Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

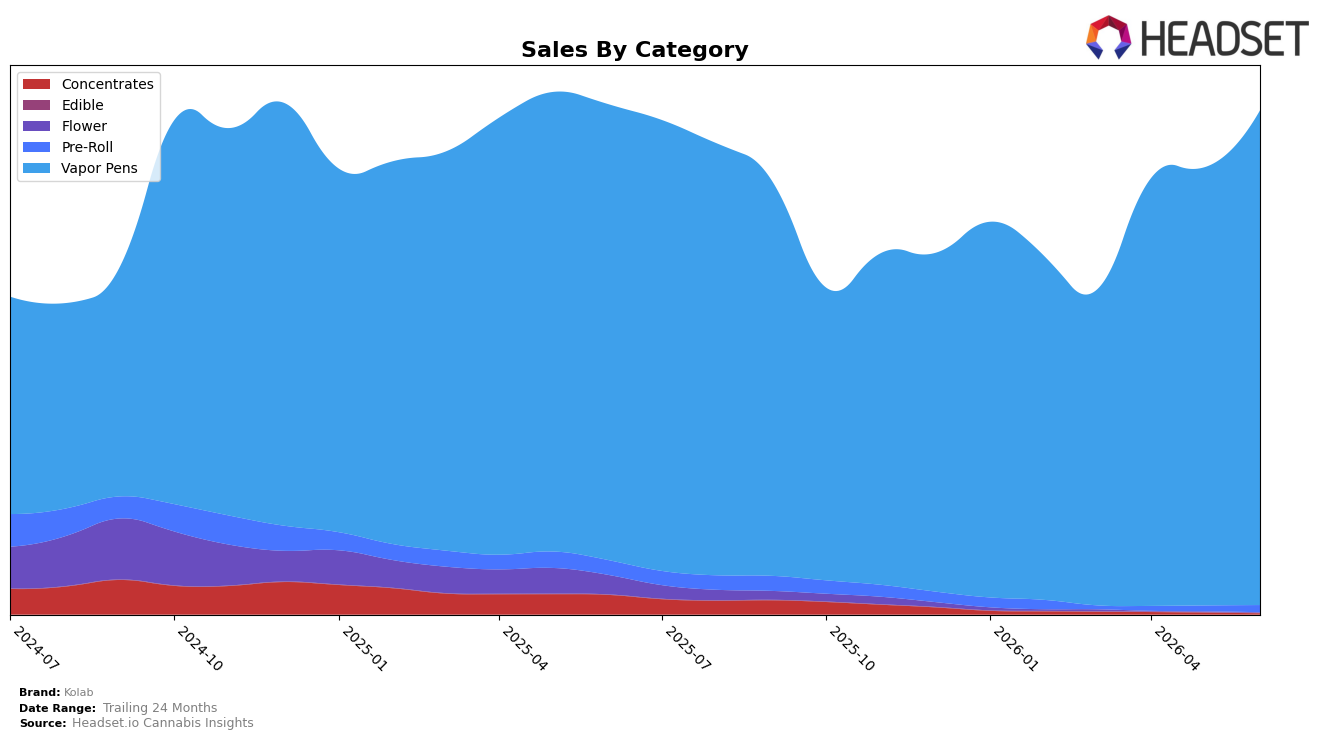

In June 2026, Kolab is effectively a one-category brand, with Vapor Pens accounting for 98.47% share and growing 12.90% month over month and 8.52% year over year, while Pre-Roll holds 1.33% share after a 21.89% MoM lift but a 53.54% YoY drop. The long tail collapsed: Concentrates fell 41.40% MoM and 95.13% YoY to 0.19% share, and Flower declined 67.70% MoM and 99.60% YoY to 0.02% share. With overall brand sales down 1.22% YoY against a 17.05% YoY price decline, the mix shift toward Vapor Pens is cushioning volume but amplifying reliance on a single category, implying operational focus on pen throughput at the expense of portfolio breadth.

