Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

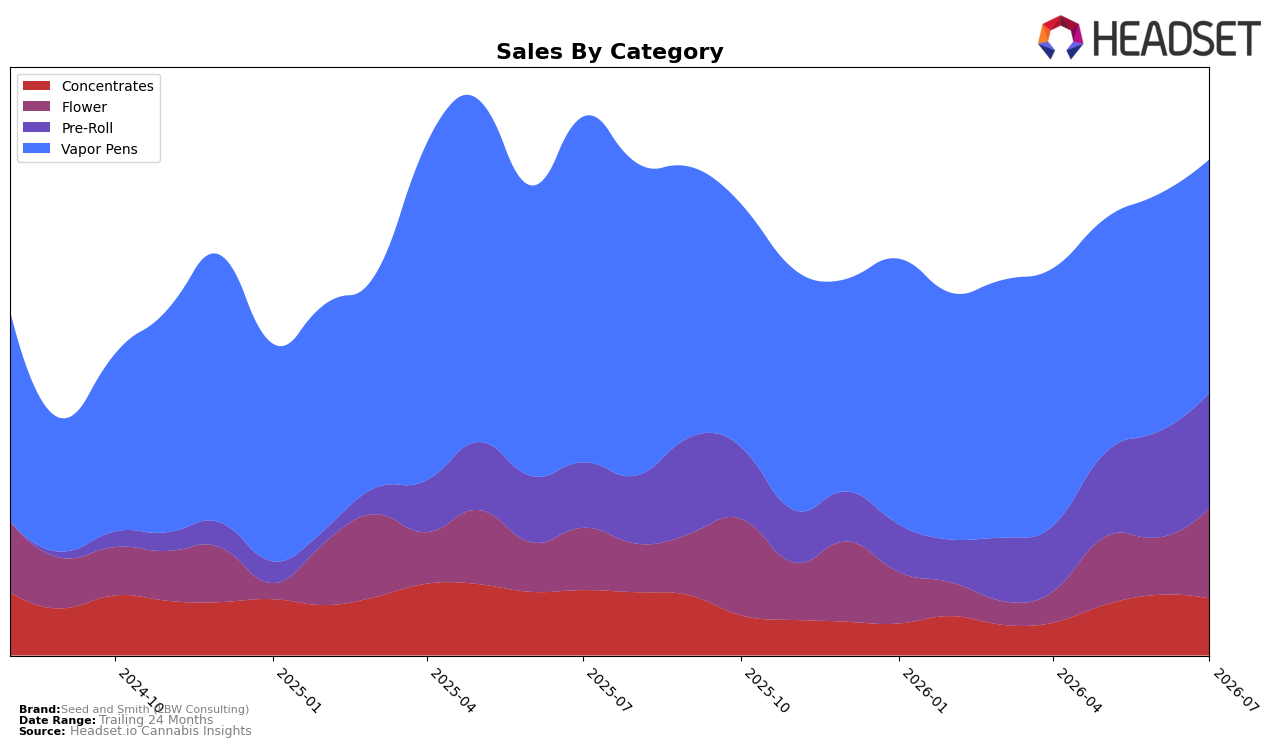

Seed and Smith (LBW Consulting) concentrated 46.45% of July 2026 sales in Vapor Pens, where category sales fell 32.11% year over year and 1.53% month over month, while Pre-Roll rose 72.20% YoY and 8.78% MoM to 23.31% share. Flower expanded to 18.37% share with 42.55% YoY growth and a 53.91% MoM jump, as Concentrates slid 12.11% YoY and 5.56% MoM to 11.87% share; the brand held rank 16 in Vapor Pens in Colorado. Despite a 1.68% YoY uptick in average price to $22.31, the -7.71% brand-level YoY sales contraction alongside a 65.16% 24‑month gain implies an ongoing pivot away from a shrinking Vapor Pens base toward faster-growing Pre-Roll and Flower to stabilize near-term volatility.

