.5% expansion within that group, the mix points to Pura Vida leaning into higher-velocity concentrate formats while pruning weaker cuts.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.