Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

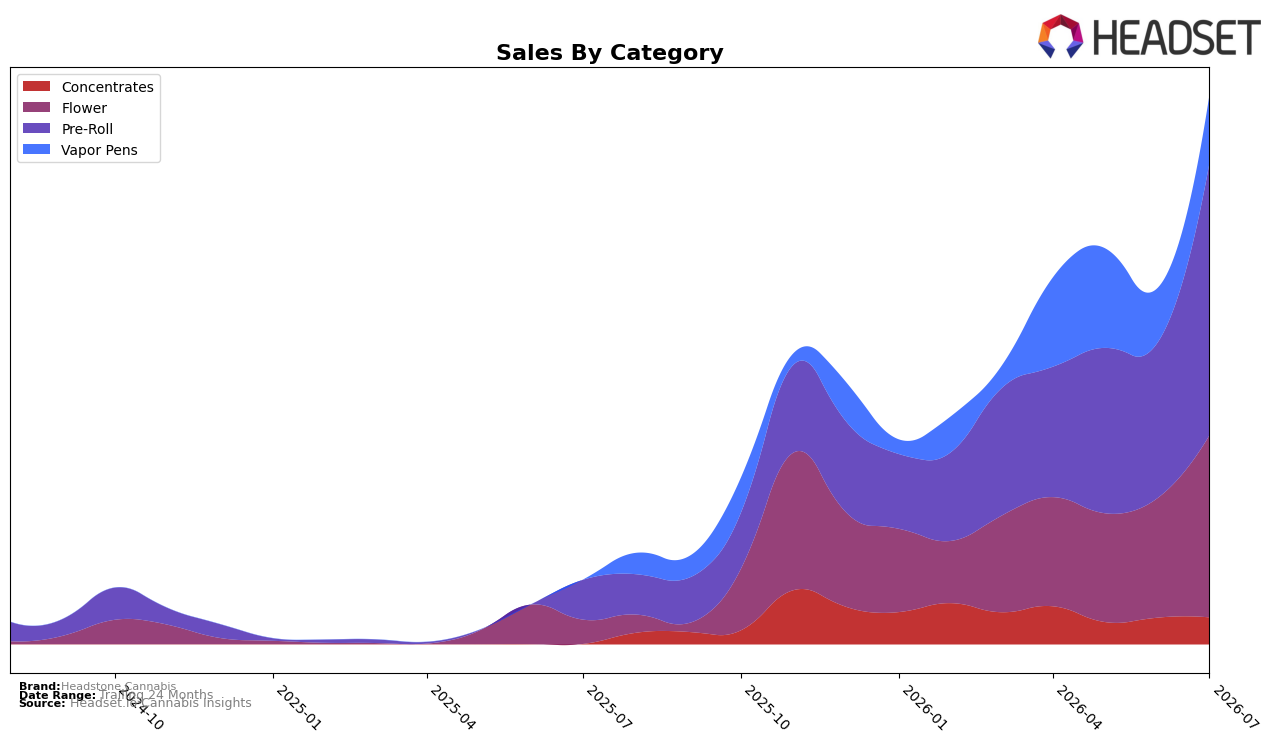

Headstone Cannabis concentrated nearly half of July 2026 volume in Pre-Roll at 49.57% share with 74.84% MoM growth and 586.37% YoY, while Flower held 33.14% share with 52.04% MoM and 656.32% YoY. Vapor Pens accounted for 12.39% share with 25.44% MoM but no YoY baseline, and Concentrates, though only 4.90% share, posted 1.01% MoM alongside a 9,194.78% YoY spike. With an average price up 11.30% YoY to $23.25 and category price points diverging (Pre-Roll at 16.23 vs Flower at 46.08), the mix shift implies the brand is scaling volume in lower-ticket formats while preserving premium-priced Flower growth, positioning the portfolio to capture both value-driven and higher-ticket buyers.

Pre-Roll’s 49.57% share and rank 17 in Alberta signal traction in the highest-velocity segment, yet Flower’s 656.32% YoY growth against a smaller 33.14% share suggests headroom to trade up without losing Pre-Roll momentum. The 25.44% MoM in Vapor Pens coupled with a 12.39% share indicates a foothold for cross-format retention, while the 9,194.78% YoY in Concentrates on just 4.90% share points to a niche trial phase rather than a volume engine. Taken together, July 2026 mix dynamics imply a barbell positioning: defend rank via Pre-Roll scale in Alberta while expanding margin through higher-priced Flower and measured penetration in extract formats.