The mix shift implies margin and positioning trade-offs: Vapor Pens’ leadership share at 46.45% is eroding (-32.11% YoY) while Flower’s 53.91% MoM spike and Pre-Roll’s 8.78% MoM lift suggest momentum in value-accessible formats despite Concentrates declining 5.56% MoM. With Vapor Pens anchored at rank 16 in Colorado and category-specific averages at $28.73 for Vapor Pens versus $14.59 for Flower, the tilt toward Flower and Pre-Roll could depress blended price even as unit velocity rises; the pattern implies Seed and Smith (LBW Consulting) is trading some high-ticket Vapor Pens exposure for volume-led share defense, making Pre-Roll and Flower the practical levers to offset Vapor Pens contraction.

Competitive Landscape

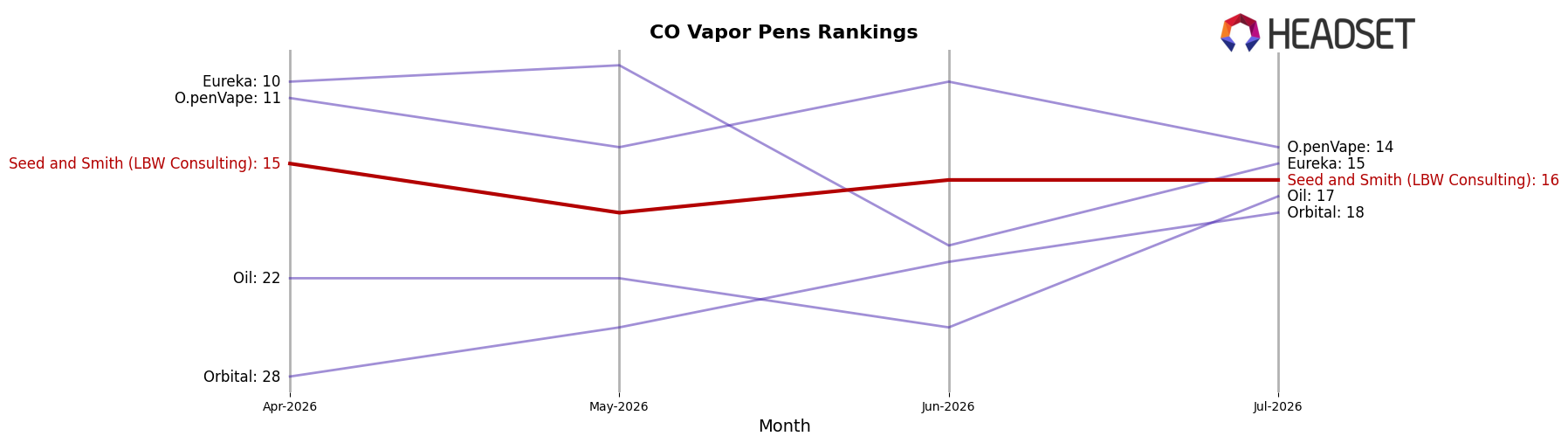

Seed and Smith (LBW Consulting) sits at rank #16 in CO Vapor Pens for July 2026, down 5 positions year over year from #11, and off 1 place from April 2026’s #15, while still trailing its historical peak of #8 from April 2025; in contrast, Spherex held at #1 year over year with a 7.2% sales lift and PAX advanced from #3 to #2 on 21.7% YoY growth, indicating share consolidation at the top as Seed and Smith (LBW Consulting) slips from the upper mid-pack. With Jetty Extracts jumping from #19 to #5 on 181.4% YoY growth and Green Dot Labs improving from #6 to #4 alongside a 76.5% YoY increase, the brand’s 5-rank YoY decline and 1-rank slide since April 2026 imply erosion of competitive position driven by faster-moving rivals rather than category contraction.

Notable Products

Space Force (Bulk) led July 2026 with a 110.2% month-over-month surge and a jump to rank 1, signaling outsized traction for value-driven Flower. Vapor Pens provided secondary momentum as Pineapple Donut Live Resin Cartridge (1g) rose 29.0% to rank 6 while Apricot Scone Live Resin Cartridge (1g) climbed 24.0% to rank 10, and four of the top ten are Flower SKUs concentrated in 3.5g formats. The pattern implies a barbell mix: bulk Flower scaling at the top-end while Live Resin cartridges deepen mid-pack velocity, pointing to a portfolio skew toward value entry points and terp-driven inhalables rather than breadth expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.