Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

In The Flow is stocked at 64 licensed dispensaries across Colorado and West Virginia, 33 of them in Colorado, with the deepest coverage in Boulder, Denver, Grand Junction, Aurora, and Durango. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

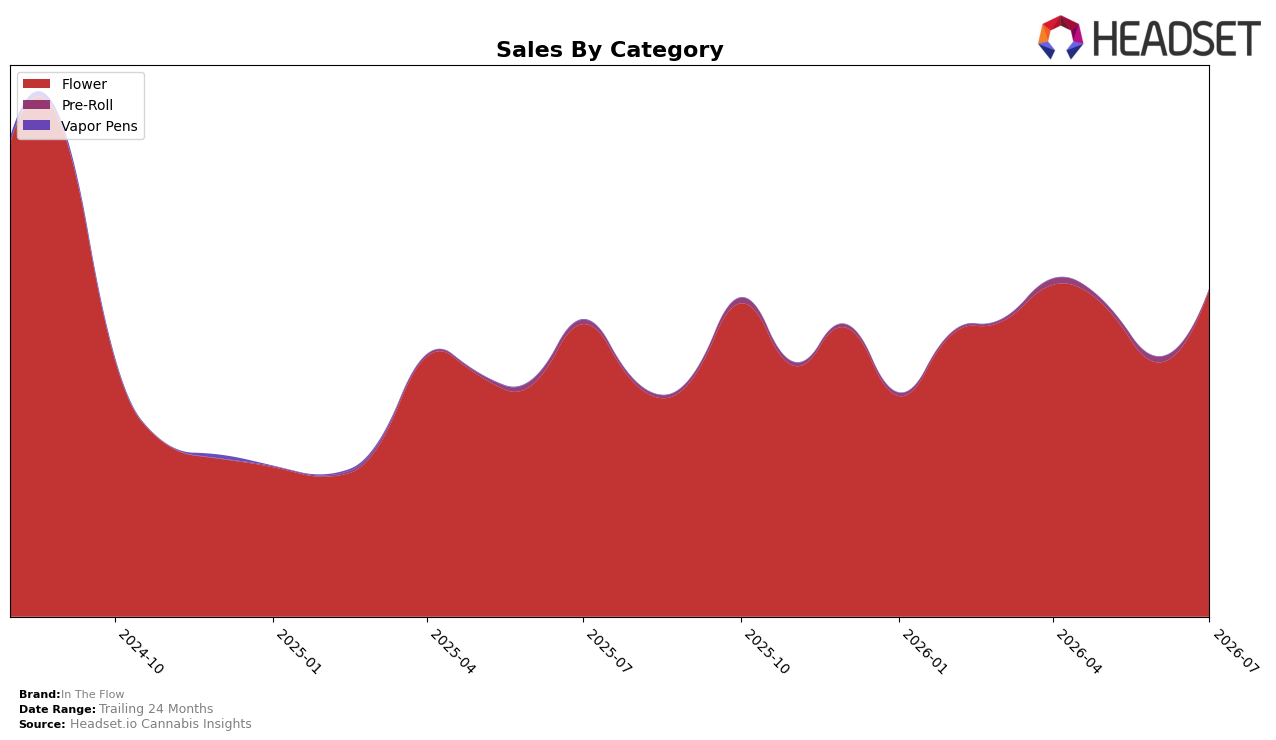

In The Flow concentrated 99.77% of July 2026 sales in Flower, with Pre-Roll at 0.23% share, as Flower rose 11.96% year over year and 28.86% month over month while Pre-Roll fell 80.82% YoY and 85.71% MoM. The brand’s overall sales grew 10.63% YoY alongside a 65.48% YoY increase in average price, and Flower’s average price at $25.05 aligns with that pricing pivot. This mix and pricing combination implies the brand is leaning into a higher-priced Flower-led model that lifts short-term revenue at the cost of breadth, with minimal Pre-Roll presence constraining cross-category reach.