This concentration lines up with market positioning: in Alberta Vapor Pens, Kolab sits at rank 4, and the 12.90% MoM growth in the category that drives 98.47% of sales suggests share defense via scale rather than diversification, even as Pre-Roll’s 21.89% MoM rebound and 53.54% YoY decline signal a volatile, secondary role. Given the 75.27% sales lift over 24 months alongside a 17.05% YoY price drop, the brand is trading margin for volume in Vapor Pens while exiting low-scale segments (Concentrates down 95.13% YoY; Flower down 99.60% YoY), implying a positioning bet on pen-led distribution density and price elasticity rather than multi-category presence.

Competitive Landscape

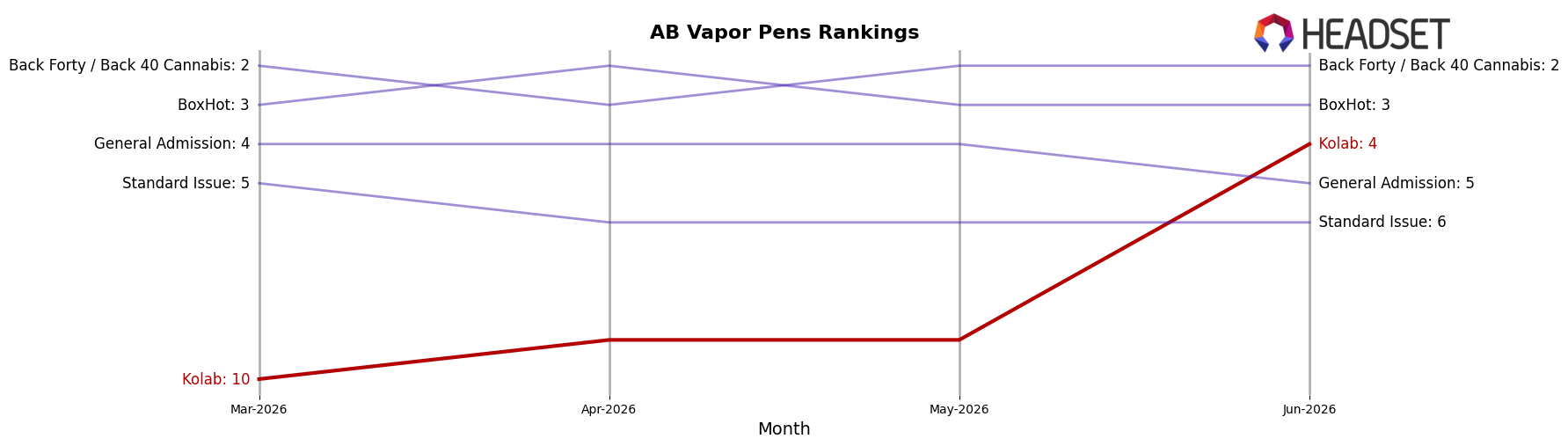

Kolab is ranked #4 in AB Vapor Pens in June 2026, improving 4 positions year over year from #8 and rising 6 spots since March 2026 when it sat at #10; this climb coincides with a peak rank of #4 in June 2026 and places it one step behind BoxHot at #3, while Spinach held at #1 with a 43.97% year-over-year sales increase and General Admission slid from #4 to #5 alongside a -14.82% sales change, indicating Kolab’s rank trajectory is advancing through mid-tier positions toward the top three on momentum rather than category contraction.

Notable Products

Purple Diesel Liquid Diamonds Disposable (1g) posted the steepest decline at -26.6% month over month while sliding to rank 8, and Pure Liquid Diamonds Disposable (1g) also contracted -20.4% at rank 6, indicating a pullback in Disposable SKUs even as overall category leaders advanced. At the top, Blue Passionfruit Diamonds FSE Cartridge (1g) surged +34.5% to rank 2 while Pink Lychee Diamonds Distillate Cartridge (1g) climbed +28.4% at rank 1, and Strawberry Ice Diamonds Distillate Cartridge (1g) increased +24.3% at rank 3, concentrating three of the top five in Vapor Pens cartridges rather than disposables. Wedding Pie Pre-Roll 10-Pack (3.5g) rose +21.7% at rank 7, but the Pre-Roll presence remains a single entry versus eight Vapor Pens in the top ten, pointing to a lineup skew where cartridges are gaining share as disposables retreat. The pattern implies Kolab is consolidating momentum in Diamonds-based cartridges while paring exposure to underperforming disposables, a mix that directs near-term focus toward cartridge depth over form-factor breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.