Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

I-70 Extracts (I70E) is stocked at 24 licensed dispensaries across Colorado, with the deepest coverage in Denver, Aurora, Colorado Springs, Thornton, and Broomfield. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

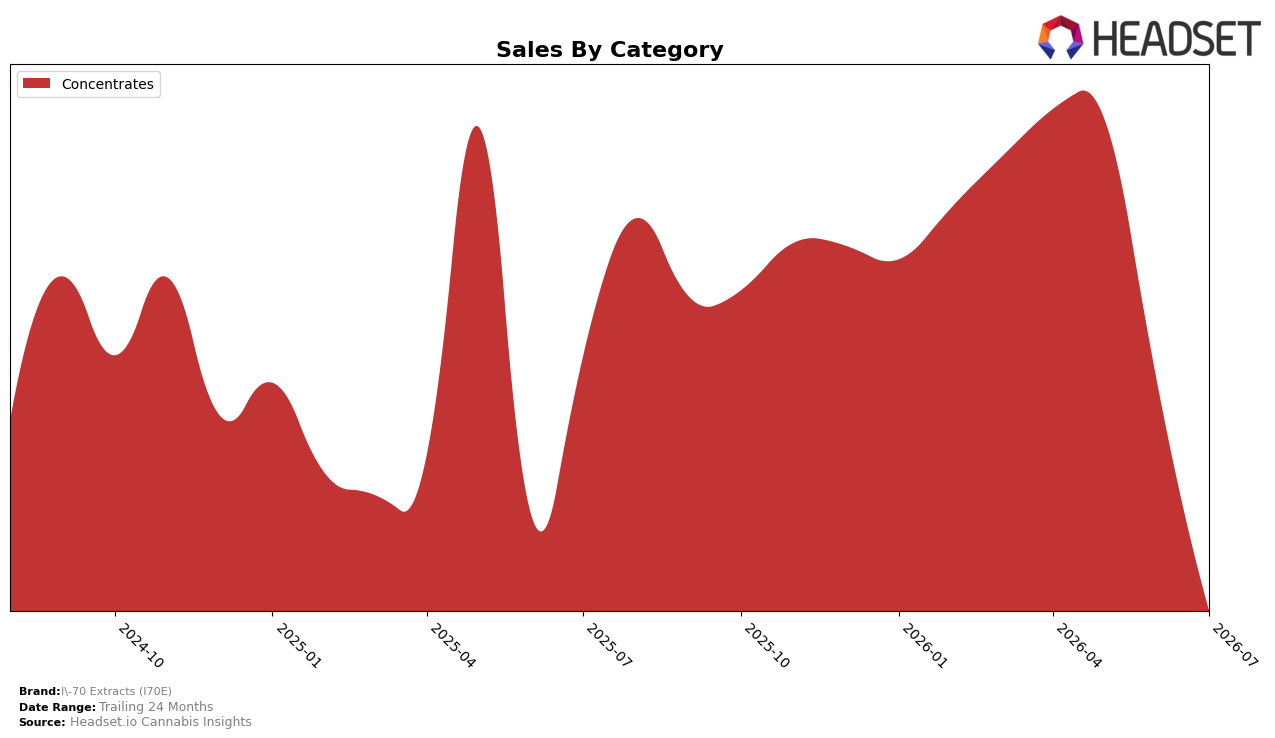

In July 2026, I-70 Extracts (I70E) operated as a single-category brand with Concentrates at 100.0% of mix, while year-over-year sales in Concentrates fell 79.02% and month-over-month declined 76.99%. The brand’s average price dropped 33.31% YoY to $8.31, coinciding with a 69.54% sales decline over 24 months and a 79.02% brand-level YoY contraction, indicating the portfolio is concentrated in a price-compressed niche where volume did not offset the price cut.

Positioning-wise, the all-in Concentrates stance at 100.0% share coupled with a rank of 48 in Colorado suggests limited shelf leverage, as the 76.99% MoM sales decline outpaced the 33.31% YoY price decrease and the 79.02% YoY sales drop. With no diversification into adjacent categories and a July 2026 average price at $8.31, the pattern implies a low-price, low-rank posture where deeper discounting did not translate to defensible rank or share momentum within Concentrates.

