May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

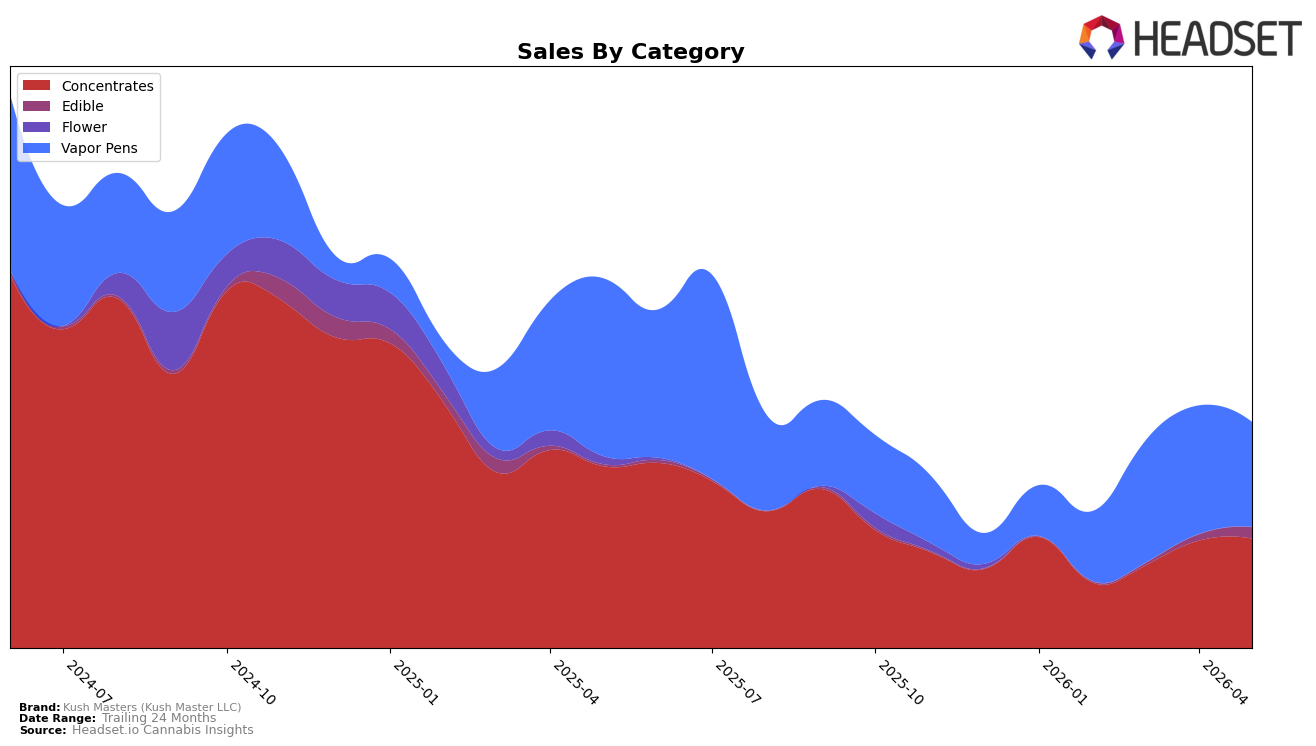

In May 2026, Kush Masters (Kush Master LLC) derived 48.54% of sales from Concentrates and 46.50% from Vapor Pens, with Edible contributing 4.96%; within this mix, Concentrates ticked up month over month by 1.88% while Vapor Pens declined 18.46% month over month, and Edible surged 86.26% month over month. Year over year, Concentrates fell 39.89% and Vapor Pens fell 41.07%, contrasted by Edible up 554.93% year over year; average price declined 8.45% year over year to $16.89, while Concentrates averaged $15.02 and Vapor Pens $20.14, indicating price pressure alongside a small mix reweighting toward categories with either lower price points or higher promotional intensity. This pattern implies the portfolio is pivoting at the margin from a two-category concentration toward a three-legged mix where Edible becomes a growth lever, cushioning volume gaps from Vapor Pens while maintaining a Concentrates core.

Positionally, a 27 rank in Concentrates within Colorado alongside a 48.54% internal share and a 1.88% month-over-month lift suggests that category remains the anchor, while the 18.46% month-over-month sell-down in Vapor Pens at a $20.14 average price points to elasticity limits relative to the brand’s $16.89 overall average and a 8.45% year-over-year price decrease. The 554.93% year-over-year and 86.26% month-over-month growth in Edible at a $12.99 average price indicates headroom to win price-sensitive baskets without cannibalizing Concentrates’ role; combined with a 38.96% brand sales year-over-year decline, the mix shift implies near-term share defense will come from deepening Edible presence while selectively stabilizing Vapor Pens rather than chasing volume at further discount across the board.

Competitive Landscape

Kush Masters (Kush Master LLC) sits at rank #27 in CO Concentrates in May 2026, slipping 1 place year over year from #26 while improving 9 spots from #36 three months earlier; relative to its historical peak at #7 in May 2024, the brand is 20 positions lower, indicating a multi-year comedown despite the recent quarter-on-quarter climb. Competitively, Amber climbed from #3 to #1 with a 101.7% year-over-year sales increase while 710 Labs held at #2 despite a 16.9% sales decline, and Billo surged from #16 to #5 with 128.2% growth—movement that compresses share at the top and raises the bar for upward mobility from #27. The rank trajectory—down 1 year over year but up 9 since February 2026—implies stabilization at a mid-pack position with limited near-term path back toward the May 2024 peak unless gains outpace faster-rising leaders.

Notable Products

Sour Cleaner Wax (1g) delivered the standout move in May 2026 with a 115.8% month-over-month surge to rank 1, while Maple Breath Wax (1g) slipped 1.1% at rank 2, indicating a reshuffle at the top of Concentrates. With four Concentrates SKUs in the top ten including Cloud Walker Wax (1g) at rank 4 and Strawnana Wax (4g) at rank 6, the balance of power tilted toward extract formats even as Dirty Dawg Cured Resin Cartridge (1g) grew 12.5% at rank 9 and Fruit Basket Cured Resin Cartridge (1g) rose 14.0% also at rank 9. The simultaneous expansion of the leading wax SKU and modest gains in lower-ranked Vapor Pens suggest Kush Masters (Kush Master LLC) is leaning into high-velocity Concentrates while using select cartridges to maintain breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.