Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

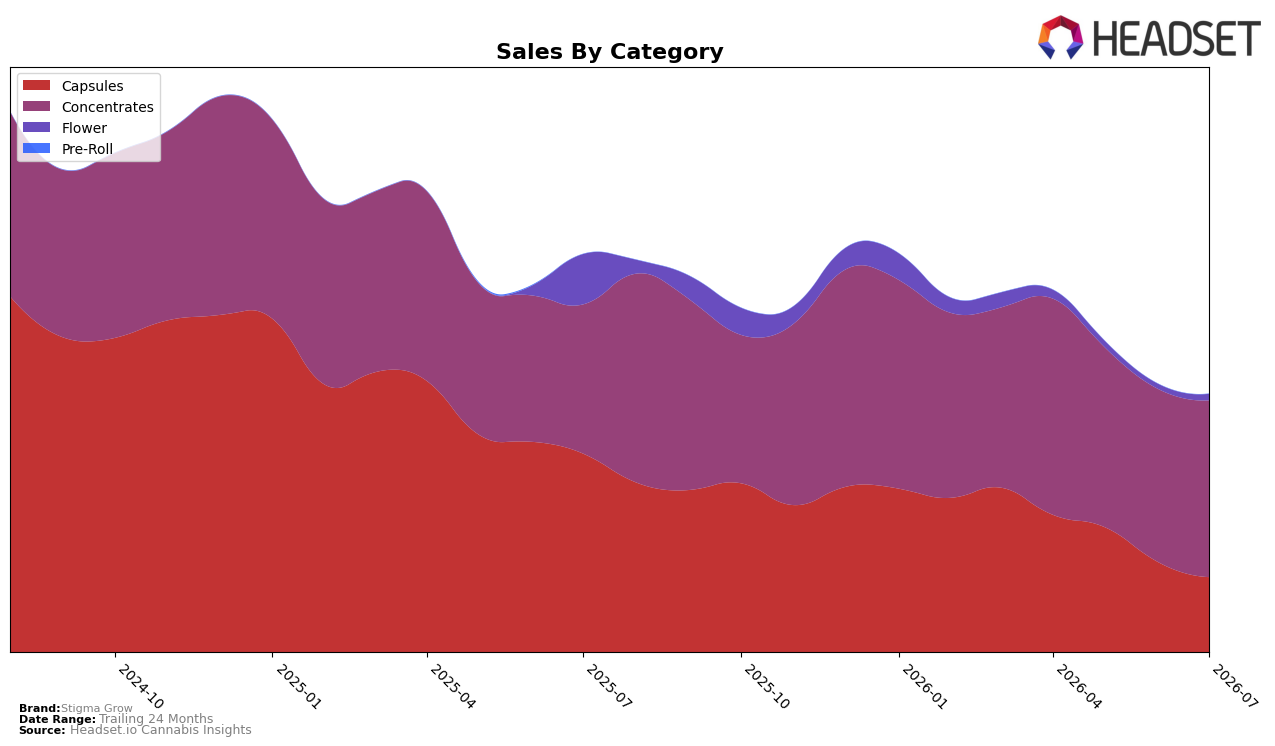

In July 2026, Stigma Grow concentrated its mix heavily into Concentrates at 68.53% share with year-over-year growth of 18.54% and month-over-month growth of 2.10%, while Capsules fell to 29.03% share with a year-over-year decline of 62.31% and a month-over-month decline of 16.98%. Flower remained a small 2.43% share but posted a 29.28% month-over-month lift against an 87.48% year-over-year drop, and the brand’s average price contracted 6.35% year over year as Concentrates averaged $31.89. This tilt toward Concentrates and away from Capsules suggests the brand is reallocating demand into a category with current momentum while tolerating steep year-over-year contraction in legacy formats, implying a deliberate push to stabilize volume via higher-turn segments rather than breadth across slower-moving categories.

That shift positions Stigma Grow to be judged primarily on its performance in Concentrates, where it holds rank 10 in Alberta and captured 68.53% of its mix, but it also heightens exposure if category-specific pricing or availability tightens given the 6.35% year-over-year price decrease. With Capsules down 62.31% year over year and 16.98% month over month while Flower’s 29.28% month-over-month gain comes off a 2.43% share base, the portfolio now relies on sustaining low-single-digit monthly growth in Concentrates to offset broader brand sales decline of 35.18% year over year, implying that incremental rank improvement in Concentrates is the critical lever for near-term recovery.