Competitive Landscape

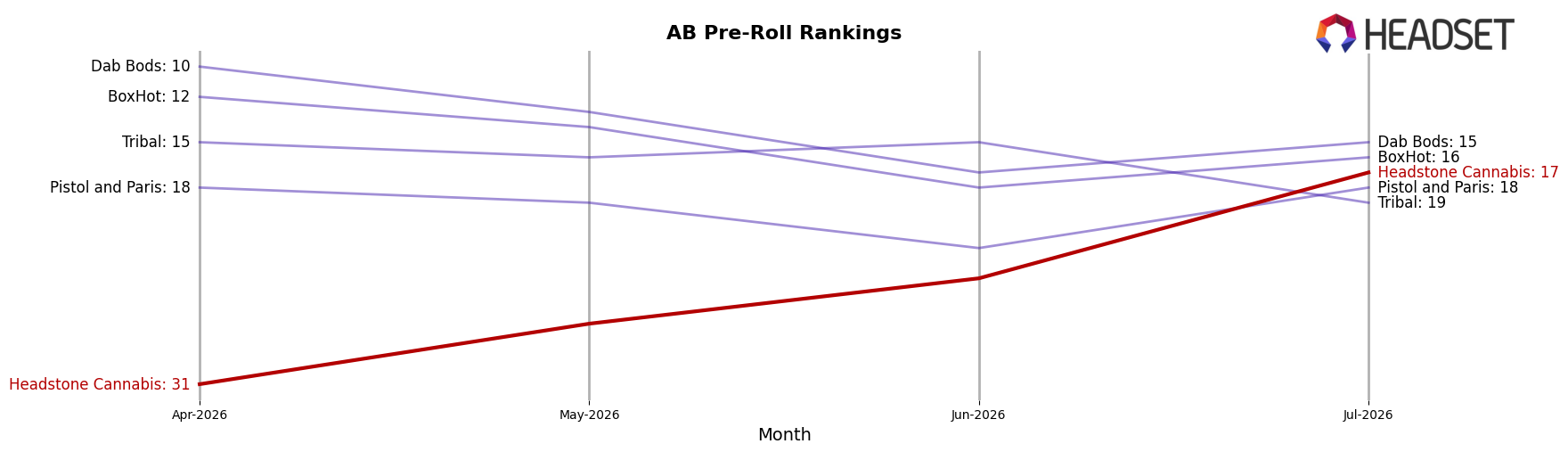

Headstone Cannabis sits at rank #17 in AB Pre-Roll in July 2026 after climbing 54 positions year over year from #71, and rising 14 places from #31 in April 2026 to reach its peak rank of #17 in July 2026; by contrast, Back Forty / Back 40 Cannabis moved from #6 to #2 with a 34.3% year-over-year sales change, while category leader General Admission held #1 year over year despite a 14.5% decline. With Space Race Cannabis sliding from #2 to #3 on a 37.9% drop and Thumbs Up Brand jumping from #19 to #5 on 138.3% growth, the mix above Headstone Cannabis is volatile, and the brand’s 54-rank YoY surge combined with a 14-rank gain since April 2026 implies momentum into the middle tier where sustained retention tactics could convert recent share wins into a stable top-15 foothold.

Notable Products

Lamb of God Pre-Roll 5-Pack (2.5g) delivered the standout movement with a 278.7% month-over-month surge to rank 1, while BlackBerry Cherry Pre-Roll 5-Pack (2.5g) also spiked 216.8% to rank 4; by contrast, Flawless Clarity Diamond Infused Pre-Roll 3-Pack (1.5g) slipped 0.9% at rank 7 and Adam & Eve Pre-Roll 2-Pack (1g) fell 6.7% at rank 9. Four of the top ten are Pre-Roll SKUs, including steady mid-table traction from Ghoul Fuel Pre-Roll (0.5g) at rank 2 with +9.2% and Demon Deep Sleep Pre-Roll (0.5g) at rank 3 with +20.4%, implying Pre-Roll breadth is anchoring visibility while premium multi-packs are pulling the category up the rankings.

Outside Pre-Rolls, Lamb of God (7g) in Flower jumped 134.6% to rank 5 as a complementary upsell to the leading Pre-Roll, whereas Black Mountain Morgue Cured Resin Cartridge (1g) rose 43.0% to rank 6 while the Afterlife Cured Resin Disposable (1g) entered at rank 8 with $48,473 in sales; Graveyard Garden Pre-Roll 10-Pack (5g) entered at rank 10, adding depth at higher pack sizes. The concentration of large MoM gains at ranks 1, 4, and 5 alongside modest negatives at ranks 7 and 9 indicates the portfolio is tilting toward higher-velocity formats and larger pack sizes to consolidate share at the top of the chart.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.