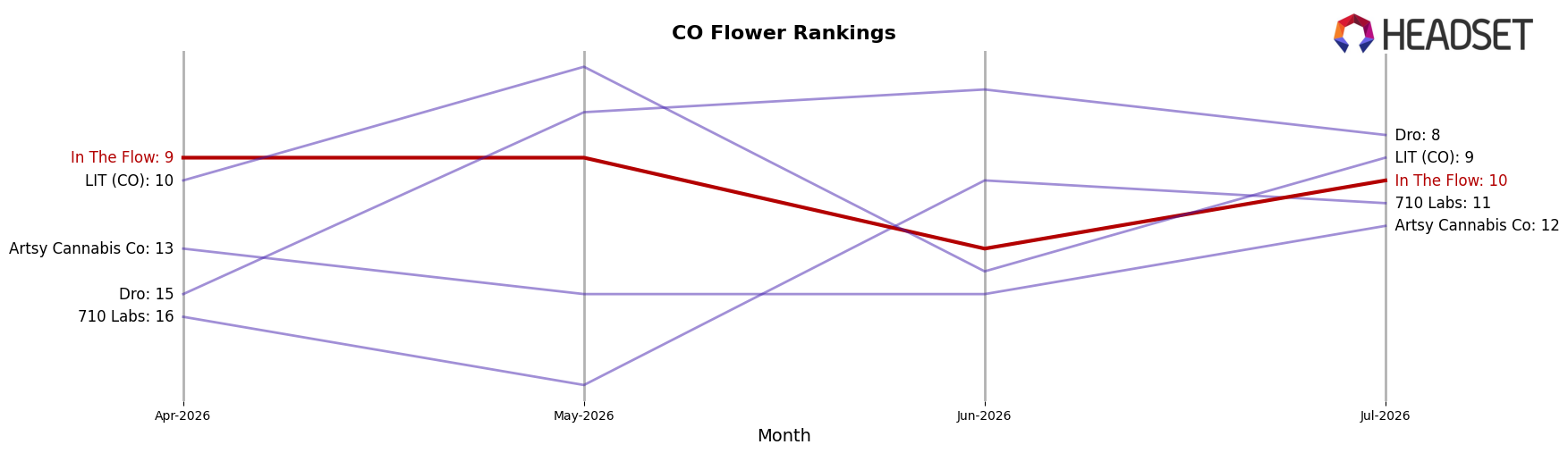

Within Flower in Colorado, In The Flow held rank 10 while posting a 28.86% MoM surge and an 11.96% YoY gain, indicating momentum concentrated in a single category as the portfolio narrows. The 65.48% YoY price increase alongside a 31.73% two-year sales decline suggests a shift from volume diversification toward price-led value capture, and the 0.23% Pre-Roll share with an 85.71% MoM decline signals retreat from entry-price formats. This pattern implies that sustaining rank 10 will depend on maintaining Flower price realization without eroding velocity, or reintroducing selective Pre-Roll presence to buffer demand elasticity.

Competitive Landscape

In The Flow sits at rank #10 in Colorado Flower in July 2026, down three positions year over year from #7, and one spot below its April 2026 position of #9; this contrasts with Seed & Strain Cannabis Co. moving from #2 to #1 alongside a 76.2% year-over-year sales gain, while Good Chemistry Nurseries eased from #1 to #3 with an 8.7% sales decline. Further, In The Flow’s peak at #7 in December 2025 has reverted to #10, whereas Natty Rems jumped from #23 to #5 with 168.5% growth, indicating that momentum is consolidating among faster risers and that In The Flow’s rank trajectory implies a need to regain share or risk further relegation from the top 10.

Notable Products

Lilac Diesel (Bulk) posted the largest movement with a 441.9% month-over-month surge in July 2026, jumping into rank 4, while Lemon Skunk (Bulk) also accelerated by 161.9% to rank 6; in contrast, Chemmy Jones (Bulk) slipped 10.2% to rank 8 and Donny Burger (3.5g) fell 12.2% to rank 2. Chemmy Jones (1g) held rank 1 with a 9.0% lift and Chemmy Jones (3.5g) advanced 19.9% at rank 3, and five of the top ten are Bulk SKUs concentrated between ranks 4 and 10, signaling a shift toward value and volume formats even as legacy eighths maintain premium visibility. This pattern implies In The Flow is tilting assortment and demand toward Bulk Flower to capture larger basket sizes while protecting flagship recognition in smaller formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.