Competitive Landscape

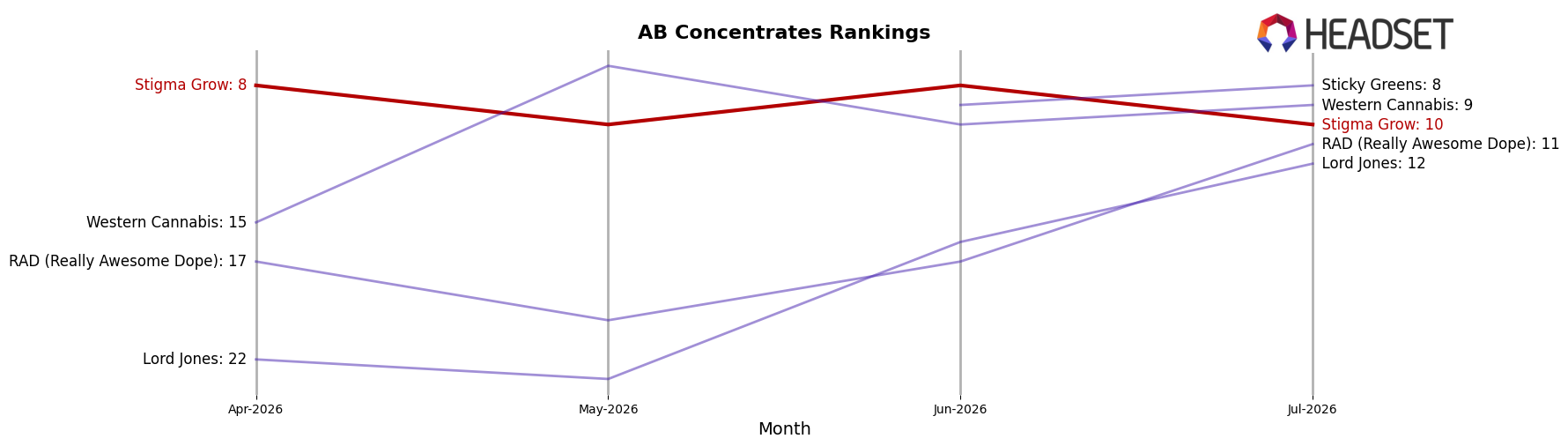

Stigma Grow sits at rank #10 in AB Concentrates for July 2026, up 9 positions from #19 year over year, though it slipped 2 spots from its peak at #8 in June 2026. In the same period, BoxHot moved from #2 to #1 while growing sales by 26.0%, and Endgame fell from #1 to #2 with a 25.5% sales decline, indicating a competitive reshuffle at the top that contrasts with Stigma Grow’s mid-tier climb. Meanwhile, Dab Bods held #3 with an 83.1% sales increase and 3Saints rose from #5 to #4 with a 50.4% gain, underscoring that Stigma Grow’s YoY rise to #10 is occurring amid faster-moving rivals, implying its trajectory is improving but may plateau without acceleration beyond the #8–#10 band.

Notable Products

Phoenix Tears RSO (1g) posted the steepest decline at -54.3% month over month while holding rank 1, indicating a volume reset even as it remained the category anchor; by contrast, Rippin Razz 2.0 Shatter (4g) surged +84.8% to rank 4, suggesting demand is shifting toward value-oriented concentrate formats within the top tier. July 2026 also saw Grape Limeade (14g) leap +494.8% into rank 7 while Twisted Citrus (14g) fell -48.3% to rank 9, and two of the top ten were Flower SKUs, pointing to a broader basket mix that is no longer dominated only by concentrates. The combination of a -19.3% slide for Indica RSO Capsules 25-Pack (250mg) at rank 2 and a +22.8% lift for Phoenix Tears Honey Oil (1g) at rank 5, alongside one flagship above $99,736 in sales, implies Stigma Grow is trading consumers between formats rather than growing the core RSO pie.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.