Competitive Landscape

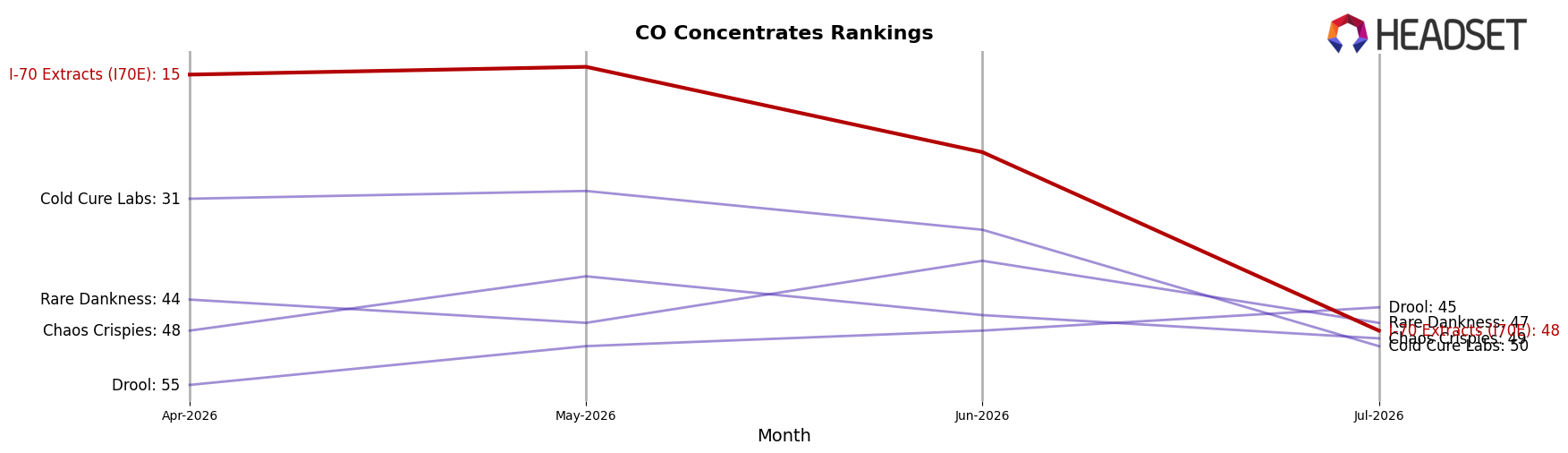

I-70 Extracts (I70E) sits at rank #48 in Colorado Concentrates in July 2026, down 19 places from #29 year over year and sliding 33 spots from #15 just three months ago; despite peaking at #14 in May 2026, the brand’s trajectory indicates a retrenchment rather than a temporary blip. In contrast, Amber held #1 with a 48.5% year-over-year sales increase while 710 Labs stayed at #2 with a 0.0% year-over-year sales change, and Sunshine Extracts advanced to #3 from #8 alongside a 43.3% year-over-year lift; this divergence—competitors holding or gaining share while I-70 Extracts (I70E) moved from #14 in May 2026 to #48 in July 2026—implies momentum loss that will require a reset of assortment or channel focus to regain mid-tier relevance.

Notable Products

Mile High GMO Wax (1g) posted the steepest month-over-month decline at -86.9%, falling to rank 8 while Marsh-Mellow Wax (1g) also sank -74.6% at rank 7, indicating demand has sharply retreated in the lower half of the leaderboard. At the top, Concord Sherbet Sugar Wax (1g) held rank 1 and Goldmember Sugar Wax (1g) sat at rank 2 despite Stardawg Sugar Wax (1g) plunging -78.2% to rank 3, so leadership is concentrated even as mid-pack volatility intensifies. With all ten entries in Concentrates and four of the top six tied to Sugar or Sherbet wax formats, the mix skews narrowly toward a single texture and potency cue, implying I-70 Extracts (I70E) will need either price or format diversification to stabilize volume cadence.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.