Market Insights Snapshot

iTHaCa Cultivated’s mix in May 2026 was overwhelmingly Flower at 99.13% share, with Tincture & Sublingual at 0.87% share, a concentration that coincided with a 212.26% year-over-year sales jump in Flower and a 10.23% month-over-month increase. In contrast, Tincture & Sublingual contracted 53.25% month over month while lacking a year-over-year baseline, and the brand’s average price rose 16.05% year over year to $92.67 alongside a 215.00% brand-level year-over-year sales increase. The pattern implies an intentional pivot toward Flower that is expanding volume while supporting higher realized prices, with the shrinking Tincture & Sublingual presence signaling de-prioritization of ancillary formats in favor of a single-category scale play.

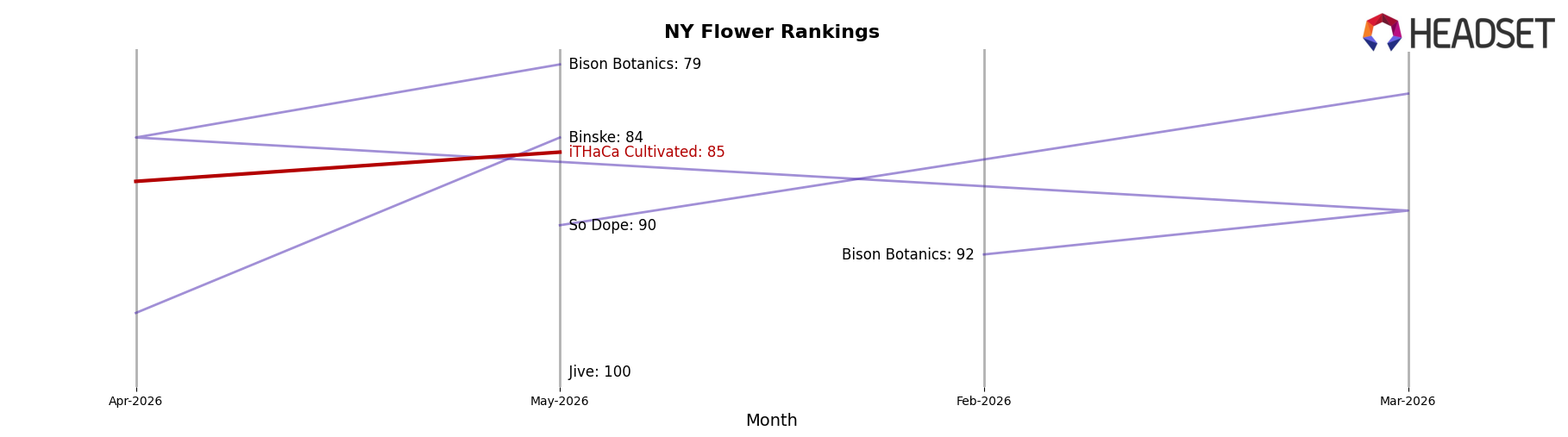

Within Flower, the May 2026 rank of 85 in New York positions iTHaCa Cultivated as a lower-tier participant despite the category’s 99.13% share and double-digit month-over-month growth, indicating that gains are derived from deepening in a single lane rather than breadth across formats. The 62.71% two-year sales increase paired with a 212.26% Flower year-over-year surge suggests recent momentum is disproportionately recent, and the 10.23% month-over-month Flower lift against a 53.25% month-over-month decline in Tincture & Sublingual points to a trade-up dynamic where the brand is leaning into price elasticity within Flower. This implies the near-term positioning is as a Flower-focused specialist competing on depth and pricing power rather than multi-format coverage, with rank headroom available if category concentration translates into sustained share capture.

Competitive Landscape

iTHaCa Cultivated sits at rank #85 in May 2026 in NY Flower, a 57-place improvement from rank #142 year over year, yet still below its peak rank #42 reached in July 2024; meanwhile, Leal climbed from #11 to #1 with 109% YoY sales growth and RYTHM advanced from #10 to #4 with 46% YoY sales growth, while Dank. By Definition slipped from #1 to #2 alongside a 38% sales decline. This combination of iTHaCa Cultivated’s 57-rank YoY gain and competitors’ mixed shifts at the top implies a recovery path that is improving but still distant from prior peak positioning, requiring share capture against leaders who are accelerating.

Notable Products

Candy Garlic (14g) posted the month’s sharpest movement with a +343.4% month-over-month jump into rank 7, while Spritzer (14g) fell -17.4% to rank 4 and Bolo Runtz (14g) declined -16.7% at rank 10. Lemon Meringue (14g) also crossed the +50% threshold at +52.7% to rank 6, whereas category leader Sour Diesel (14g) slipped -8.8% but held rank 1; nine of the top ten are Flower SKUs, indicating a concentrated portfolio. With King Louis (14g) up +61.1% at rank 9 against Gorilla Glue (14g) advancing +37.4% to rank 2, the mix is tilting toward fast-rising mid-table strains rather than relying solely on the top-ranked anchor. The pattern implies iTHaCa Cultivated is shifting commercial momentum to breadth within Flower, leaning on breakout mid-tier SKUs to diversify rank risk while the flagship holds share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.